By Michael O’Neill

The Canadian dollar is trading at levels last seen in April 2018. It is just below 80 cents in US dollar terms, and it appears poised to continue the rally. Is this fair value? Is the move sustainable? Only time will tell.

Just as a rising tide lifts all boats, in 2020, a sinking US dollar lifts all currencies. The greenback is the FX engine, and it is full throttle in reverse. USDCAD sank twenty big figures (0.2020 points) in ten months, for a 13.3% gain. It was not alone as evidenced by the US Dollar index.

The USDX is a measure of the value of a weighted basket of currencies representing the bulk of America’s trade. It plunged from 103.80 in March to 90.04 on January 14, meaning the Canadian dollar was not the only rising currency.

USDCAD ended 2020 on a weak note and other than a bit of a wobble around the Georgia Senate runoff vote, the trend is continuing in 2021.

The prevailing wisdom in FX land heading into year end was for a vaccine-fueled turbo-charged, global economic recovery creating demand for the so-called “risk currencies,” in a low-rate interest rate environment.

Traders do not care too much about the here and now, preferring to gaze into their crystal balls to predict future currency levels. They assume other central banks will follow the Fed and that ample global liquidity will lead to capital flows away from the US$ as other markets (Europe & EM) become less risky and hence a safer place to invest. That sentiment is undermining the greenback.

“Hmm, I see US dollars…” Photo: creative commons

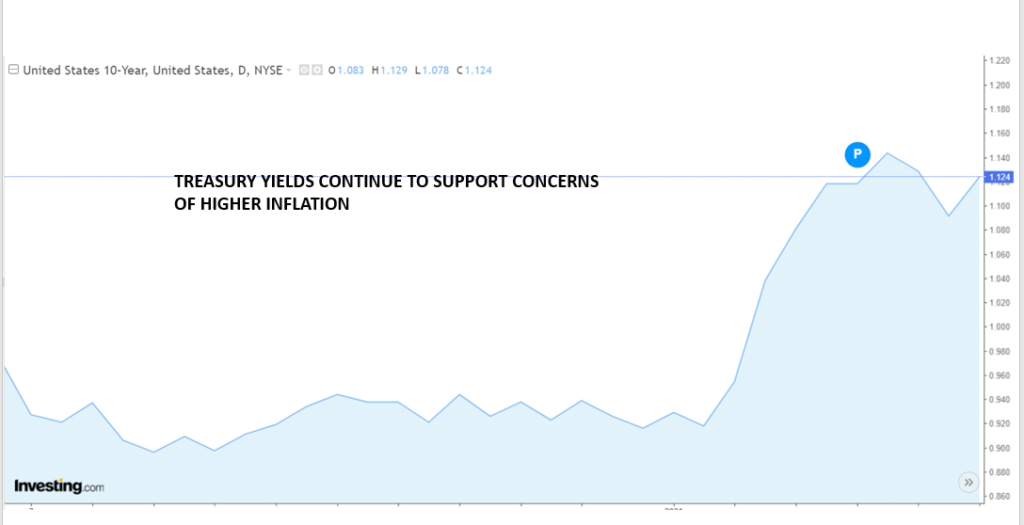

However, the balls may be crystal, but the view is far from clear. Earlier this week, a sharp spike in US 10-year Treasury yields gave the US dollar a bit of a bid. Call it the “Biden Bounce.” The President-elect promised to spend “trillions and trillions of dollars” on a new economic stimulus plan. Bond traders were not impressed. The concern is inflation implications from the stimulus program would force the Fed to taper quantitative easing programs earlier than expected. US Treasury yields soared with the 10-year yield reaching 1.177% from 0.918% at the beginning of the year.

Initially, the rationale for implementing the QE (coupled with fiscal support) was to maintain market stability and to quell emerging deflationary forces. The former has been achieved. The vaccine rollout has started (albeit sporadically), employment and subsequent price increases will follow. It follows that tapering will start sooner than has been previously signalled (2023?). Inflation is on everyone’s radar, except the central banks. At least that is what the US bond market is signalling.

US Treasury yields drifted lower on pushback from Fed officials. Boston Fed President Eric Rosengren said he did not expect inflation to be sustained over 2% this year. Vice-Chair Richard Clarida and Fed board member Lael Brainard echoed that sentiment.

And just in case financial markets did not get the message, Fed Chair Jerome Powell said Thursday; “the time to raise rates is no time soon.” Then he reminded traders that the Fed was well armed with tools to combat rising inflation. Despite the comments, 10-year Treasury yields were sitting at 1.13% near the close of trading, Thursday.

Treasury yields remain firm

Source: Investing.com

So, if you ignore the central bank inflation view, the weak US dollar scenario goes out of the window as well. The US may lead an economic boom (size does matter) and if so, interest rate differentials that favour the US will attract the lions share of capital flows. By default, the US dollar becomes king again.

The above scenario does not bode well for USDCAD bears.

The Loonie has rallied on the back of widespread US dollar selling pressures while domestic issues are ignored. Traders have swallowed predictions of robust economic growth in 2021, hook, line, and sinker. Economists expect that the vaccine roll-out will unleash pent-up consumer demand and drive growth up 5.5% in 2021. They may be too optimistic.

Ontario is the largest economy in Canada, and it has been hit extremely hard by the second wave coronavirus outbreak. Many restaurants and small retail outlets have been closed off and on since April. Many are on the verge of bankruptcy. It is not improving any time soon. Quebec and Alberta have also been hit hard.

Where is the pent-up consumer demand that supports the 5.5% Canadian economic growth going to come from? Canada is behind other major economies vaccinating their citizens. The UK has administered 4.19 doses per 100 people, the US is at 2.82, while Demark, Italy, Iceland, and Spain are ahead of Canada. The recent Bank of Canada policy statement noted “record high cases of COVID-19 in many parts of Canada are forcing re-imposition of restrictions. This can be expected to weigh on growth in the first quarter of 2021 and contribute to a choppy trajectory until a vaccine is widely available.”

The Canadian dollar appears well on its way to the 80-cent level (USDCAD 1.2500). However, Canada’s current account and massive budget deficits, combined with the slow pace of vaccinations and the latest lockdown measures suggests that it may truly be Looney to buy Loonies.