Photo: Wikimedia commons

By Michael O’Neill

Dollar bears are running wild, and gold is rocking. Gold (XAUUSD) soared 36% since March 19 as FX traders soured on the US dollar. The shiny metal trades at record highs and has its sight set on the $2000.00 level. There is nothing special about that price-its just another number followed by three zeros. Prices are not only going to hit that level; they will blow through it.

It may take a couple of weeks or even a couple of months, but higher gold prices have the tacit blessing of the G-7 central banks. Collectively, they all adopted, near-zero, zero, and negative interest rate policies. In days of yore, owning gold was considered an aggressive strategy as the buyer did not earn any interest.

That’s not true today, and if Fed Chair Jerome Powell is to be believed, US interest rates, for one, are not going higher any time soon.

He said “we aren’t even thinking about higher rates. The economy will need our continued support for an extended period,” in answer to a question at the July 29 press conference.

Savvy investors realized that early and helped propel record inflows into gold-backed exchange traded funds (ETF’s). Low interest rates are a big part of the reason for the demand, but not the only reason. Social unrest and the resurgence of the coronavirus in the US, along with trade risks and geopolitical tensions, are also supporting prices.

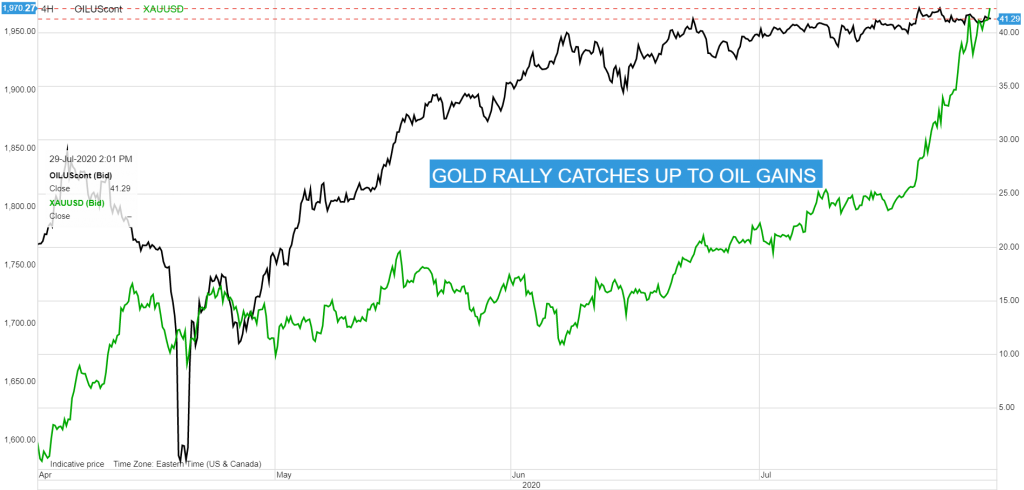

The gold price rally from March is impressive, but it pales in the face of the massive jump in crude oil prices. Saudi Arabia’s declaration of an oil price war decimated the crude market in the first 4 ½ months of the year. West Texas Intermediate, for May delivery, dropped to negative $37.63/barrel on April 20. It may have been to a technical issue around expiring CBOE contracts and storage, but somebody took a beating. Sanity returned. News of oil peace talks, followed by aggressive production cuts, boosted prices from April’s depths to $42.30/b, July 23.

Chart: WTI oil and gold

Source: Saxo Bank

The Australian dollar was the best performing currency since the pandemic depths of March. AUDUSD jumped 31% since March 18, touching 0.7197 on July 29, following the FOMC meeting. Coincidently, Australia produces 312.2 ounces of gold per year, making it the 2nd largest gold producing country.

If gold were an 80’s era rock band, Fed Chair Jerome Powell would the front man, albeit without the hair, and spandex. The Fed’s performance in March was uber-aggressive, unprecedented, and expensive. They cut rates twice, taking Fed Funds from 1.50% to 0.25%, and delivered $2.3 trillion in economic stimulus programs. It was also successful. The actions put a floor under the free-falling economy.

However, the economy has yet to get back to pre-pandemic levels, and renewed outbreaks in many US states, suggest a recovery is a long way off. The Fed is unsure about how the recovery will take shape. They admitted as much in the latest FOMC statement.

In June, they said, “The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term.” This time they injected another layer of uncertainty, adding “The path of the economy will depend significantly on the course of the virus.”

The Fed is in full quantitative easing (QE) mode. They committed to buying Treasuries and Mortgage-Backed Securities to the tune of $120 billion per month. The Fed Chair acknowledged that the economy would need support for an extended period.

The Feds promise of low interest rates, QE, and rising COVID-19 cases, gave FX traders the green light to sell US dollars. EURUSD rallied to 1.1795 from a post-statement low of 1.1758 and AUDUSD is back at March 2019 levels.

Meanwhile, north of the border, USDCAD struggles to break support in the 1.3310-30 area. This currency pair’s performance lagged that of the other commodity bloc currencies, AUDUSD and NZDUSD. Part of the reason may be found in Ottawa, where the government’s coronavirus spending is 60% higher than Australia’s.

Another reason is that AUDUSD is linked with gold price movements while USDCAD is tied to crude. Gold prices are expected to keep rising while supply/demand imbalances will limit oil price gains. Just over a month ago, Fitch ratings downgraded Canada’s debt rating to AA+ from AAA, while Australia still has its AAA rating.

Canada still has a major advantage over Australia.

Canada is attached to its largest trading partner, and around 90% of Canadians live within 160 kilometers of the border. Australia is over 8,000 kilometers across the open sea to its largest partner, China.

And that may mean, Canadian dollar gains catch up to its antipodean counterpart.

The USDCAD technicals think that is a possibility. They are bearish below 1.3530 with a decisive break below 1.3530, and a decisive break below 1.3300 could put 1.2000 in play.

Gold may be rocking, but US dollar bears and a dovish Fed may see USDCAD take center-stage.