Source: Peanuts Worldwide

By Michael O’Neill

Hike and hold or hold and hike. That was the Bank of Canada’s dilemma on January 25.

They hiked, said they would hold, and left traders to decide if it was a blockhead move.

The BoC said Canadian economic growth was stronger than expected and that the economy remains in excess demand. They noted that the unemployment rate is near historic lows and business are reporting ongoing difficulty in finding workers.

Those are not reasons to stop raising rates.

Governor Tiff Macklem and the Governing council think otherwise. They expect domestic growth to stall in the middle of the year and believe that improved global supply chains and lower oil prices will drive inflation down “significantly” this year, and if correct, pausing rate hikes makes sense.

Mr Macklem’s press conference could have been his finest hour.

All he needed was a fat Romero y Julieta in his mouth while proclaiming “Now is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.”

Alas, he didn’t.

Instead, he said “We expect to hold the policy rate at its current level while we assess the impact of the cumulative 425-basis-point increase in our policy rate. We have raised rates rapidly, and now it’s time to pause and assess whether monetary policy is sufficiently restrictive to bring inflation back to the 2% target.”

Now that is a bit of a nose stretcher.

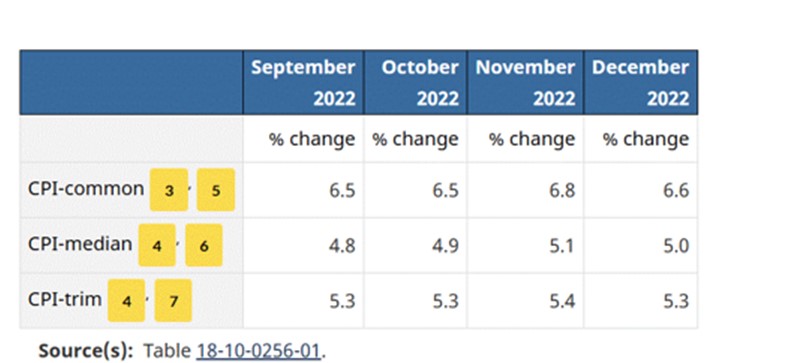

On December 8, BoC Deputy Governor stressed that rate decisions will be data dependent. The drop in inflation in December is merely a one-month trend and even by the BoC’s own measurement, inflation is still higher than in September and October.

That’s wishful thinking not inflation peaking.

Source: BoC

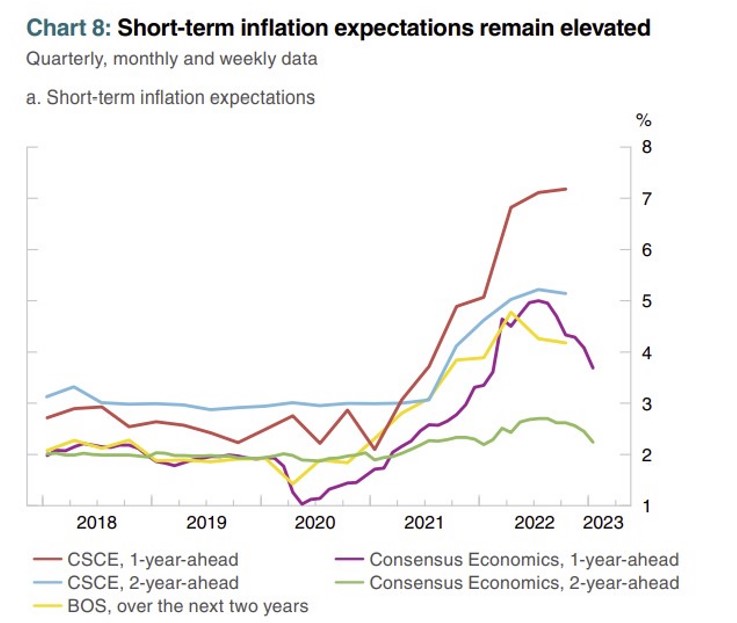

The BoC’s Consumer Expectations Survey suggests that Inflation is going to be a problem for far longer than policymakers anticipate.

The survey respondent’s 1-year ahead inflation forecast is 7.18% while the 2-year ahead guess is 5.14%. Based on those predictions, it is not a stretch to expect workers to demand large pay bumps.

Source: BoC MPR

It is already happening.

Canada Revenue Agency (CRA) workers are especially dismayed by economic hardships and are demanding a 30% pay increase over three years.

CBC quoted CRA Union President Marc Briere saying, “People are having a hard time out there to make ends meet and so that’s why we’re asking for a new contract with decent wage increases.”

He didn’t clarify whether those having a “hard time” referred to his own union members who earn an average of $66,687.00/year, enjoy a defined benefit pension, and have little risk of losing their jobs, or the low-income, non union private sector workers.

The Monetary Policy Report (MPR) noted that a major risk to the projections is that “global energy prices could increase, pushing inflation up globally.”

That’s a huge risk.

Opec expects world oil demand to increase by 2.22 million barrels/day, supported by rising Chinese demand as the economy reopens from covid-zero restrictions. Demand could rise even higher if the economic downturns in major developed economies are less severe than expected.

JP Morgan analysts downgraded their forecast for Brent (the European benchmark price) to $90.00/b from $100.00/b. That price reduction assumes that Russia successfully finds alternative buyers for its crude and India is a prime candidate.

However, it is unlikely that the west will repeal sanctions on Russian crude in the next year. The European Union just rolled over all EU sanctions for another six months. In addition, the EU, and US plan to review the price cap on Russian oil in March.

All of the above will underpin crude suggesting West Texas Intermediate is more likely to trade at $90.0-$100.00/barrel than $70.00/b.

The biggest risk to the Bank of Canada’s view is the Federal Open Market Committee.

The FOMC meets February 1, and they are expected to raise rates by 25 bps and that won’t be the last hike. US rates will continue to climb to at least 5.0% then stay there.

Many analysts are anticipating that not only will the Fed pause hiking rates as soon as March, but they also expect the first rate cut by December.

Fed officials do not see it that way.

Vice Chair Lael Brainard said policy moved into restrictive territory at a rapid pace, but rates still needed to move closer to a sufficiently restrictive level to restore price stability.

Fed Governor Waller warned against premature rate cuts to guard against inflation resuming and said it would take at least “through the summer” to gain confidence with that outlook.

If US rates continue to rise while the Canadian rate environment stagnates, the ensuing surge in USDCAD could result in higher domestic inflation as Canadians pay more for US goods. The Bank of Canada would have to raise interest rates and Tiff Macklem would become more Charlie Brown than Winston Churchill.