By Michael O’Neill Agility FX, Senior Analyst

Did the Loonie dodge a bullet?

After Donald Trump was elected president, the US dollar soared. His proposed infrastructure spending and tax cut initiatives were expected to be inflationary and would mean that the Fed might be forced to raise interest rates higher than originally forecast. That was a bullish dollar scenario.

The Canadian dollar was a victim of that sentiment. USDCAD rallied hard in December, leading to forecasts for added gains toward 1.4000 sometime in 2017. The Bank of Canada (BoC) already had a doveish bias and the prospect of a widening of US/CAD interest rate differentials was viewed as a major negative for the Canadian dollar.

The view was reinforced by BoC Governor Stephen Poloz in January. He responded to a press conference question about interest rates with “Yes rate cuts remain on the table”.

USDCAD headed higher but the move stalled well below the December peak, leaving many traders perplexed.

Canadian and US interest rate paths were diverging, Canadian economic growth was lagging that of America, the oil price rally had stalled and there were rising fears that the North America Free Trade Agreement (NAFTA) was in jeopardy, so why wasn’t USDCAD a lot higher?

The answer was “Donald Trump.”

It was Donald Trump that sparked the US dollar rally and it was President Trump who ended it.

The president’s complaint that China, and Japan were playing the “devaluation market” spooked FX markets. It was followed by comments from Peter Navarro, the head of the new National Trade Council, accusing Germany of doing the same thing.

Suddenly, fears of trade wars replaced the US growth/higher rates story and the US dollar retreated.

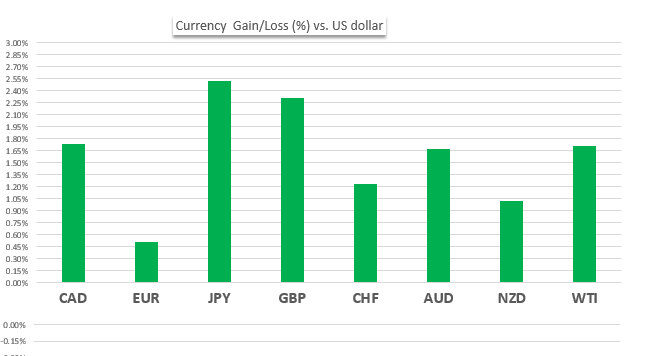

The US dollar has dropped across the board against the G10 currencies since President Trump’s inauguration.

Chart: Currency gains vs. US dollar from Jan.20-Feb.9/17

Source: Loonieviews.net

President Trump’s protectionist policies are seen as a US dollar negative and offsetting any positives from the fiscal stimulus program. Many believe his trade agenda will be lead to slower growth. If growth is slowing, Fed rate increases may be fewer and slower than expected.

Traders have not forgotten last year’s rate hike scenario. In February 2016, the market was convinced that it would see four Fed rate increases in 2016. They saw one. The CME Fedwatch tool now pegs the odds for a March rate increase at a mere 4.4% and a June increase at only 47.3%. Maybe the three rate hike scenario for 2017 is just a mirage.

Steady oil prices have contributed to the positive Canadian dollar sentiment. West Texas Intermediate, (WTI) the benchmark price for Canadian crude, has managed to stay above $50.00/barrel since January despite high US crude inventories. Oil traders remain optimistic that the mix of Opec production cuts and increasing global demand will provide additional upside for prices.

That’s not all. There are seasonal factors as well.

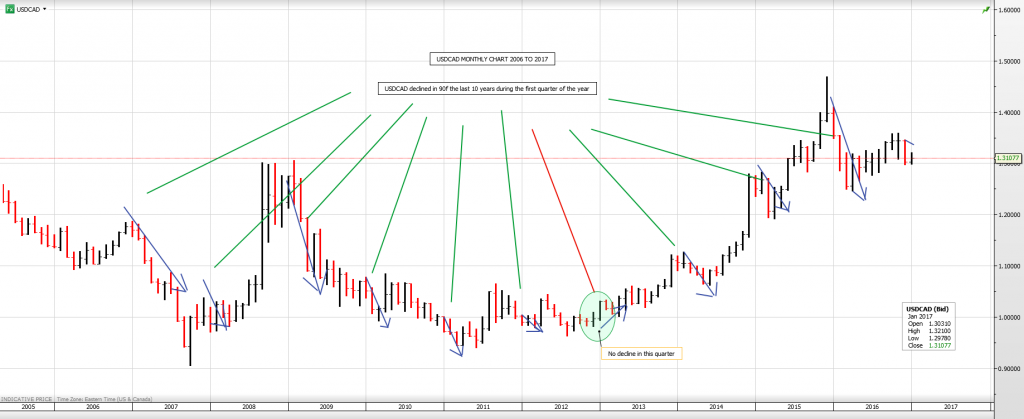

USDCAD has declined in the first quarter for nine out of the past ten years. The rationale for the move is hard to quantify although corporate year end could be one factor.

The Canadian dollar tends to get sold in the latter part of the year as foreign entities operating in Canada, close their books for the year. For many that also means repatriating profits back to their parent company in America which they do by selling Canadian dollars and buying US dollars.

At the start of the new year, USDCAD demand dries up because repatriation flows are finished. New capital expenditure budgets are, or have been, approved and companies start spending money. That could also mean American companies pump money back into their Canadian subsidiary. In addition, Canadian exports may increase after slowing down into the year-end holiday season. These factors may be anecdotal but the seasonal USDCAD weakness is very clear in the following chart.

Chart:USDCAD monthly 2016 to 2017

Source: Saxo Bank

Source: Saxo Bank

The short term USDCAD technical factors have turned bearish as well and warn of further losses. USDCAD could drop to 1.2730. (78.55 cents) in the weeks ahead.

USDCAD had been in a steady uptrend since the beginning of May 2016. It stayed intact and survived many attempts to break below it until January of this year when it shattered. The break coincided with the breach of the 38.2% Fibonacci retracement level (1.3165) of the 1.2460-1.3600 range that had prevailed for all of 2016, opening the door to further losses down to the 61.8% level. (1.2895).

For the time being, confusion surrounding President Trump’s trade strategy, a lack of details about the fiscal stimulus program and seasonal factors will keep the Loonie flying high.