“Look, up in the sky. It’s a bird. It’s a plane, It’s Superman. Nope, it’s just a bird, an interest rate hawk, as a matter of fact. The kind of bird that has rarely been seen around the global central banks for the past few years.

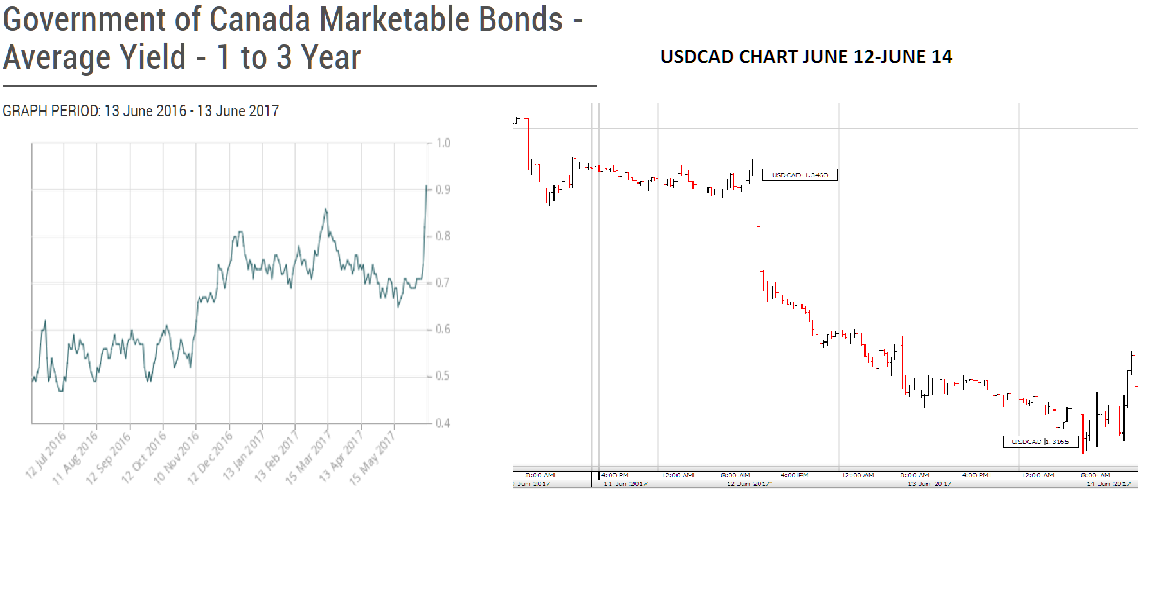

The Canadian interest rate hawk was first spotted in Winnipeg on June 12. Bank of Canada Senior Deputy Governor Carolyn Wilkins delivered a speech titled “Strength in Diversity”. The title was a nice segue into an upbeat assessment of Canadian economic growth.

She noted that Canada had moved past the adjustment to lower oil prices as shown by Q1 GDP growth of 3.7 percent, which she described as impressive. Growth was spread across more than 70 percent of industries.

Employment growth was another positive economic sign with job gains in services offsetting those lost in “goods employment”.

The she dropped the “rate hike “bomb although she avoided using the term “rate hike”.

She said “To ensure that inflation gets back to target on a sustainable basis, we must consider not only current economic conditions but also how they will evolve. If you saw a stop light ahead, you would begin letting up on the gas to slow down smoothly. You do not want to have to slam on the brakes at the last second. Monetary policy must also anticipate the road ahead.”

Financial markets heard “rate hike.” Canadian government bond yields soared as did the Canadian dollar.

Ms. Wilkens speech was an abrupt “about face” from the previous Bank of Canada stance. Her speech, while acknowledging economic risks, focused on the positives. Instead of highlighting economic risks that could necessitate more accommodative monetary policy, she targeted upside growth risks. She said “We also underscored the risk that even stronger growth in the United States could lead to a big jump in business confidence, igniting “animal spirits” as John Maynard Keynes would have put it.”

Ms. Wilkens speech was an abrupt “about face” from the previous Bank of Canada stance. Her speech, while acknowledging economic risks, focused on the positives. Instead of highlighting economic risks that could necessitate more accommodative monetary policy, she targeted upside growth risks. She said “We also underscored the risk that even stronger growth in the United States could lead to a big jump in business confidence, igniting “animal spirits” as John Maynard Keynes would have put it.”

And the stronger growth in the United States prophecy may be coming true.

On June 14, the US Federal Open Market Committee (FOMC) raised the target range for federal funds to 1.0-1.25 percent, the second time rates were increased in 2017. Not only that, the door is still wide open for a third increase, possibly in September.

