Source: IFXA

By Michael O’Neill

Fed Chair Jerome Powell spoke, and markets did not like what he said. More accurately, it was their interpretation of Mr Powell’s comments they didn’t like.

The FOMC statement didn’t say anything overtly hawkish or dovish. Both camps were able to find enough evidence to support their views but positioning for a pivot won the day.

The Fed raised the overnight rate by 75 bps, taking the top of the fed funds band to 4.0%, a move that was almost universally expected. The FOMC statement was identical to the one from September except for one paragraph making reference to cumulative rate hikes and their lagging effect on the economy.

The result was predictable. The US dollar soared, equities sewered, and the 10-year US Treasury yield popped to 4.09% from 4.00%.

However, Mr Powell’s press conference roiled markets like ex-lax ladened food at a Chili Festival.

Huh! What about pivot? He didn’t say anything about a pivot.

Photo: hdclipartall.com

There was plenty of anticipation ahead of the November 2 FOMC meeting and many traders and analysts had worked themselves into a lather hoping the Fed would open the door to a slower pace of tightening. It didn’t happen.

Mr Powell kicked-off his press conference saying, “My colleagues and I are strongly committed to bringing inflation back down to our 2 percent goal.”

He also put the boots to rate pivot notions saying, “We still have some ways to go, and incoming data since our last meeting suggest that the ultimate level of interest rates will be higher than previously expected.”

That was not what markets wanted to hear. The stampede out of stocks, bonds, commodities and into US dollars left a river of red ink across the globe.

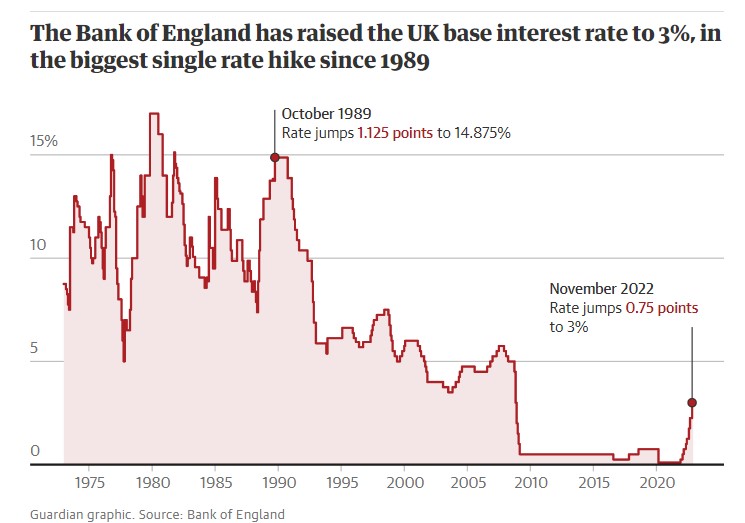

And the Fed isn’t even the most aggressive inflation-fighting superhero. The Bank of England BoE) wins that cape after they raised their benchmark rate by 75 bps to 3.0%. That’s because the UK economy is already in a recession and is in far worse shape that the US. Hiking interest rates in that environment is like throwing gasoline on the fire.

Source: UK Guardian

The Fed and BoE don’t appear to have any interest in pivoting until inflation is firmly on track to reach their 2.0% targets.

The Bank of Canada has already pivoted once. Will they pivot again?

The BoC surprised markets with its “dovish” 50 bps rate hike on October 26 despite earlier policymaker comments, data, and the Business Outlook survey suggesting another 75-bps hike was warranted.

The BoC was one of the first central banks to recognize that inflation increases were becoming problematic and raised the overnight rate to 0.50% in March 2022. Aggressive, it was not. The overnight rate was 0.25% so raising rates by 25 bps was rather useless if the goal was to temper rising prices.

The BoC has since raised the overnight rate to 3.75% but inflation isn’t showing much evidence of cooling. In September inflation rose 6.9% y/y while Core-CPI (excluding food and energy) rose 5.2% m/m.

Governor Macklem argued that the 50 bp bump was warranted. The BoC has increased rates 350 bps since March, and he said he is attempting to balance the risks between under and over tightening.

He may have a point. It takes a lot of time for rate hikes to work its way through markets. Economists believe it takes between nine months and two years for rate hikes to have an effect. Former US Treasury Secretary Larry Summers described the lag like being in a shower when there is a 20 second wait between turning on a faucet and when the temperature changes. In between you can scald or freeze yourself.

Mr Macklem said Canadian rates were still going higher in testimony to the Senate Committee on Banking saying, “We also expect our policy rate will need to rise further.”

The Bank of Canada may have been one of the first off the mark in the rate hike sweepstakes but has been overtaken by the Fed and that has inflation consequences of its own.

