Photo: Dreamline.com

By Michael O’Neill

“Who let the dogs out? Who? Who?” The Baha Men asked that question twenty years ago, and FX traders are asking that same question today. We are deep into the Dog Days of Summer, which end August 23.

The Farmers Almanac describes the days as hot and humid.” They got that right this year, at least in the eastern parts of Canada and the US as well as the UK and Europe. On Canada’s west coast, not so much.

Traders are well-aware of the phenomenon. Liquidity tends to evaporate as August is prime holiday month for many market participants, although thanks to COVID-19, the holidays are likely spent close to home.

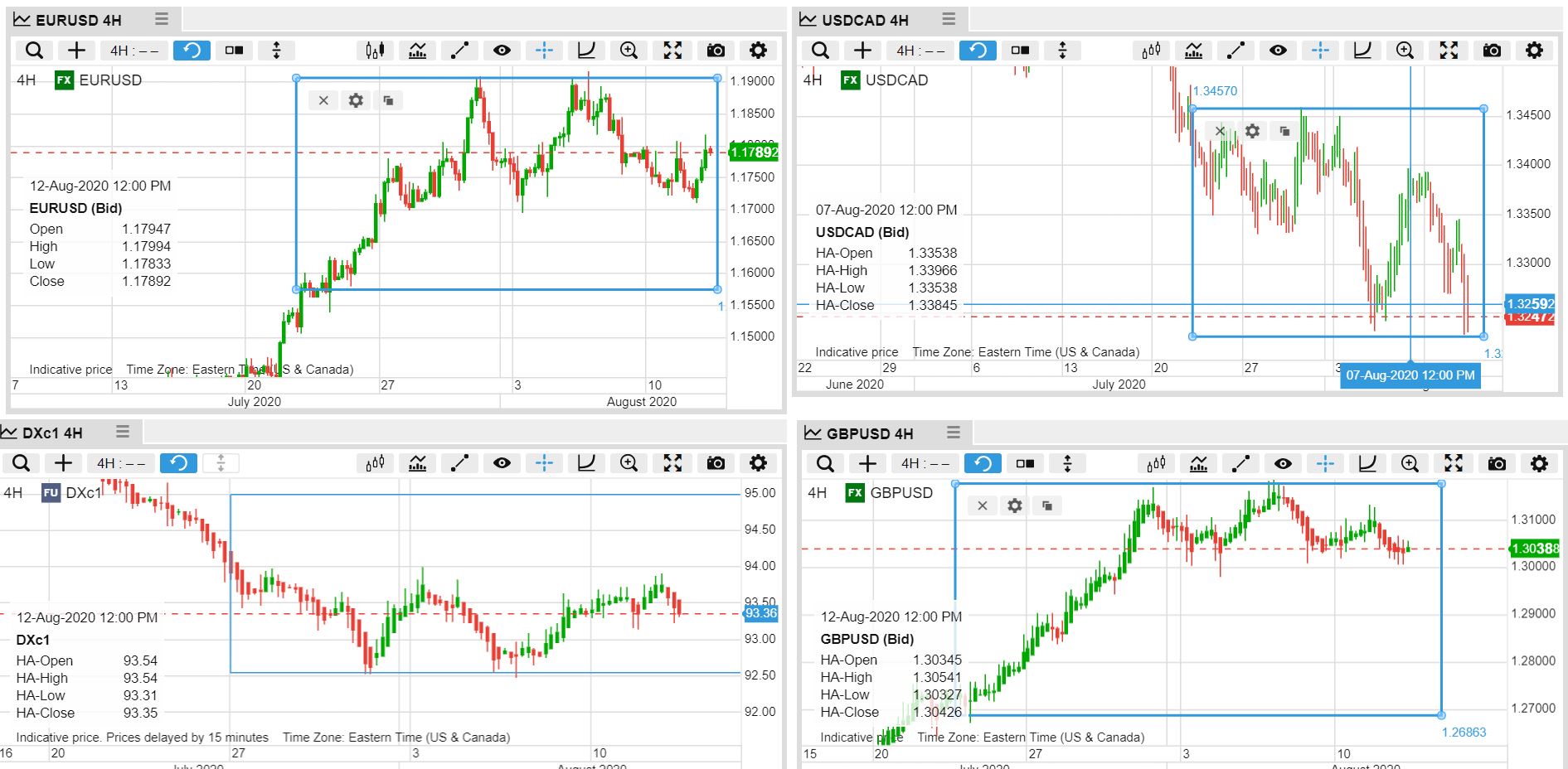

The following chart clearly shows range-bound currency pairs during the Dog Days.

