By Michael O’Neill

It’s a game of roulette for corporate treasurers, exporters, and importers. And the Bank of Canada (BoC) is spinning the wheel.

FX risk managers with Canadian dollar exposure face a Shakespearian dilemma. “To hedge or not to hedge, that is the question.” The central bank isn’t making their task easy. On September 4, the BOC released a terse monetary policy statement that didn’t do anything to lift the veil of uncertainty around the domestic interest rate outlook. For many analysts, it is a perplexing result.

The July 10 meeting left the overnight interest rate unchanged at 1.75%. The statement showed concern about the global economic outlook saying, “Evidence has been accumulating that ongoing trade tensions are having a material effect on the global economic outlook.” Apparently, they were not surprised. They said, trade tensions were already incorporated into their forecasts. The statement concluded with “Recent data show the Canadian economy is returning to potential growth. However, the outlook is clouded by persistent trade tensions. Taken together, the degree of accommodation being provided by the current policy interest rate remains appropriate.”

Since then, the US/China trade war has intensified. Both sides slapped new tariffs on imports at the start of September. The September 4 BoC statement acknowledged the escalation in trade hostilities. It said “As the US-China trade conflict has escalated, world trade has contracted and business investment has weakened. This is weighing more heavily on global economic momentum than the Bank had projected in its July Monetary Policy Report.”

The BoC was pleased with the better than expected Q2 GDP growth but warned some of the strength was temporary. They admitted concern about soft consumption, weaker Business Investment, and that household debt levels were rising from “already-high levels.” Nevertheless, their analysis concluded that “In this context, the current degree of monetary policy stimulus remains appropriate.” Huh? Other central bank’s had similar concerns and cut interest rates.

BoC Deputy Governor Lawrence Schembri justified the decision to leave rates unchanged, in a speech in Halifax, on September 5. He said “the Canadian economy is operating close to full potential, the unemployment rate is near historic lows and inflation—our primary responsibility—is right on target.” Mr Schembri added: “central banks have been conducting monetary policy appropriate to their own circumstances and outlooks. This has contributed to lower bond market yields and reduced borrowing costs in Canada.”

In other words, the domestic economy is too strong to cut interest rates.

The September 4 BoC statement said, “growth in the United States has moderated but remains solid, supported by consumer and government spending.” Still, the Fed is cutting interest rates. They chopped the overnight fed funds range to 2.00-2.25% from 2.25-2.50% on July 31, and CME Fedwatch says there is a 90% probability that rates will be cut again, in two-weeks. To paraphrase the immortal words Gomer Pyle, USMC, “Shazam, Shazam, Shazam, what is the BoC thinking?”

The major central banks are easing monetary policy because of domestic economic risks from the China/US trade war. The BoC sees the same risks but left rates unchanged because “it is appropriate for our circumstances.” Yet, in a somewhat contradictory statement they admitted being spooked by those same risks writing “given Canada’s reliance on international trade, we agreed that the trade war remains our primary concern and the biggest risk to our forecast.”

There are numerous time-bombs still ticking that, if they go off, would lead to another stampede into safe-haven trades and undermine the Canadian dollar in the process.

UK political dysfunction is coming to a head. The danger of a “no-deal” Brexit is looming, despite UK Prime Minister Boris Johnson’s set-backs. Many UK Members of Parliament insist on reopening Brexit talks with the European Union. (EU) However, to do so, they need unanimous approval from the 27 member EU, which may be difficult. A “no-deal Brexit” is still on the table.

The European Central Bank is expected to announce a new series of monetary stimulus measures next week. The measures may include a 10 basis point cut in the deposit rate, which is currently negative 0.40%. The Peoples Bank of China is rumoured to be planning to trim their benchmark Reserve Requirement Ratio (RRR) along with other fiscal stimuli.

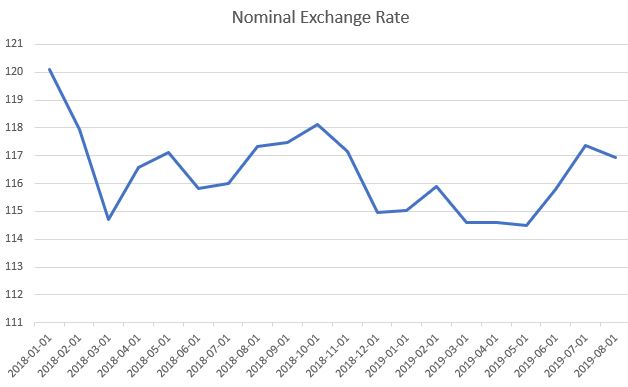

The major central banks are cutting rates but not the BoC. That is good news for Canadian importers but not so good for exporters. The Canadian dollar and Japanese yen are the only currencies to have gained against the US dollar since January 2, 2019. And the Canadian dollar has gained the most, rising 3.15%. Even, worse, the Bank of Canada’s Canadian Effective Exchange Rate (CEER) has strengthened since the beginning of May. The BoC defines the CEER as a weighted average of bilateral exchange rates for the Canadian dollar against the currencies of Canada’s major trading partners.

Chart: Canadian Effective Exchange Rate (CEER)-monthly from January 1, 2018

Source: Bank of Canada/IFXA

Corporate Treasurers and importers that need to buy US dollars and sell Canadian dollars, between now and year-end should consider the current levels to start hedging. USDCAD has been in a ragged, yet steady uptrend since January 2013. The uptrend line has survived numerous tests and comes into play at 1.2950. (about 77.00 US cents to 1 Canadian dollar) Furthermore, the currency pair has been locked in a 1.3025-1.3660 range since the beginning of the year. At 1.3200, USDCAD has 0.0250 points of downside compared to 0.0465 points of upside. More importantly, the Canadian dollar is rising on a CEER basis, at the same time oil prices are declining.

It isn’t too much of a stretch to believe the Bank of Canada is spinning the roulette wheel with their bet riding on the “sunshine and unicorns” slot. Corporate Treasurer’s are left deciding “to hedge, or not to hedge.”