By Michael O’Neill

Global trade tension headlines have roiled financial markets. The Bank of Canada, not so much. It’s not that they don’t care about existing and possible new tariffs, it’s that they are hard to assess. BoC Governor Stephen Poloz, at his press conference in Victoria, BC on June 27, was asked how the imposition of US tariffs affects monetary policy decisions? He answered, “when an individual tariff on a business sector, is incorporated into the BoC models, the net effect of the tariffs on the economy as a whole, is hard to figure out. “That is “bankspeak” for “I don’t know.” Mr Poloz went on to say “Some things will go up, some things will go down, and it depends on how companies and consumers respond.” He added, “if an action adds 25% to something, inevitably prices rise.” He admitted that the analysis was complicated but concluded that “inflation was likely to rise.”

The complicated analysis is why he emphasized that the BoC monetary policy was “data dependent, not headline dependent.”

Mr Poloz reiterated that the economy was close to capacity and inflation was in the 2% target range. An upside surprise to Canadian April GDP data (due June 29) would solidify the case for the “data-dependent” BoC to raise interest rates at the July 12 meeting.

The Bank of Canada may be a major factor in the value of the Canadian dollar, but it is far from being the only factor. Canada is a significant exporter of oil, and traditionally rising oil prices have supported the Canadian dollar. That hasn’t been the case for most of this year.

At the beginning of 2016, Opec engineered a production cut of 1.2 million barrels per day amongst its members and Russia. The aim was to rebalance the global market to reduce crude supply to its 5-year average. They nailed it. In May, Opec announced that global crude production was 20 million barrels below the target.

During that time and for much of 2018 oil prices climbed steadily. The 174 (ordinary) meeting of Opec in Vienna ended on June 22. They announced they would increase production by 600,000 to 1.0 mb/d. Many traders expected prices to collapse. It didn’t happen. Instead, WTI oil drifted inside a $63.00-$67.00 range until June 25.

Then President Trump got into the act. He is insisting that all nations that import Iranian crude should cease imports by November or they will face US sanctions as well.

Opec only raised production by 600,000 b/d. The potential loss of Iran’s 2.1 mb/d production would aggravate the supply/demand equation in favour of demand.

Oil production disruptions are already causing problems. Canada’s Syncrude plant lost power shutting in 350,000 b/d. Venezuela oil production is about 660,000 b/d below their contracted obligations according to Reuters. The loss of Iran’s 2.1 mb/d would exacerbate the supply situation.

Oil prices soared. WTI oil touched $73.69/b on June 28.

At this juncture, it appears that prices have a lot further to rise. The June 2017 uptrend is intact while prices are above $62.20, a level being guarded by support at $63.75. A decisive break above the $73.50 -$74.00 area, would target gains to $76.34, the 61.8% Fibonacci retracement level of the June 15, 2014-January 19, 2016 range. The 76,4% retracement level is $88.23/b.

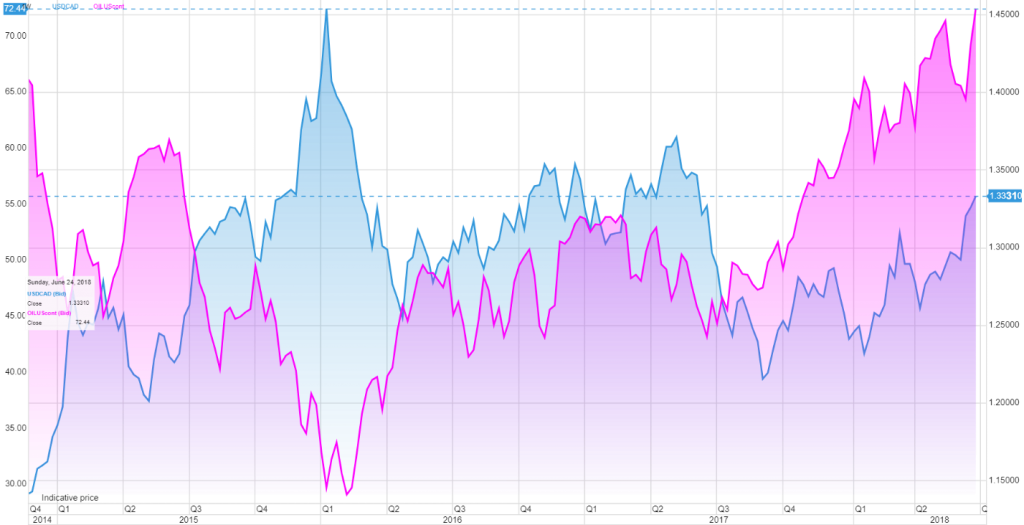

The Canadian dollar has not benefited from oil price gains since February. Oil prices have risen 25.6% while the Canadian dollar has lost 6%, in the same period. The following chart shows the correlation between oil prices and the Canadian dollar is broken. Over time, the relationship is self-correcting. A July 12 rate hike coupled with a hawkish statement could be the catalyst that brings the couple together again. If that happens and oil prices stay at current levels or move higher, the Loonie will soar.

Chart: USDCAD (blue line) Oil (purple line) 5-year, weekly

Source: Saxo Bank

Summer is only a week old. A broad swath of the northern hemisphere is in a heat wave, and school is out. Typically, it would mean the onset of the “summer doldrums.” This year, probably not, or at least not until President Trump takes an extended vacation and doesn’t have access to his twitter account.

The Bank of Canada may insist that it is data dependent not headline dependent, but the same can’t be said for FX markets.