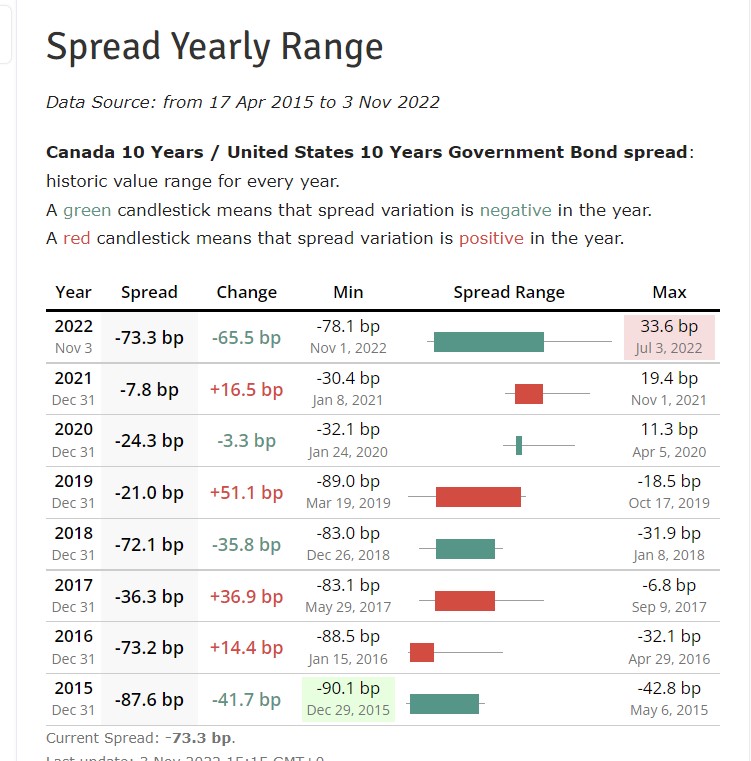

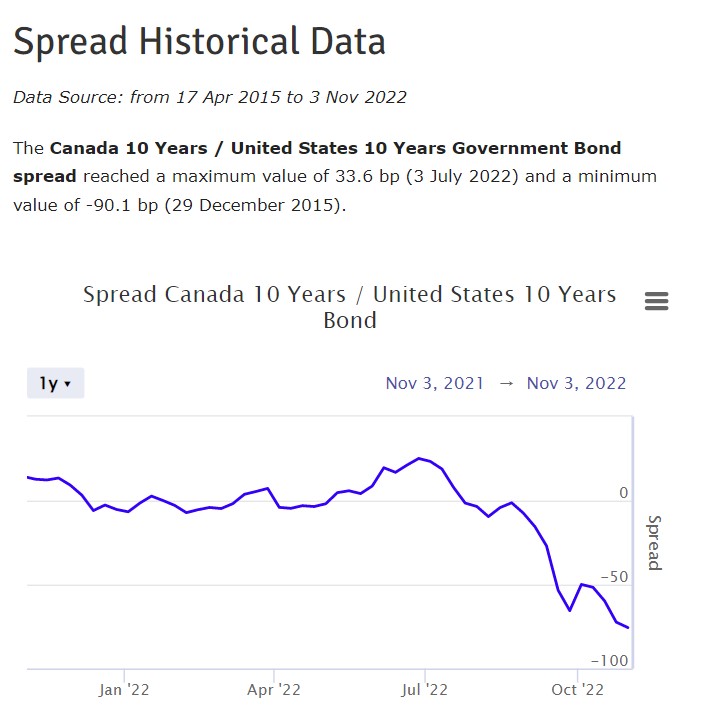

The Canada and US 10-year government bond spreads has widened sharply in favour of the US. That makes Canadian investments less attractive and imports inflation via a weaker Canadian dollar.

Source: worldgovernmentbonds.com

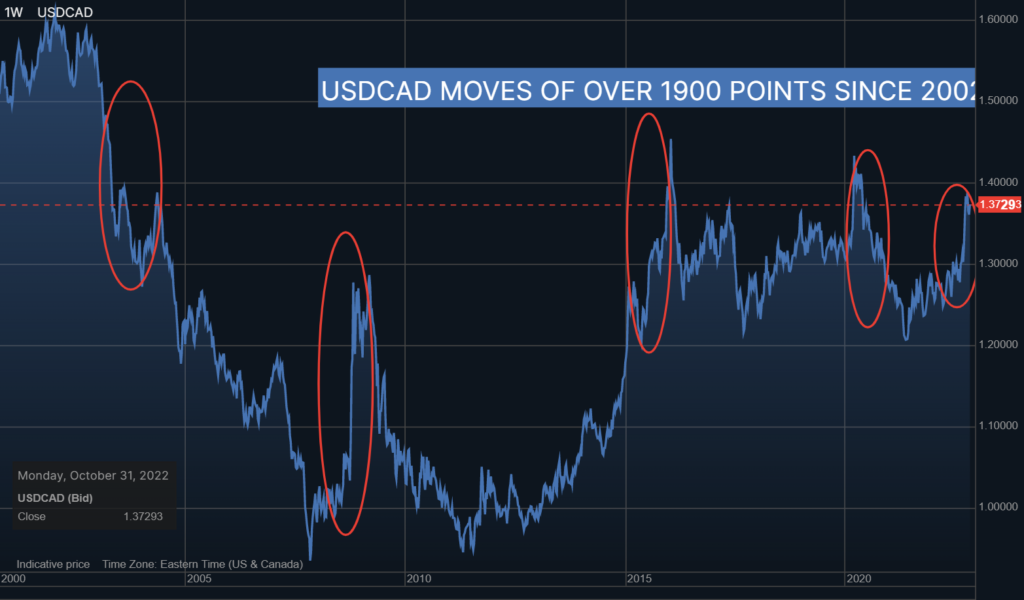

Since 2015, the widest CAD/US spread has been 90.1 points in favour of the US and USDCAD climbed 1900 points that year. The spread, as of November 3 is 73 points.

USDCAD has traded in a 1550-point range in 2022 (1.2410-1.3980) which is the fifth largest range in the past 20 years.

Further USDCAD gains above 1.4000 may be hard to achieve, at least until the end of the first quarter of 2023 especially if the BoC matches Fed rate hikes and oil prices remain above $80.00/barrel.

The sum of all rate hikes and the time they take to meander through the economy will determine the pace of future US rate hikes and by default the direction of the Canadian dollar.

Chart USDCAD weekly for 20 years highlighting significant USDCAD ranges

Source: Saxo Bank