Photo: Wikimediacommons/IFXA Ltd

By Michael O’Neill

When any government say’s “this is no time for austerity” taxpayers should worry. When those words are uttered by a government that increased a budget deficit 1,275% in less than six months, taxpayers should be terrified.

Welcome to Canada.

The forty-third session of the Parliament of Canada resumed September 23. It had been interrupted when Prime Minister Trudeau’s government prorogued parliament after dumping the Finance Minister, to avoid questions on WE charity corruption, and numerous ethics violations.

They’re back, and your wallet is wide open.

The Throne Speech sketched the government’s approach for the rest of the year, saying it was based on four foundations. They are: 1) Fighting the pandemic, 2) Supporting people and businesses, 3) Build a better Canada, 4) Stand-up for who we are as Canadians.

Delivering on the promises is easy. All it takes is debt. The Throne Speech noted “with interest rates so low,” governments can lock in “the low cost of borrowing for decades to come.” Reclassifying ‘Borrowing’ as an ‘Investment in the Future’, certainly assists the optics. Unfortunately, when its time to pay the piper, your grandkids and their grandkids will be digging deep.

The Throne Speech did not put any dollar amounts to the spending initiatives. Instead, those numbers will be available “this fall” when the government provides a new economic and fiscal update.

The existing $343.2 billion budget deficit will very likely balloon, as the government borrows heavily to fund its promises. Fitch Ratings cut Canada’s debt rating from AAA to AA+ Stable in June. They were concerned with the significant fiscal deterioration in 2020 and may get scared silly when the new programs are introduced.

However, not everyone thinks large deficits are a problem. David Wessel, Director – The Hutchins Center on Fiscal and Monetary Policy wrote in an article for the Brookings Institute about this issue. He said “if interest remain low, as currently anticipated, the government can handle a much heavier debt load than was once thought possible. The key to managing a ballooning debt is low-interest rates.” So, perhaps a sharply rising Canadian deficit is not a bad thing, providing low interest rates prevail. If rates rise, presumably its not.

On the other hand, the size of the deficit may be problematic when compared with G-10 peers, all of which are vying to attract global investment.

The US and the Eurozone economies are large and diverse enough that they may be able to tolerate massive deficits. It may not be the same for smaller economies. FX traders tend to lump Canada and Australia into the same boat as both are English speaking, resource-based economies, of similar size.

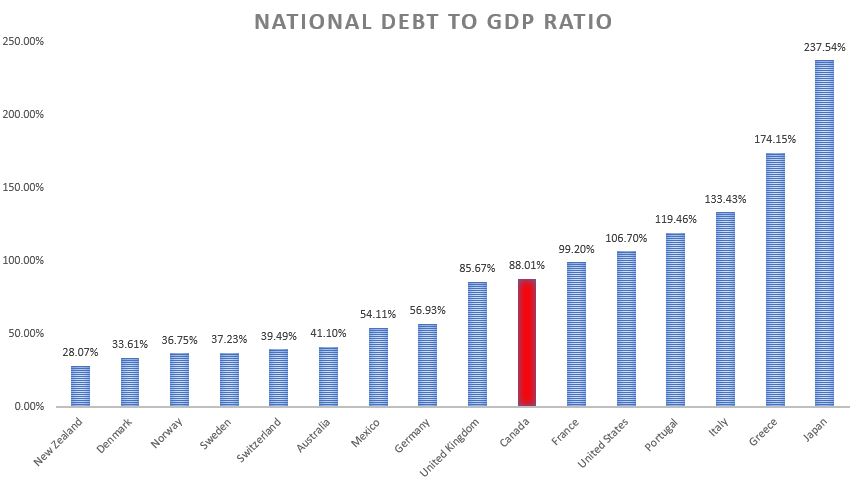

Nevertheless, when it comes to attracting capital inflows, Australia may have far more appeal than Canada, as highlighted by the following chart. Canada’s debt to GDP ratio is more than double that of Australia, which also explains why Australia still has a AAA debt rating.

Source: IFXA/Worldpopulation review.com

Canadian taxpayers will pay the price for the latest government initiatives, and the Canadian dollar may suffer as well.

Climate Change is a cornerstone of the government plan to create jobs. They will “Support manufacturing, natural resource, and energy sectors as they work to transform to meet a net zero future, creating good-paying and long-lasting jobs” while taxing industries that pollute.

Alberta Premier Jason Kenney was not impressed. He claimed the Throne Speech doubled down on job-killing policies. Canada’s energy industry employs around 800,000 people directly and indirectly and generates 20% of government revenues. Eventually, international investors will ask how the government will pay for new climate change initiatives as these revenues disappear.

Australia’s climate change policies are far less onerous, and damaging to industry, making that country a more attractive destination for investment capital.

Canada, US, and Mexico ratified a new trade deal that at the beginning of the year. Since then, the US has levied tariffs on Canadian aluminum and threatened levies on softwood lumber and even lobsters. The aluminum tariffs have been repealed but replaced with quotas. The Canadian dollar continues to be vulnerable to aggressive US trade strategies which will only get worse if President Trump is re-elected.

The Canadian dollar is vulnerable to a slew of external influences as well. China is getting more aggressive expressing their annoyance at the US for cooperating with Taiwan.

. The US election on November 3 could be a flash-point for a rash of risk-aversion trades. The George Bush/Al Gore, “hanging chads” farce took over a month to resolve. President Trump is already talking about needing the Supreme Court to resolve the 2020 election.

Things could turn nasty if he loses as Republican’s are better armed then Democrats.

USDCAD peaked above 1.6000 in January 2002. That was due to the Russia and Emerging Market debt crisis in 1998, the tech stock meltdown, and culminating with the 911 terrorist attacks in the US. A US/China shooting war and/or another explosive resurgence of the COVID-19 pandemic could be catalysts. A break above 1.4470 would set the stage for a re-test of the all-time peak.

The Canadian Loonie isn’t quite cooked, but it is in the oven.