“The US election is finally here” Photo: IFXA Ltd

By Michael O’Neill

The US election is finally here. If it seems like the candidates have been campaigning for an eternity, they have. President Trump kicked things off on January 20, 2017, when he formally filed his re-election campaign with the Federal Election Commission. That was also the day he was sworn in for his first term.

Democrat Candidate Joe Biden started his presidential bid, a tad later. He only secured his party’s nomination on August 18, 2020. Others argue that he has been campaigning for 47 years; ever since 1973 when he was first elected to the Senate.

Who will win? A large number of polls suggest it is Joe Biden’s election to lose. In 1891 American author Mark Twain said “Lies, damned lies, and statistics” to complain about how numbers are used to bolster weak arguments. That phrase is more accurate today than ever, especially when it comes to US elections. Just ask Hillary.

Who cares? American’s for sure. Also, the rest of the world, from the G-20 to Emerging markets, and even despots, and tyrants. That’s because, for all its faults, the USA is the most influential nation on earth. It is the world’s economic engine, the world’s reserve currency, and the worlds most powerful nation.

A major knock against Joe Biden is that he plans to raise taxes. The spectre of higher taxes raises fears of exacerbating the economic slowdown while the country is still reeling from the coronavirus. Those naysayers predict stocks will plunge. Their evidence is the performance of the Dow Jones Industrial Average (DJIA) since October 12, with Biden riding high in the polls. They conveniently ignore the impact of a surge in COVID-19 cases in America and around the globe for the sell-off. The reality is that global interest rates are at record low levels and fueling positive risk sentiment. As long as rates remain at or near zero, equities look attractive, regardless of who is President.

And interest rates are not rising any time soon. Certainly not in Canada. Bank of Canada (BoC) Governor Tiff Macklem said during the Monetary Policy Report press conference on October 28: “You can be confident that interest rates will be low for a long time.”

The BoC left interest rates unchanged, recalibrated the Quantitative Easing program, promised extraordinary forward guidance, and said policy rates would be unchanged until 2023. The recalibration of the QE program means that instead of buying $5.0 billion short- maturity bonds each week, they will only buy $4.0 billion, but by the bonds will have a longer duration. The BoC said the action was stimulus-neutral.

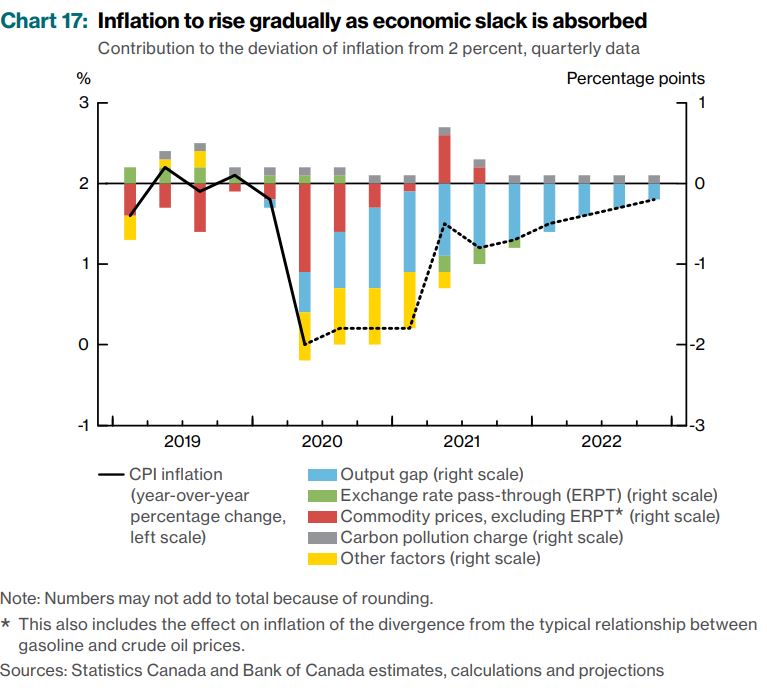

The BoC expects the “dramatic decline in gasoline prices in March and April” to hold inflation down until 2021. After that, the sizeable output gap will ensure inflation remains below the 1-3% targeted range into 2023. The Q3 output gap is estimated to be -3 to -4, and with over 720,000 Canadians still unemployed in September, closing the output gap by 2023 may be optimistic.

Source: BoC Monetary Policy Report

The Bank of Canada downgraded its 2021 Real GDP forecast to 3.8% from 4.9%, and its 2022 forecast to 3.0% from 3.2%

Some pundits may suggest that the USDCAD rally from 1.3186 at the October 27 New York close to 1.3322 by early afternoon on October 28 was because of the dovish Bank of Canada monetary policy outlook. That would not be true. USDCAD gains were driven by broad safe-haven demand for US dollars because of new coronavirus outbreaks in Europe, and America, and from caution ahead of the election.

However, the MPR states “By convention, the Bank does not forecast the exchange rate in the Monetary Policy Report. The Canadian dollar is assumed to remain at 76 cents US over the projection horizon, close to its recent average and somewhat above the 74 cents US assumed in the July Report”.

So that explains no forecast of inflationary impact of a potentially much weaker Can$

Germany, France, Italy, and Spain introduced, or will be introducing, new lockdown measures in the coming days. Recent Eurozone economic data has been weak, derailing a tepid economic recovery. New lockdown measures will exacerbate the slowdown and may force the European Central Bank, (ECB) to announce new stimulus measures at the October 29 meeting.

Global interest rates are going to stay low for a prolonged period. Markets are expecting some type of COVID-19 vaccine in the coming months, and as long as they have that hope, low interest rates will spur positive risk sentiment. The US election is just a distraction and traders are “Biden their time” until a result is known.