Photo: ABCNews

By Michael O’Neill

We’re eight months into 2022, and things look a whole lot different than they did in January.

At the end of 2021, n economist at a major bank wrote that the US dollar was about 14% above fair value and predicted several years of US-dollar weakness. He noted that the US had a diminished capacity for fiscal spending and that global and China risks were reflected in the price. He also believed in the guidance coming out of the Fed.

Another major global investment bank optimistically predicted,”2022 will be the year of a full global recovery, an end of the global pandemic, and a return to normal conditions we had prior to the COVID-19 outbreak. We believe this will produce a strong cyclical recovery, a return of global mobility and strong growth in consumer and corporate spending, within the backdrop of still-easy monetary policy.”

Oops.

To be fair, forecasting is binary-You are either right or wrong. The above forecasters may have missed the mark badly, but their analysis was sound due to the existing data and central bank guidance.

However, there is no excuse for the abysmal performance of the G-10 central banks. To say they “sucked” would be charitable.

Fed Chair Jerome Powell believed inflation was transitory due to supply-chain bottlenecks after global economies reopened following pandemic measures. The Bank of Canada, the Bank of England, the European Central Bank, and the Reserve Banks of Australia and New Zealand seemingly cut and pasted FOMC statements, then tweaked them for their respective audiences.

They should have known better.

They knew Russia had designs on Ukraine. On November 10, the US reported Russian troop movements on the Ukraine border, and by the end of the month, 92,000 Russian soldiers were on station. On December 17, President Biden warned Putin of “strong economic and other measures” if Russia invaded Ukraine. Russia was the second largest oil producer in 2021, which should not have been unknown to central bank economists.

The central bankers knew China was still dealing with aftershocks from the covid pandemic in January when authorities were locking down cities ahead of the Beijing Olympics.

Why did central bankers think aggressive lockdowns would not continue to negatively impact supply chains in the country known as the “World’s Factory.”

Central bankers also believed that the inflationary impact from consumer spending on cars, restaurants, hotels, and travel would “peter out.” They dismissed other analysts who suggested consumer demand had legs as they were sitting on a mountain of cash and were tired and bored of living frugally during the covid era.

When inflation started to tickle the 1978 Great Inflation Crisis levels, Jay Powell, Tiff Macklem, and the Bank of England’s Andy Bailey were forced to act.

The Bank of England was first out of the gate with a series of 25 bp rate increases which took the overnight rate from 0.10% to 1.75% by August. 4.

The Fed was slower off the mark and didn’t hike the fed funds rate until March, then got progressively more aggressive, taking fed funds to 2.25%.

The Bank of Canada won the gold star for aggressiveness after bumping rates 100 bps on July 13, which matches the Fed funds rate. BoC officials took to Twitter on August 25 to try to convince Canadians that they are not a “bumbling band of incompetents.” I’m not convinced.

Despite all the hikes and “born again” inflation fighting rhetoric from the central bankers’, traders seemed to believe they were “just kidding, right.” It took Powell’s Jackson Hole speech to convince them otherwise.

But despite the mid-August carnage, the S&P 500 is still 3.55% higher than June 15, when the Fed hiked rates 75 bps.

Perhaps some equity traders believe the worst-case scenarios are baked into prices, making it time for bargain hunting. If so, they are channeling their inner Baron Nathan Rothschild, who reportedly advised: “buy when there’s blood in the streets, even if it’s your own.”

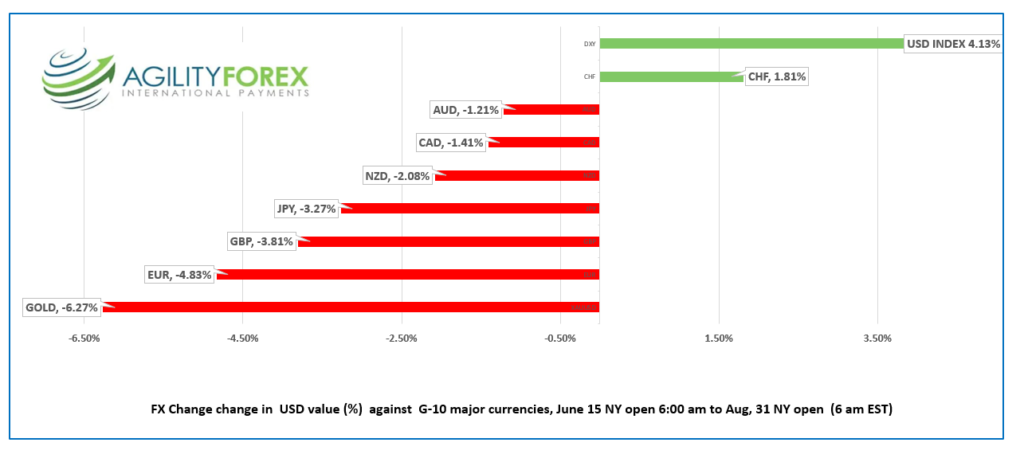

The FX market is singing a different tune. The US dollar has posted gains against the major G-10 currencies since the beginning of the year. The picture didn’t change much after the Fed’s June rate hike, except the Swiss franc posted a 1.81% gain, partly due to safe-haven demand for francs.

The US dollar will remain bid as long as the FX market believes the Fed will stick to its word and tame inflation by aggressively raising interest rates while outpacing rate hikes by other central banks. EURUSD and GBPUSD have broken significant support levels, and even though both currency pairs are oversold, they will continue to head lower.

USDCAD is showing signs of a topside breakout. While prices are above 1.3020, which is the 38.2% Fibonacci retracement level of the Covid range (1.2015-1.4650), a test of the 61.8% level of 1.3640 is in the cards. The long dollar trade is crowded, but there will be plenty of buyers on corrections., which should limit downside moves.

The central banks caused this car crash, and traders are still cleaning up the wreckage.

Chart: USDCAD since Covid

Source: Saxo Bank