By Michael O’Neill

Deutsche Bundesbank, Germany’s central bank finds itself it the middle of a spat between the European Court of Justice and the German Constitutional Court. The German court found that the European Central Bank may have over-stepped its mandate when Mario Draghi and crew initiated quantitative easing, in 2015. The court ruled “The ECB fails to conduct the necessary balancing of the monetary policy objective against the economic policy effects arising from the program. Therefore, the decisions at issue…exceed the monetary policy mandate of the ECB.” That finding contradicts the European Court of Justice ruling in December 2018, that said PSPP did not exceed the ECB mandate or infringe on European Union law.

Both sides are singing “Street Fighting Man” and EURUSD bears are growling.

Things are different on the other side of the Atlantic. When the Bank of Canada has a Tiff, all it means is that Mr Dean”Tiff” Macklem is in the house and as of June 2, Mr Macklem is the Governor. He has big shoes to fill, but fortunately they are his own. Mr Macklem worked for the BoC since 1989 as the Senior Deputy Governor from July 2010 to May 2014.

There is no doubt that Mr Macklem is eminently qualified. He was in the thick of the Bank of Canada response to the 2008 financial crisis, and his knowledge and insight went a long way into feeding Mark Carney’s “rock-star banker” legend.

There is no doubt that Mr Macklem is eminently qualified.

There is no question about his talent, but his independence is a cause for concern. He appears to be too closely aligned with the Trudeau government and their controversial climate change agenda. In fact, he was the Chair of the Expert Panel on Sustainable Finance, appointed by Finance Minister Bill Morneau, and former Minster of the Environment Catherine McKenna.

The final report was released last June. It was a bureaucrat’s dream advocating the creation of various, study groups, committees, councils, and centres, while defining, recommending, promoting, supporting, aligning, and accelerating a host of vague objectives, goals, and standards. The report said that “Finance is not going to solve climate change, but it has a critical role to play in supporting the real economy through the transition.”

And that’s the scary part. How will Mr Macklem align his conclusions in the Sustainable Finance report with the Bank of Canada’s key goals of low inflation, and stable currency, in a post-Covid-19, bloated deficit, high unemployment world?

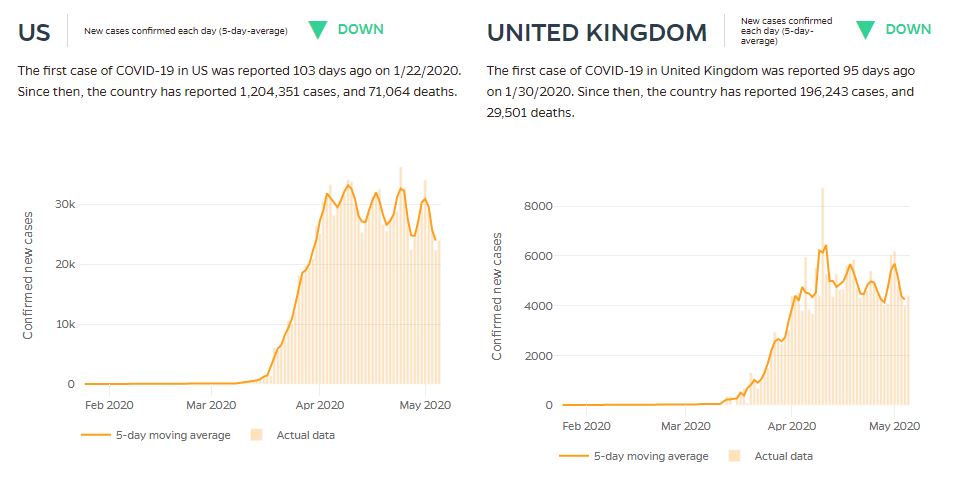

Global investors are not concerned-yet. They continue to be focused on the phased-easing of lock-down restrictions in the major centres. Governments are trying to reopen their economies in the face of mounting business closures, soaring unemployment, and somewhat declining numbers of new COVID-19 cases.

Graph: 5 day moving average of daily confirmed new cases

Source: John Hopkins University of Medicine

Canadian Economic forecasters have been working over-time calculating, then re-calculating economic growth forecasts. On May 1, Bank of Montreal predicts a whopping 44.0% drop in Q2 GDP, followed by an even more spectacular rebound of 62.0% in Q3 and a 2020 annualized rate of negative 6.0%. TD Bank is more optimistic. On April 20, they predicted a 42.0% plunge in Q2 GDP followed by a Q3 rally of 3.6%. The Bank of Canada decided to skip the entire forecasting rigmarole, due to the uncertainty surrounding the outlook. The one thing they agree on is that Q4 2020 will look a lot better than Q2 2020.

Australia and New Zealand are taking steps to re-open their economies, while isolating themselves from the rest of the world. The two governments are planning a “Trans-Tasman Travel Bubble” to take advantage of the COVID-19 curve flattening in both countries. Australia is New Zealand’s largest source of tourists, followed by China, US, and the UK. Nevertheless, NZ Prime Minister Jacinda Ardern, is in no hurry to open the borders to anyone other than Aussies. The antipodean economies were early victims of the pandemic and consequently are ahead of the curve in terms of recovering. The Australian and New Zealand currencies climbed steadily since the middle of March led by an 18% gain in AUDUSD, underpinned by hopes their economies will begin to normalize rapidly.

The Canadian dollar is not in that boat; it is still taking water.

The Canadian dollar is not in that boat; it is still taking water. The coronavirus pandemic decimated the domestic economy while the oil price collapse trampled on the ashes. West Texas Intermediate (WTI), the North American benchmark price for crude soared an impressive 137% since April 28. Unfortunately for Canadian producers, even with the sharp narrowing of the spread between WTI and Western Canada Select, (WCS) the price is well-below break even for most producers.

Friday’s Canadian employment report forecasts suggest job losses of 4.0 million and an unemployment rate of 18%. Those jobs won’t be coming back anytime soon, and with chances for a resurgence in COVI-19 cases, Canadian economic risks, and the Canadian dollar outlook, are skewed to the downside.

Incoming BoC Governor Macklem does not officially take the helm until June 2, so if traders have any tiff with monetary policy, it is with outgoing Governor Stephen Poloz.