Source: YouTube

By Michael O’Neill

There’s a whole lotta honking going on. A trucker protest that began because of the government’s “spin the wheel” approach to vaccination rules and requirements morphed into a massive anti-government demonstration by hordes of disgruntled Canadians.

A cacophony of horns are blaring across financial markets as well. Not from motor vehicles or musicians but by scores of traders and analysts who believe central banks have lost the plot in managing inflation.

Those horns got louder on February 10.

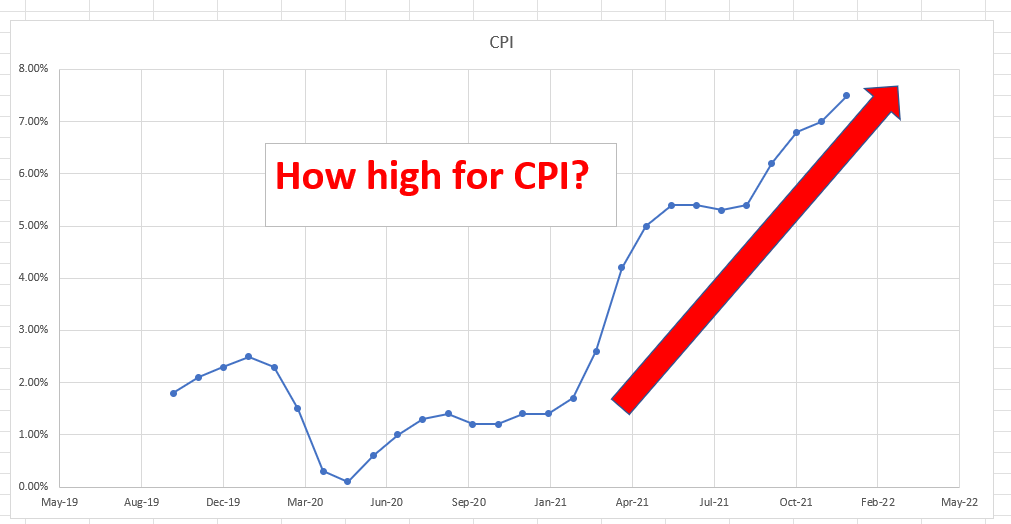

The Bureau of Labor Statistics reported, “the all items index rose 7.5 percent for the 12 months ending January, the largest 12-month increase since the period ending February 1982.”

At his post FOMC press conference on January 26, Fed Chair Powell explained that inflation was higher than the longer-run goal of 2.0% due to supply imbalances from the pandemic and has spread into other economic areas, including wages. He added, “Like most forecasters, we continue to expect inflation to decline over the course of the year. He would probably say the same thing after the latest inflation report.

Should you be worried? Most certainly.

The Fed and other central banks struggled to explain why inflation was stubbornly below their targeted levels prior to the pandemic.

In October 2019, Mr Powell seemed perplexed as to why inflation was below the 2 percent objective, and he worried that indicators of longer-term inflation expectations were at the lower end of their historic ranges. Despite those concerns, he was confident that inflation would rise to 2.0%.

His confidence was well placed, although Fed actions had nothing to do with CPI reaching the Fed target in March 2021.

Chart: BLS/IFXA Ltd

Today, Mr Powell’s problem is trying to convince Americans and global investors that inflation, which is at a 40 year high, will decline over the course of the year. It may not be that simple.

Winston Churchill told the British House of Commons in 1948, “those that fail to learn from history are doomed to repeat it.”

Mr Powell missed the speech because he wasn’t a British MP, and he wasn’t even born, but he should still heed the words.

There are a lot of similarities to the Great Inflation Era of the mid 1970’s-early 1980s.

The 1974 Arab oil embargo shocked the global economy, quadrupling the cost of oil, and then the 1979 Iran Revolution saw prices double.

At the same time, the Federal Reserve pumped liquidity into the market. Michael Bryan, Federal Reserve Bank of Atlanta’s paper on the Great inflation claims the Fed exacerbated the inflation problem. He said the Fed was motivated by a mandate to create full employment with little or no anchor for the management of reserves. The Federal Reserve accommodated large and rising fiscal imbalances and leaned against the headwinds produced by energy costs. These policies accelerated the expansion of the money supply and raised overall prices without reducing unemployment.”

These events led to soaring inflation and a sky-high Fed Funds rate that peaked at 22.36% in July 1981. Unemployment soared, and stocks tanked.

It’s 2022, and Groundhog Day is not just a movie.

Oil prices have more than doubled in only twelve months. The Biden Administrations’ budget deficit is around $3.0 trillion, and the Federal Reserve’s balance sheet has ballooned to $8.0 trillion from $4.0 trillion in 24 months.

War drums are pounding in Eastern Europe. Russia, the world’s second or third-largest oil producer, and the US and NATO are trading threats and amassing troops over Russia’s threat to invade Ukraine. China continues to intimidate Taiwan, and North Korea’s Kim Jung Un is flinging ballistic missiles into the Sea of Japan.

Nevertheless, the December FOMC dot-plot forecast shows the overwhelming majority of policymakers expect Fed funds to top out at 2.5% in 2023 and beyond.

The inflation issue not just a US problem. Canada’s inflation is 4.8%, with the three main Bank of Canada measures all above target. Governor Macklem blamed the current level of inflation on supply chain disruptions, oil prices, and poor harvests boosting food prices. He didn’t mention anything about the impact of massive Bank and Government stimulus. He also said, “we want to clearly signal that we expect interest rates will need to increase.”

On Feb 2, he proclaimed to the Senate Banking Committee, “Canadians can be assured that we will use 1 1our monetary policy tools to control inflation.”

If you believe Mr Macklem and his desire to control inflation, then you must believe Canadian interest rates are going sharply higher.

Former Bank of Canada Governor Gerald Bouey (1973-1987) needed to hike the overnight rate to 16% in February 1981, so why expect Canadian inflation to be tamed with just a 1 or 2% rate increase? If so, Canadian’s may expect honking big rate hikes in the coming months.