A minute localized change in a complex system that has large effects elsewhere is known as the “Butterfly Effect” or in mathematics, “Chaos Theory”

That phenomenon has been evident since Donald Trump won the 2016 US election but it reached new heights of prominence in the past week.

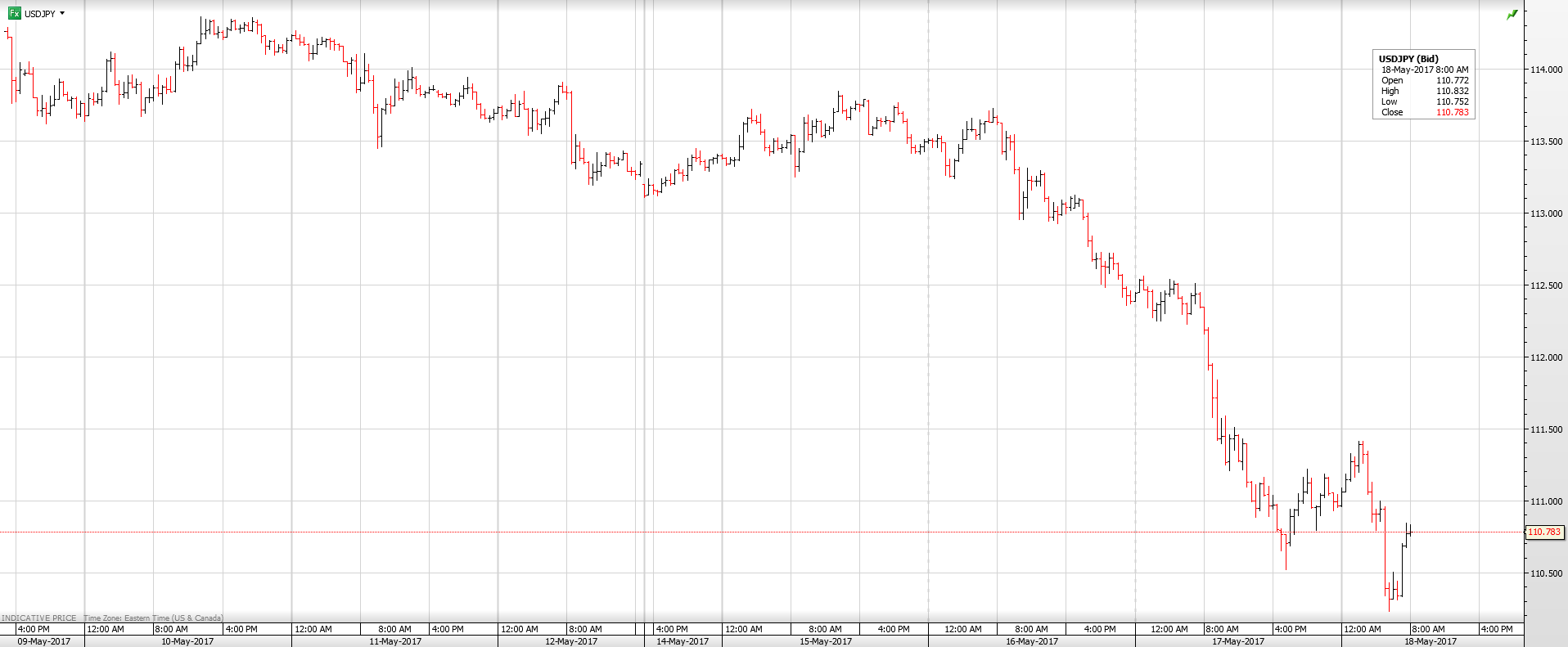

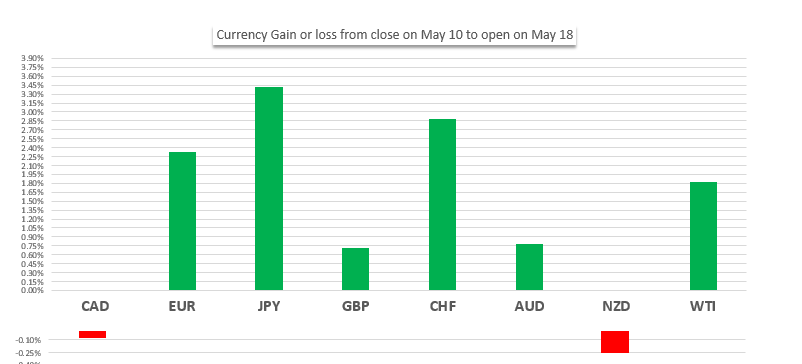

President Trump flapped his gums in Washington D.C. and in Tokyo, the Japanese Yen soared, rising 3.5 percent inside a week.