Source: Saxo Bank

Currencies may trade in tight bands implying a general lack of direction, but that doesn’t mean there are not significant issues lurking in the wings. They may come to the fore when September rolls around and continue into year-end.

Those issues include China, COVID-19 concerns, the US election, central bank actions, massive government deficits, and renewed trade hostilities.

There are numerous flash-points, and all of them have China as the epicentre. China is embroiled in political spats with Australia, New Zealand, Canada, United Kingdom, European Union, and the US.

China: China-Australia political relations deteriorated when Prime Minister Scott Morrison proposed an independent review of the coronavirus pandemic.

Beijing’s heavy-handed tactics in Hong Kong led Australia to offer safe-haven to Hong Kong students living in Australia, along with the suspension of its extradition treaty. China saw the reaction as a “grave provocation.” China used its trade muscle to send a message to Australian politicians when tariffs on Australia barley were imposed.

New Zealand annoyed Beijing when it followed Australia’s lead and suspended its extradition treaty with China, then changed its military, and technology export policy. Beijing accused NZ of “gross interference” in its affairs.

The United Kingdom /China relations are deteriorating.

The UK complained about China’s actions in Hong Kong, the detention of Uighurs in the northwest region, and banned Huawei from participating in the UK’s 5G network. China is not amused. They are the UK’s sixth-largest export market, and in the absence of an EU trade deal, gives China added clout.

China and the US are at odds on just about everything. American’s have assailed China on all fronts, from contesting China’s South China Sea aspirations to sanctioning senior Chinese politicians, and what looks like a stealth-nationalization of WeChat and Tik Tok. President Trump blames China for the COVID-19 pandemic, calling it the China virus, further antagonizing Beijing.

China tensions could escalate further and spark a wave of risk-aversion trading.

COVID-19 For many nations, the worst of the coronavirus pandemic may be over. Strict quarantine measures, mandatory social distancing and wearing of face-masks in public has the virus reeling. America is not one of them. The US is still recording 50,000 new cases each day, but hopes for a soon to be released vaccine, have traders acting like the pandemic has been eradicated.

It’s not. Many infectious disease specialists are uttering House Stark’s motto-“Winter is Coming.” Cold temperatures bring people indoors which will put social distancing to the test. Winter is also flu season. Sure, a vaccine is coming. Russia approved one this week, and President Trump ordered 100 million vaccines from Moderna, but no one knows if they work.

“its getting chilly” Source: HBO

A Covid-19 pandemic, round 2, would tax politicians’ ability to manage it, especially since budget deficits have ballooned and interest rates are close to zero or negative. The US dollar soared at the height of the pandemic, which suggests a new pandemic would lead to a similar move

Election: The US election is another cause for concern. President Trump is 9 points behind Joe Biden as per an August 10-12 YouGov poll. Traditionally stocks rise when a Republican wins and sink with a Democrat winner. If the relationship holds in 2020, sky-high US equity indexes may plunge to earth, dragging global indexes down with them. Hilary Clinton would tell you not to believe the polls.

Trade: The Canadian dollar is vulnerable to all the aforementioned concerns plus a slew of homegrown problems. For starters, President Trump kicked-off another trade skirmish. While campaigning in Ohio, he decided that import of Canadian aluminum was a national security concern and slapped them with a 10% tariff. The news was a shock to the US Aluminum Association which said :“We’re incredibly disappointed the administration failed to listen to the vast majority of domestic aluminum companies and users.” They also pointed out that aluminum imports from Canada declined in June. Canada retaliated, placing tariffs on a series of US products.

China is expressing annoyance with Canada in a variety of ways. Canadians in China are vulnerable to arbitrary arrest and detention as the “Two Michaels,” Kovrig and Spavor discovered when Beijing retaliated for Huawei CFO Meng Wanzhou’s arrest on a US extradition warrant.

The Office of the Chief Economist (Global Affairs Canada) 2020 State of Trade report had this to say about China trade: “Canadian goods exports to China experienced a sharp 16% drop. Underlying this drop were the trade measures China imposed on Canadian food products.”

Beijing has weaponized its trade clout to extort political gain.

The dogs may be barking now, but investors could be howling later.