By Michael O’Neill, Agility FX Analyst

The state of central bank forward guidance and oil producer announcements can be summed up in three words; fairy tales and hallucinations.

Oil prices have been erratic since the beginning of June. Supply disruptions due to attacks on Nigeria’s oil industry combined with US crude inventory draw downs and bullish forecasts from OPEC drove WTI from a low of $26.00/ barrel in February to $51.60/b in June. By month end, the rally had run out of gas (pun intended) and oil prices started to decline.

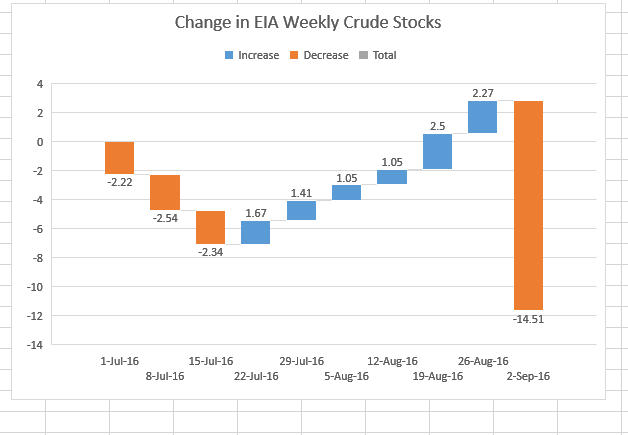

Previous bullish information became bearish. In June, the Energy Information Administration (EIA) Crude oil stocks change reports showed US inventories declining and traders bought oil.

In July, that sentiment turned. Weekly oil stocks declines were ignored and oil prices went lower. That was partially due to the EIA continuing to say that oil inventories remained at “historically high levels for this time of year”.

EIA Crude Stocks change from July 1-Sep 2 Source: EIA and IFXA Ltd

WTI prices bottomed out at the beginning of August. News that Russia was promoting a non-Opec/Opec meeting in Algiers to discuss production caps caused a flurry of buying. On September 5, Russia and Saudi Arabia announced an agreement to cooperate in world oil markets. They didn’t say when or how but oil traders didn’t care. Oil prices rallied further. Even news that Iran has no intention in participating in any production cap agreements until it has achieved pre-sanction levels, failed to dampen the enthusiasm of the oil bulls.

Western oil production is not state owned and there are laws against price fixing. The US and Canada are two of the top five oil producing nations and they are excluded from the production cap discussions. Furthermore, Opec has a long history of establishing and then ignoring production limits. Why will this time be any different.

Expecting oil prices to rally based on mere promises by a couple of producers to “cooperate”, in an enviroment where the major G20 economies are experiencing sluggish economic growth, appears to be more of a hallucination than a recipie for sustained gains.

Fairy tales are stories of fantasy. You can find them at any library and lately within many central banks. The European Central Bank (ECB) delivered one such story on September 8. The ECB left policy on hold and hinted at an extension of the quantitative easing program beyond March 2017, painting a picture that suggests everything is unfolding as expected. Except it isn’t. The ECB trimmed their GDP growth rate, inflation remains low and the real impact of the UK’s decision to leave the European Union remains unkown.

The Bank of Canada (BoC) policy statement on September 7 didn’t start with “once upon a time” but it was a fairy tale nonetheless. The BoC said that it believes that global growth will strengthen gradually in the second half of the year. That belief differs from the Reserve Bank of Australia who wrote on September 2 that the global economy is continuing to grow at a lower than average pace, noting more difficult conditions in emerging markets. In July, the BoC projected that the Canadian economy would grow at 3.5% in the thrid quarter. On September 7, the third quarter growth rate wasn’t mentioned.

The BoC noted that CPI inflation was below the 2% target an observation that they have been making for the past four years. Previously they suggested that inflation would get back to the target level at some point in the future but apparently have dispensed with that notion.

And then there is the Fed. The august members of the Federal Open Committee have spouted an entire series of fairy tales. Various fed speakers have delivered a confusing and often-times contradictory array of comments that have completely obscured the US rate outlook. The FOMC members seem confident that interest rates will increase by year end. Sixty percent of Fed futures traders don’t believe them.

The Canadian dollar outlook is a bit of both a fairy tale and a hallucination. The hallucination is that oil prices will rebound by Opec introducing production caps. The fairy tale is that USDCAD will decline to the 2016 low. Expecting sharply higher oil prices and a rebounding domestic economy despite seasonal US dollar demand, including repatriation flows and the risk of a US rate hike is rather Cinderella-ish.