Meme: imgflip/IFXA Ltd

By Michael O’Neill

Bad guys had a bad day when they broke into John Wick’s house, stole his car, and killed his puppy. Seventy-seven villains met their demise when Mr Wicks sought retribution.

Financial markets are not as bloody, but red ink will flow if markets ignore the Fed’s veiled rate hike warnings in the minutes from the June 16 Federal Open Market Committee (FOMC) meeting.

The minutes did not come right out and say interest rates were going up. That would be too easy, which explains why the minutes contained nearly 10,000 words on fourteen pages. However, the Summary of Economic Projections was pretty clear about the direction of Fed Funds in 2023.

The FOMC minutes noted, “a vast majority of participants revised up their projections for real GDP growth this year,” compared to March, due to stronger consumer demand and improvements in vaccination rates.”

Policymakers were optimistic about the business sector, noting that the sectors most impacted by the pandemic were rebounding. Many industries were suffering from a shortage of materials and labor, and some of them planned to offset those issues by raising compensation and raising prices. They didn’t say if the higher compensation and higher prices were transitory.

Policymakers admitted guessing wrong on inflation. “However, participants remarked that the actual rise in inflation was larger than anticipated, with the 12-month change in the PCE price index reaching 3.6% in April.”

They tempered their enthusiasm for insisting inflation increases were “transitory,” noting “several participants remarked that they anticipated that supply chain limitations and input shortages would put upward pressure on prices into next year.”

That begs the question of “when does transitory become “entrenched?”

The FX reaction to the minutes suggesting Fed tapering will soon be a thing was to buy US dollars.

That makes sense, as tapering will eventually lead to a rate hike.

The Bond market reaction was a bit of a “head-scratcher.” Traders bought bonds and drove 10-year yields down to 1.25% from 1.48% the day before. Why would yields drop if interest rates would be rising?

The answer may be as simple as yesterday’s price action not having anything to do with the FOMC minutes.

Analysts blame the surge in bond prices and plunging yields to safe-haven demand, rising Delta variant coronavirus cases worldwide, falling oil prices, and fading euphoria from US fiscal stimulus.

Another school of thought is that the bond volatility is due to fears the US will run into the legislated debt ceiling limit on August 1. (The debt ceiling is the maximum debt that the US Treasury can incur).

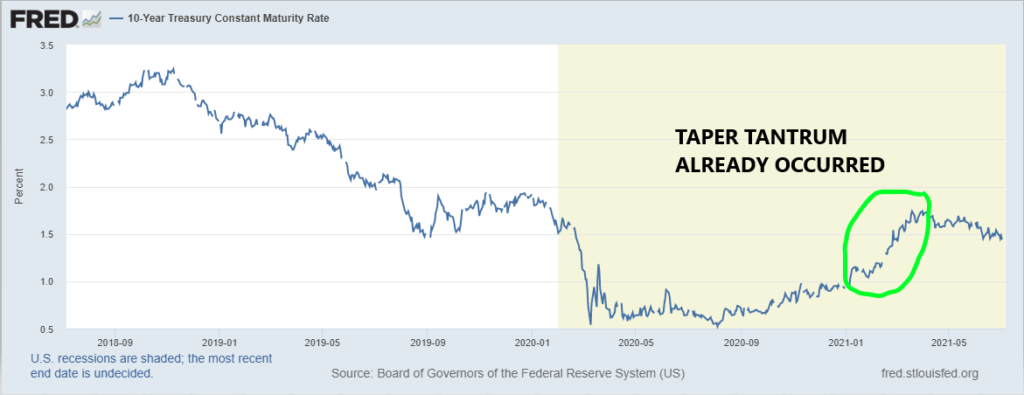

The bond market had its tantrum five months ago.

Source FRED

Treasury yields rose from 1.02% in February to 1.74% in April after Fed Chair Powell indicated that the FOMC would allow inflation to run hot. The pace of US vaccines was starting to pick up, and traders feared the Fed’s promise to keep interest rates super-low, would send consumer prices soaring. Yields consolidated the gains in a 1.42%-1.58% band during June.

The latest dip in yields may be more a factor of stale but weak long bond positions getting squeezed out rather than a view on inflation risks.

Cynics among us may believe the Fed (and other central banks) deliberately muddle their message to maintain an aura of mystery to bolster their credibility while remaining just as confused as the rest of us.

The Fed exists for two reasons. Their website says, “Our two goals of price stability and maximum sustainable employment are known collectively as the “dual mandate.”

The Fed tweaked its inflation mandate on January 26, 2020. Instead of a 2.0% annual target, the “Committee seeks to achieve inflation that averages 2 percent over time.” The Fed’s performance vis a vis the 2.0% benchmark is easily judged. They either hit the target or miss. The latest inflation tweak is a vague, floating number with an unquantifiable duration. Now, everything is a bullseye.

The Fed’s inflation tweak looks like a hard-target compared to their employment mandate. They admit that their goal of maximum sustainable employment is a mirage. The Fed website says, “Many nonmonetary factors affect the structure and dynamics of the labor market, and these may change over time and may not be measurable directly. Accordingly, specifying an explicit goal for employment is not appropriate.” Yessirree Bob, our goal is maximum sustainable employment, but we do not know what that is”

And if that wasn’t vague enough, the FOMC statement describes the employment as the “Committee’s broad-based and inclusive maximum employment goal.” Inclusive? What does that mean? You are a worker, or you are not a worker.

The FOMC minutes signal that tapering is on the agenda, inflation may be more persistent than expected, and rate hikes are coming down the pipe. The pace of dual COVID-19 vaccinations in the developed world suggests the coronavirus may downgrade to a nasty flu, leaving the pace of economic growth to accelerate.

If so, bond bulls may feel like they robbed John Wicks.