The issue is “Did, President Trump interfered in an FBI investigation?”

Last week, Mr. Trump fired the FBI Director James Comey, who still had seven years to run on his contract. Mr. Trump explained his actions, saying “He’s a showboat. He’s a grandstander. The FBI has been in turmoil,” “I was going to fire Comey. My decision. I was going to fire regardless of recommendation.”

If there is any truth to the adage that American public officials “serve at the pleasure of the President”, then clearly, Mr. Trump was not getting any pleasure from Mr. Comey.

And if Mr. Comey was not giving him any pleasure, Mr. Trump is likely to be even more unhappy with Robert S. Mueller.

He is a former FBI Director and has been appointed by the Justice Department to oversee the investigation into ties between President Trump’s campaign and Russian officials.

That is the news that really spooked financial markets. The words, “official inquiry and Trump” in the same sentence, evoked memories of Bill Clinton and Monica’s dress or even worse, Nixon and Watergate. Traders didn’t just jump to conclusions, they pole vaulted to them.

There were no shortage of media stories trumpeting market mayhem. “Equity Markets Plunge”, “Dow Dives” or “Dow Has Worst Day in 8 Months, are just a few.

Currency markets reacted like (or to) the equity market price moves and extended the US dollar losses seen for the past week, even further. Only the New Zealand and Canadian dollar’s failed to benefit from the broad greenback weakness.

The entire Trump/Comey saga is entertaining and it injected a much need dose of volatility into financial markets.

It was just a few days earlier when market pundits were lamenting the lack of volatility in the Chicago Board of Trade Volatility Index (VIX). In less than a week, the VIX has jumped from a low of 9.65 to 16.25.

However, perhaps the reaction is more of the mountain/mole hill variety.

When you strip away “he said, she said” from the Trump/Comey debate, all that is left is Washington politics.

Mr. Mueller is charged with investigating the Trump Campaign and its ties to Russia not President Trump.

The Democrats and major media outlets like the Washington Post, New York Times and CNN are rabidly anti-Trump.

Many Republican’s aren’t overly fond of the President either, but they are rabidly anti-Democrat, and have a majority in the Senate.

Enough is enough.

The focus will shift from the White House to the US economy next week and when it does many of today’s US dollar seller’s will become US dollar buyers.

The minutes from the May 3 FOMC meeting are due on May 24. FX markets have forgotten how balance sheet normalization talk led to US dollar demand, earlier. These minutes may bring that issue to the forefront, again.

Q1 GDP and Durable Goods data are due on May 26. Better than expected results will not only boost June rate hike expectations and but renew calls for two or three more hikes in 2017.

The Japanese yen was the biggest beneficiary of the rush to reduce risk so it wouldn’t be much of a stretch to suggest that it would also be the biggest loser if US rate hike fever takes hold.

The Yen may have been a beneficiary, but the Loonie has been an enigma.

The Canadian dollar rallied from May 10 but that move was largely due to a 9 percent rally in oil prices. It didn’t appear to derive much benefit from the broadly weaker US dollar, although it was certainly a factor.

The list of Canadian dollar negatives is long. They include; the risk of further US trade sanctions, the perception of a housing market bubble floating in a cactus patch, M&A flows resulting in Canadian dollar selling, a doveish Bank of Canada and selling of Canadian dollars for euros and sterling.

The list of Canadian dollar positives is much shorter. The prospect that Opec will announce a nine-month extension to production cuts at their May 25 meeting, could trigger a rally in WTI prices and by default, the Loonie.

The Trump/Comey show is not coming to an end any time soon but it is intermission time. Traders can run out to the concession stand, grab a bag of hot buttered economic data, wash it down with a fine Opec vintage and concentrate on data not drama