By Michael O’Neill

The Canadian dollar was a car-wreck on October 25. Not a little parking lot fender bender, either. It was a massive, multi-car mash-up that left damage and destruction in its wake. And it was all caused by the Bank of Canada.

In car racing terms, the Bank of Canada (BoC) quarterly Monetary Policy Report, policy statement and press conference was the equivalent of the Daytona 500. It was a hot ticket.

Financial markets eagerly awaited the central bank’s reaction to moderately strong domestic data, including rising inflation, the Finance Minister’s Fall Update, NAFTA negotiations and higher oil prices.

Traders were expecting the BoC to be cautious. Caution is part of its DNA. They expected the overnight rate target to be left unchanged at 1 percent and an acknowledgement of a gradual approach to interest rate increases. Markets were also looking for confirmation a December rate increase was still on the table supported by a claim that the “output” gap was closing.

The BoC met most of those expectations. They have a tightening bias as Governor Stephen Poloz confirmed when he said: “less monetary stimulus will be needed in the future.” They believe that the economy is close to its full potential although there may still be some labour market slack.

Nevertheless, the Bank is not in a hurry to raise rates. They are still monitoring how the previous two increases impacted the economy. They are staying cautious. Mr Poloz repeated the four key uncertainties that he cited in his September speech. That was the speech that precipitated the Canadian dollar’s steep drop. They noted substantial uncertainty about geopolitical developments and the North American Free Trade Agreement. Recent changes to domestic mortgage rules are another reason to be cautious.

None of the above should have surprised market participants expecting a cautious outlook, and for the most part, they weren’t.

The surprise came when it became apparent that not only was a December rate hike no longer on the table; rate hikes may not be considered until sometime in the spring.

Governor Poloz admitted as much when he answered a question about the fiscal stimulus announced in the Fall Update. He responded by saying “he wasn’t in a position to judge the Fall Update,” adding he “needs a complete budget” to assess.

In 2017, the Budget date was March 22, 2017. If Budget 2018 falls around the same date, the closest BoC policy meeting afterwards (a potential rate hike day) is April 18, 2018.

The news hit the Loonie like a NASCAR on a wall. The Canadian dollar dropped 1.2% in the blink of an eye and then extended those losses the rest of the day.

“The Loonie suffered a similar fate as these cars after the BoC announcement” Source: Google Images

The Canadian dollar could have got some support from the Fall Budget Update. It didn’t.

Finance Minister Billy “forgot-the-villa” Morneau, announced $14.9 billion in additional spending over the next four years. He is moving up the ‘enhanced child care benefit” hoping that it deflects attention from his numerous personal tax shelter benefits. He also announced a cut in the small business tax to 10% effective January 1, 2018.

The budget deficit narrowed but not from anything the government did. It was due to the surprisingly robust domestic economic growth. Prime Minister Justin Trudeau was reportedly telling everyone who would listen; “See, I was right. Budgets do balance themselves”.

The Canadian dollar traded at 78 cents to the US dollar on October 25 and could hit 75 cents before year end according to some technical analysts.

That is a pretty big move for risks that are merely “uncertain” which may limit Canadian dollar losses.

NAFTA may survive. There are powerful American lobby groups that want to keep the deal.

The US Chamber of Commerce said withdrawing from NAFTA will “do harm” to the American economy. US Farm groups, which include National Cattlemen’s Beef Association, National Pork Producers and National Corn Growers Associated are opposed.

The President of the Amercian Automotive Policy Council Matt Blunt “We certainly think a U.S.-specific requirement would greatly complicate the ability of companies, particularly small- and medium-size enterprises, to take advantage of the benefits of NAFTA.”

The quality of the American opposition to radically changing NAFTA terms suggests that cooler heads may prevail and an agreement worked out.

Oil prices are firm. Saudi Arabia’s Oil Minister Khalid al-Falih said the focus was on reducing oil stocks in industrialized countries to their five-year average. He even raised the prospect of prolonged output restraint.

The Bank of Canada has a tightening bias and the domestic economy is robust.

Governor Poloz may be driving the pace car around the track at the moment, but the entrance to pit row can come on any lap.

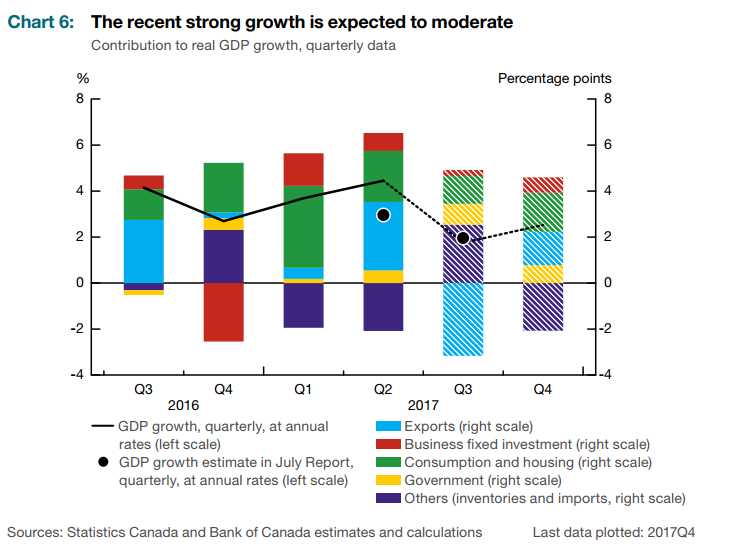

“Growth is moderating, not disappearing” Source: BoC MPR