The FOMC attributed the need to increase rates to moderately rising economic activity, solid job gains, and increased household and business spending.

The only concern was the recent dip in inflation. Janet Yellen dismissed it by saying policy makers wouldn’t overreact to “noisy” data.

The FOMC also announced that the Fed would gradually reduce their securities holdings in 2017, but stressed it would not be disruptive to interest rates.

The FOMC’s actions were expected although the balance sheet reduction news and the unchanged interest rate forecast suggests that this meeting was not as doveish as many market participants expected.

Hawks are circling the European Central Bank (ECB) and the Bank of England (BoE) as well. President Mario Drahi has stubbornly maintained that the ECB’s policy is unchanged despite, Germany’s Bundesbank President Jens Weidmann, wanting to discuss the timing for an exit to quantitative easing. In what may have been a nod to the hawks on the board, the ECB changed its forward guidance by dropping the reference to lower rates in its June 8 statement. The thought that the ECB’s quantitative easing program will be ending has underpinned EURUSD.

Across the channel, at the Bank of England, the feathers were flying at the June 15 policy meeting.

The Bank of England voted to leave rates unchanged, but only five of the eight voting members wanted the unchanged policy. Three others wanted to raise rates by 0.25 percent.

The BoE is wrestling with rising inflation and weakening growth in the uncertain environment around Brexit. The UK election results added another layer of uncertainty.

However, the European Central Bank, the Bank of England and the Bank of Canada are merely contemplating interest rate increases at some point in the future. The FOMC has acted.

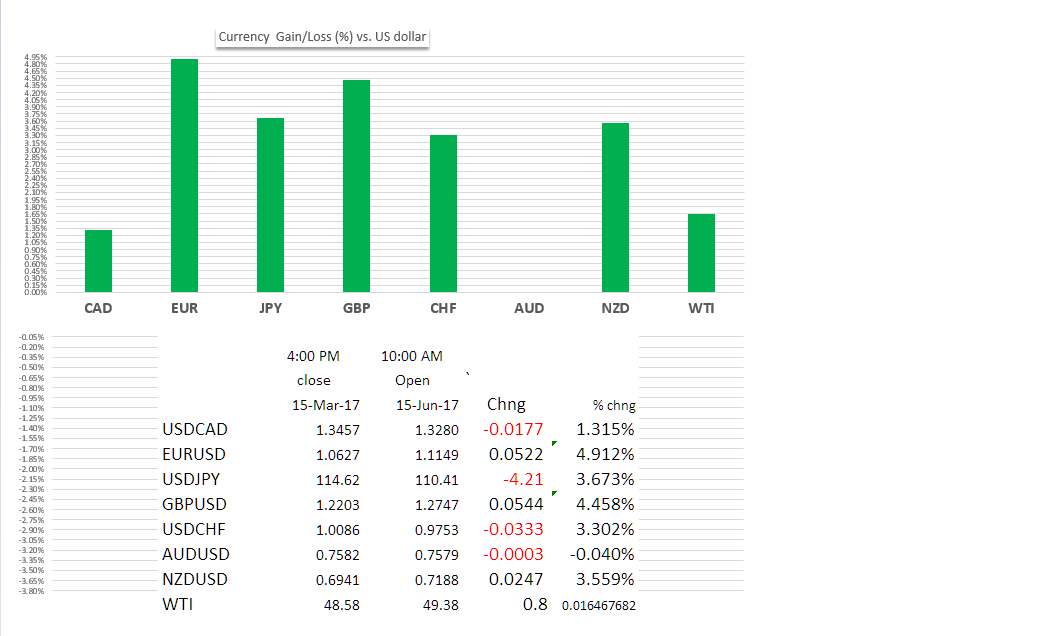

Yet, despite two rate hikes since March 15 and the promise of a third, the US dollar has dropped substantially against the G7 currencies. The exception of the Australian dollar, which is unchanged.

The question is “if interest rate hikes are supposed to attract investment capital resulting in increased demand for a nation’s currency, why has the US dollar declined?

The answer may be in the type of hawk advocating rate increases. Fed Chair Yellen, who is hiking rates, coos like a dove at every press conference. Noted Bank of England hawk, Kirsten Forbes has been declawed as the June 15 meeting was her last as a board member. Jens Widemann, the ECB hawk has been crying rate hike for so long, his calls have lost their impact. The BoC is known to flip-flop on policy statements so as hawks go, Carolyn Wilkins may just be a fledgling.

A dove in hawks clothing (feathers?) is still a dove.