By Michael O’Neill

The Bank of Canada door to lower rates is wide open, with the first interest rate cut expected in June. But before you rush in, they also gave a lot of reasons why the door could slam in your face.

The BoC did as most economists and analysts expected. They left the overnight rate unchanged at 5.0% and continued with quantitative tightening but adopted a modestly more dovish tone than on March 6. The Governor’s Monetary Policy Report opening statement was rather chipper. The BoC is forecasting GDP growth of 1.5% in 2024, a big increase from the December forecast of 0.8%, and expects inflation to drop to 2.2% (previously 2.4%) by year-end.

Rationale for a Rate Cut

Inflation is below target: The Bank of Canada aims to keep inflation at the 2 per cent midpoint of an inflation-control target range of 1 to 3 per cent. The key word is target. Inflation is on a downward trend and if CPI is lower than the 2.8% y/y result in February, the BoC could act.

Sluggish economic growth: The Canadian economy finished 2023 rather sluggishly. January’s GDP growth surprised to the upside, rising 0.6% while February’s growth is estimated at 0.4%. CIBC economists suggest that the growth is an anomaly due to the end of public sector strikes in Quebec and an easing of supply chain disruptions. If so, a June rate hike should be in the cards.

Weakening Job Market: Canada’s unemployment rate jumped 3 ticks to 6.1% in March. Notably, job losses in accommodation, and food services point to weak consumer spending which effects hiring plans. The BoC may not want to see unemployment rise too much further.

What’s the Hurry?

Neutral Rate of Interest increased: The BoC raised its neutral rate of interest by 25 bps to 2.25-3.25% (the rate where monetary policy is neither stimulating or restraining the economy), which suggests that Canadian rates may not fall as far as previously expected.

Government Budget April 16: The Trudeau administration, currently lagging in voter approval, appears poised to deploy a well-worn strategy—winning hearts (and votes) through fiscal generosity. This strategy is unveiling itself in an almost unprecedented pre-budget announcement spree. The lineup includes a boost in defense spending, broader daycare access, school meal programs, support for housing construction, and the establishment of a Rental Protection Fund. These are in addition to the already publicized Pharmacare and Dental plans. This wave of fiscal stimulus could tie the BoC’s hands, potentially deterring rate cuts to avoid an overheated economy.

Fear of Reigniting Housing Boom: Policymakers may be reluctant to cut rates due to fears it would overheat the housing market, which is already underpinned by heavy demand and scarce supply.

Economic growth: The BoC predictsthat economic growth will rebound to 1.5% on average in 2024, which is well above its 0.8% forecast in December. The BoC’s forecasting track record is rather poor and if GDP growth surprises to the upside, there would not be any need to cut rates.

What will Happen?

Economists at CIBC and RBC expect the BoC to cut rates in June due to Canada’s economic underperformance against the US, and because, in his press conference, Mr. Macklem, when asked about a June cut, said, “It is within the realm of possibilities.” He also injected a note of caution when he noted “We are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained. The further decline we’ve seen in core inflation is very recent. We need to be assured this is not just a temporary dip.”

Loonie Takes it on the Chin.

The Canadian Dollar took a sharp dive today, with USDCAD rocketing from 1.3558 to 1.3702, all thanks to a cocktail of spicy US inflation numbers and a dovish serenade from the Bank of Canada. The US inflation update came in hotter than the forecasts, with a March year-on-year climb of 3.5%, edging past both the predictions and the previous figures. Core CPI wasn’t far behind, nudging above expectations at 3.8%. It’s a clear signal that the inflation beast isn’t tamed yet, throwing cold water on any hopes for a Fed rate cut in June and hinting that 2024 might not be the year of cuts markets were hoping for.

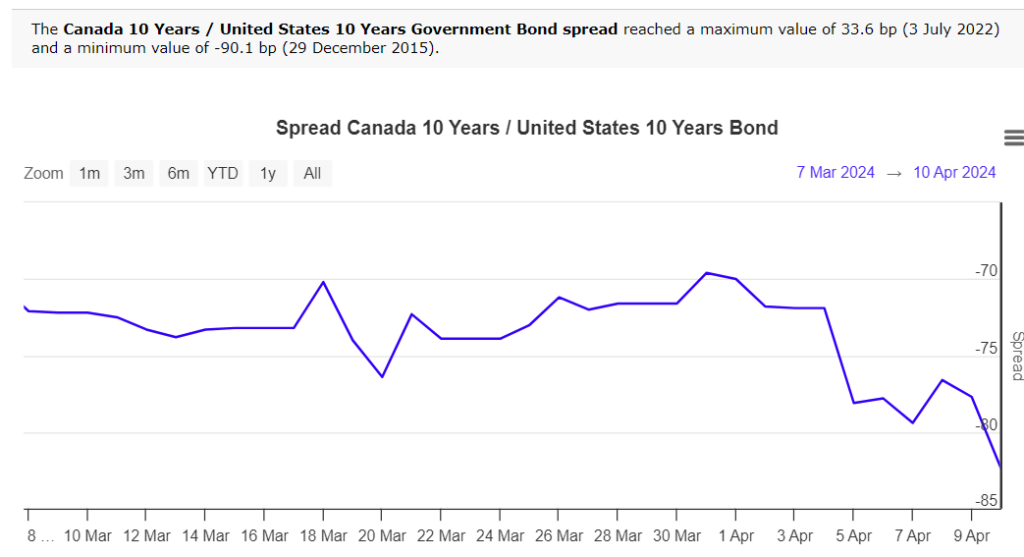

The dovish outcome from today’s BoC meeting was the final nail in the Loonie’s coffin. The 10-year yield spread between CAD and US bonds widened sharply to -82.4 and fueled the USDCAD rally. The mix of hot US inflation and a dovish BoC suggest USDCAD is likely to revisit 1.3860 while prices are above 1.3505.

The BoC may have opened the door to a June rate cut, but in the process, slammed it in the face of USDCAD bears.

Source: worldgovernmentbonds.ca