By Michael O’Neill

The Merriam-Webster dictionary defines “a gray area” as: an area or situation in which it is difficult to judge what is right and what is wrong. If the Federal Reserve, Bank of Canada, and Reserve Bank of Australia, slashed interest rates because of fear about potential impacts to economic growth from the coronavirus (COVID-19), their decision would be in a “grey-area.

They did. It is.

The RBA was first off of the mark. On March 3, they cut the Overnight Cash Rate by 25 basis points to 0.50%. They justified their actions saying “The coronavirus outbreak overseas is having a significant effect on the Australian economy at present, particularly in the education and travel sectors,” suggesting it would affect domestic spending and weaken Q1 economic growth.

Later that day, the G-7 Finance Ministers and Central Bank Governor’s released a statement saying they are closely monitoring the spread of COVID-19, and its impact on markets and economic conditions.”

The Federal Reserve monitored the outbreak so closely that they decided to act immediately, rather than wait for their regularly scheduled meeting, March 17-18. They slashed rates by 0.50%, lowering their target range for federal funds to 1.0-1.25% percent.

During the press conference, Fed Chair Jerome Powell said the US economic fundamentals “remain strong, unemployment near half-century lows, and the pace of job gains as “solid,” which has underpinned spending. You are forgiven if you thought he was justifying a rate hike. He claimed that the virus and measures to contain it would “surely weigh on economic activity.” He noted that the outbreak caused significant movements in financial markets and that they were beginning to see its impact on travel and tourism.

What he didn’t say was “here is the data to support our actions” All Fed officials claim that monetary policy decisions are “data-dependent.”

Wall Street traders were not impressed. Their initial reaction knocked the Dow Jones Industrial Average (DJIA) down 2.94% by the end of the day and by the close on March 5, the benchmark index was down 8.47%.

The next day, the Bank of Canada mirrored the Fed’s move, cutting the overnight rate to 1.25% from 1.75%. The last time the BoC trimmed rates by 0.50% was in March 2009, suggesting there was some “showmanship” with the magnitude of the cut. It seemed like it was designed to show that the BoC Governing council had the economic pulse of the country and could act decisively. Governor Stephen Poloz admitted as much when he said “Many of the implications of COVID-19 lie beyond the influence of monetary policy.”

Mr Poloz explained the decision on March 5. He pointed out that that business investment had fallen short of expectations for the past three years, and that six-months ago, the BoC saws signs that the US/China trade war weighed on exports and investment. Last October, they toyed with cutting domestic interest rates because of slowing growth but decided against such a move due to fears of increasing financial vulnerabilities. Those vulnerabilities are focused on the housing market. The January Monetary Policy Report said, “stronger housing activity also means more household debt, of course, which continues to be Canada’s biggest financial system vulnerability.”

On March 4, the BoC shoved financial market vulnerabilities to the back burner. Mr Poloz said “the downside risks to the economy today are more than sufficient to outweigh our continuing concern about financial vulnerabilities”.

He has a point. If manufacturers can’t get parts, or retailers can’t get inventory, because of coronavirus supply chain disruptions, private sector job losses are sure to rise. If you fear for your job, you are unlikely to strap on a mortgage or buy a new car. Furthermore, the Indigenous railway blockade over pipeline access and unreconciled reconciliation promises and the cancelation of a series of energy mega-projects, underscore the risks to the domestic economy. Teck Resources Frontier project, Meg Energy’s oilsands expansion, and Warren Buffet’s Saguenay LNG project abandoned investment plans due to an “unstable investing environment.”

3.8 million Canadian public sector workers don’t have those risks. They have jobs for life. They do not have any concerns about saving for retirement, regardless of interest rate levels. Falling stock markets, wiping 10, 20 or even 50% of an RRSP’s value is of no concern either. Their guaranteed pensions will rise every year, even in retirement. To paraphrase Winston Churchill: “Never have so few, received so much, by so many.”

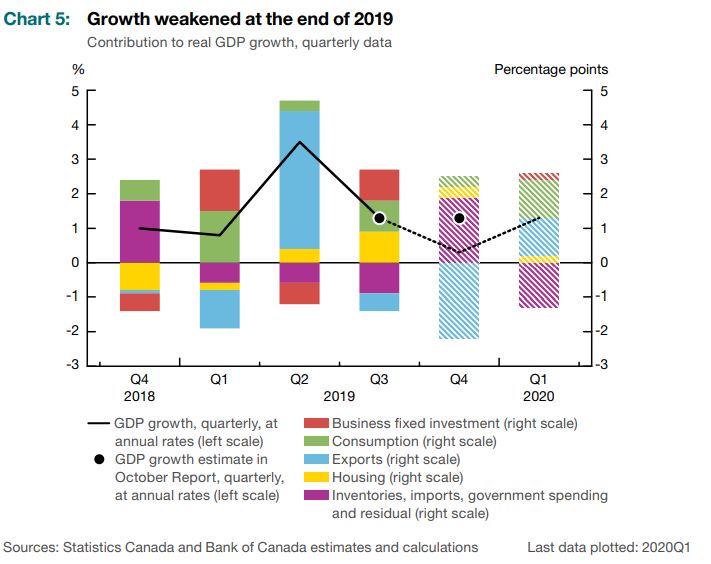

The BoC’s January forecast for an uptick in growth GDP growth in Q1 2020 will be downgraded

Source: BoC January MPR.

Perhaps its time for a system reboot.

The Canadian dollar appears to be recalibrating. Two months ago, USDCAD probed support in the 1.2950, which led to speculation for additional losses to 1.2500. At the time, China and the US were getting ready to ink a trade deal, WTI oil prices were well-above $60.00/barrel, and US equity indexes were at a record levels.

A few sneezes later and the world has gone to hell in a coronavirus basket. WTI lost over $20.00/barrel, and the DJIA is lower than it was at the start of the year. USDCAD climbed to 1.3465 before consolidating in a 1.3240-1.3440 range. The long-term uptrend from October 2012 (monthly chart) is intact above 1.3000. A decisive break above 1.3450-80 area targets 1.3550 and then 1.3660.

Things may not be looking so good for the Loonie, but noted English clergyman Thomas Fuller once said: “the darkest hour is just before dawn.” Dawn for USDCAD happens if Opec and Russia agree to an additional 2.0 million barrel/day production cut that shores up oil prices. Dawn is also when China economic growth recovers after recent health measures battle COVID-19 into submission. Dawn is another 50 Shades of Gray area.