Captain America and three Easy Riders Photo: IFXA

By Michael O’Neill, Senior Analyst, Agility Forex

In Canada and elsewhere, interest rates are lower than they have been at any point in history. In financial markets, it is called “easy money”.

The theory is that lower interest rates encourage banks and lenders to loan money, thereby increasing investment and stimulating the economy.

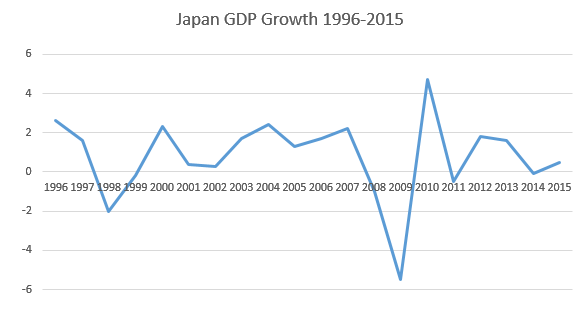

It sounds simple. Whether it works or not, is not so simple. Japan has been applying all kinds of fiscal and monetary stimulus packages for 20 years and has only had mixed success.

That doesn’t mean that Japan will stop trying.

Its not over until Haruhiko Kuroda sings

The Bank of Japan announced negative interest rates at the end of January. The goal was to stimulate consumption and investment. Predictably USDJPY strengthened. Unfortunately for Japan, the strength was very short lived. From a post announcement peak of 121.70, on January 28th, USDJPY declined steadily until it found a short term bottom at 107.76 in April.

Many analysts expected the BoJ to follow up the January move by announcing another “bigger and better” stimulus package at the April 28 meeting. They didn’t. USDJPY dropped anew and it finally found at bottom at 98.75, the British Brexit vote low.

You can fool some of the people some of the time and in FX, you can fool some of the traders all of the time.

USDJPY rallied from the 98.75 to 107.36 in July, buoyed by the government of Japan’s plans for a ¥28 trillion fiscal stimulus plan. At the time, many in the market believed that at the July 29th meeting, the BoJ would inject another round of monetary stimulus to complement the government’s fiscal stimulus. In boxing parlance, a one-two punch, with the knock-out blow being another cut in interest rates, which were already negative.

That didn’t happen.

The BoJ announced that they were doubling the purchases of exchange traded funds and a review of its policies. The governor, Haruhiko Kuroda said that the BoJ would conduct a thorough assessment of the effects of its negative interest rate policy and asset buying program. All traders heard was “it’s not working” and they sold USDJPY.

The Bank of Japan may be seeking assurances that its monetary stimulus program is effective but the Bank of England has no such concerns.

On Thursday, the BoE made the first cut to interest rates since 2009 while announcing a new round of stimulus measures. The Bank Rate was cut to 0.25% from 0.50%, the quantitative easing program was expanded to the tune of £60 billion and there is a brand new £10 billion high quality corporate debt purchase program.

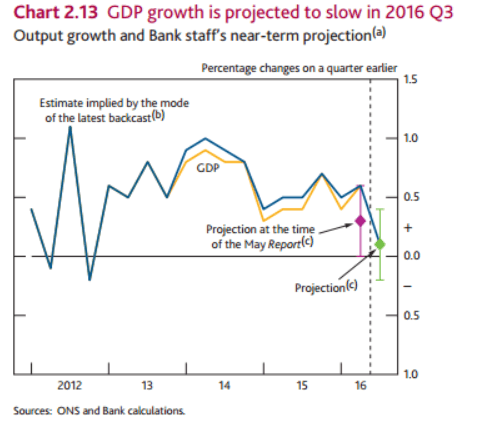

According to the Bank of England Governor, Mark Carney, the UK’s decision to leave the European Union marked a regime change. The huge reduction in the GDP growth forecast for 2017 to 0.8% from 2.3% predicted in May, prior to the Brexit vote, is evidence of that change.

Source: Bank of England

The BoE may be in stimulus mode, but across the channel, the European Central Bank is content to “wait and see”. The ECB launched a massive stimulus program in March and as of two weeks ago, ECB President, Mario Draghi, was content to monitor the impact of the new measures. As for any Brexit fall-out, they will await updated forecasts, which will be ready in September.

Canada was fashionably late to the stimulus party, albeit earlier than the UK. The government of Canada announced a $30 billion stimulus program in March which was meant to jumpstart a moribund domestic economy. The Bank of Canada on the other hand , chose to stay on the sidelines and didn’t add any monetary policy stimulus to the mix.

The ECB, BoJ and BoE embarked on stimulus programs to alleviate or rejuvenate sluggish economies. China is in the same boat, attempting to engineer a soft landing. That is three of the top four global economies struggling to boost growth.

While these economies are slowing, the US economy is chugging along. It has reached a point where the Federal Open Market Committee is contemplating raising interest rates.

Contemplating is likely all the FOMC will do, at least until December. The prospect of a renewed slowdown in G10 economic growth will provide the FOMC members with all the ammunition they need to support leaving rates unchanged at the September meeting.