By Michael O’Neill

Is it over now? That’s the question Canadian borrowers are asking Bank of Canada Governor Tiff Macklem because the central bank left interest rates unchanged at 5.0%. It was the third consecutive month of “no change.”

There has been some “Bad Blood” recently, a lot of it actually. But that’s what happens when the central bank chief exhorts Canadian’s to strap on debt by saying “you can be confident rates will be low for a long time” and then blindsides them with rate hikes starting 20 months later.

That kind of bad advise is hard for borrowers to “Shake it Off.”

Mr Macklem’s interest rate forecast was so far out to lunch, it was like a Space-X moon shot hitting Pluto. But it is not his fault. Financial forecasts are notorious for being wrong but even so, they are always in demand by buy-side clients. That’s because they can shift the blame for their losing trades to sell-side economists. Noted US economist, John Kenneth Galbraith once said, “The only function of economic forecasting is to make astrology look respectable.”

The BoC may have paused raising rates, but they are loathe to say its over. The December 6 monetary policy statement had a slightly hawkish bias and so did Deputy Governor Toni Gravelle’s remarks the next day.

Mr Gravelle cited elevated wage growth which he said, “while above 4.0%, is higher than the level consistent with 2.0% inflation.” He also noted that although the Bank’s preferred measures of core inflation dipped slightly in October, it is just one month, and officials need to see more progress. Then he warned that “Given the risks to the inflation outlook, we remain prepared to increase the policy rate further if needed.”

Perhaps policymakers are feeling a tad bit remorseful after seeing the damage from Mr Macklem’s misguided interest rate forecast 3 ½ years ago.

Even so, Bank of Canada policymakers are merely puppets occasionally hogging centre stage because it is Fed Chair Jerome Powell and his colleagues on the FOMC who are pulling the strings.

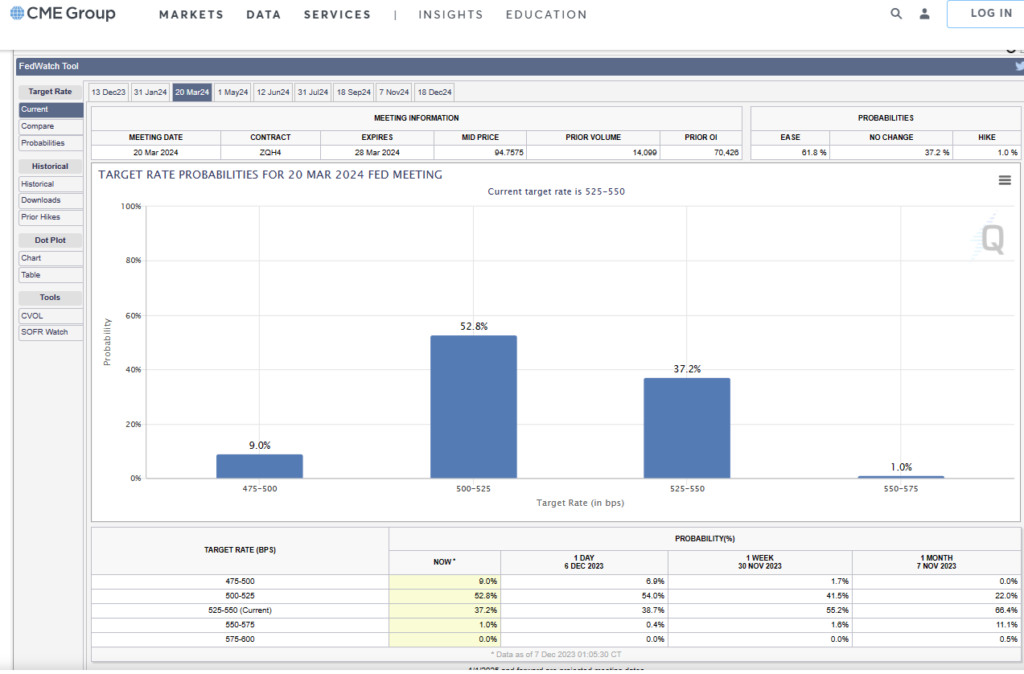

The outlook for US interest rates is as clear as mud. Market participants are convinced the Fed made its last rate hike on July 25 when Fed Funds rose to 5.50%. The Fed left them unchanged for the next two meetings and are universally expected to do the same on December 13.

Last September the FOMC minutes revealed that policymakers thought that the risks to achieving the 2.0% inflation target had become more balanced. They were concerned about downside risks to economic activity and the laggard macroeconomic effects from the tightening of financial conditions. They even worried about balancing the tightening/not tightening risks so said that future rate decisions would be “data dependent.” Mr Powell echoed that sentiment last week.

Financial markets have taken a “data dependent” Fed at face value. Weaker than expected employment data, robust Q3 GDP growth numbers, and sharply lower inflation readings sent bonds screaming higher. The US 10-year Treasury yield has collapsed 83 bps since November 1 to just 4.10% today, creating a firestorm of interest rate cutting predictions. CME interest rate traders have put their money where their mouth is and are pricing in a 62.8% chance of a rate cut on March 20, which is up from 41% a week ago and just 22% in November.

Source: CME Group

Fed rate cut fever has infected the G-10, except for Japan. EURUSD traders expect the European Central Bank to drop its 4.0% overnight rate to 2.5% by the end of 2024, while sterling traders believe the Bank of England will lower rates by 75 bps. The RBA and RBNZ are also expected to join the rate cut party.

The central bankers are not amused. They see themselves as the elite echelons of global economic policymaking and find it very repugnant that a cabal of greedy, money grubbers are usurping their authority. To that end, it is highly likely that Chair Powell will maintain a hawkish bias during his press conference on December 13. The forward guidance other G-7 bankers will express a will have a similar tilt.

The Canadian dollar is merely a spectator in the unfolding drama and as a matter of fact that has been the story all year. The value of the Canadian dollar has risen a mere 0.12% since the 2022 close and the opening level on December 7.

There isn’t a whole lot to like about the Loonie. The Canadian economy is shrinking and flirting with negative growth while the US, its largest trading partner grew 5.2% in Q3.

Canada’s anti-fossil fuel policies have scared away foreign investors. In 2022 the US saw investment inflows of $388 billion, Australia attracted $67 billion, and Canada, a mere $54.0 billion. National Post’s Diane Francis quotes the IMF who claim Canada’s investment climate has deteriorated relative to comparative jurisdictions.

The Canadian dollar is also suffering from the steep drop in oil prices since November 30 and bearish interest rate spreads between 10 year Canada and US government bonds. The USDCAD long term uptrend from June 2021 is intact above 1.3140 on a monthly chart.

It has been a good year for Taylor Swift but for answers about Canadian interest rates in 2024, it is still a “Blank Space.”