By Michael O’Neill

“Get your rates a-droppin’. Head out to the bank. Tiff is looking for some adventure with whatever’s in the tank.” Bank of Canada Governor Tiff Macklem may not have been “Born to be Wild,” but if he cuts interest rates on June 5, he will be the “Leader of the Pack.”

The First Cut is the Deepest

Mr. Macklem predicted such a move during his post-meeting press conference when he responded to a question about a June rate cut with, “Yes, it’s within the realm of possibilities.” He said that “the data since January have increased our confidence that inflation will continue to come down gradually even as economic activity strengthens. Our key indicators of inflation have all moved in the right direction.”

Inflation in Check

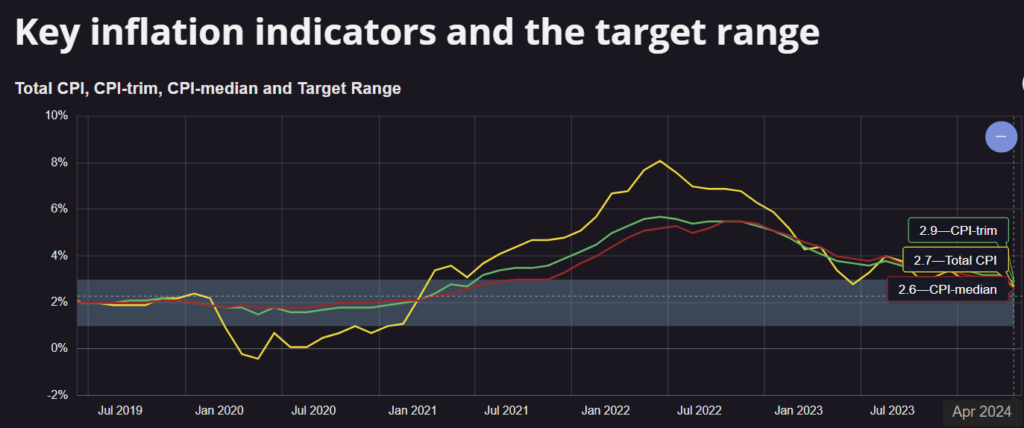

The inflation data continued to move in the right direction, as evidenced by the April consumer price index, which rose 2.7% y/y compared to 2.9% in March. More importantly, the BoC’s own inflation metrics, CPI-trim and CPI, dropped and are now inside the bank’s targeted range of 1-3%.

Source: Bank of Canada.

Analysts Predict Rate Cut

The results led to a bevy of analysts and major bank economists forecasting a 25 bp rate cut in June. If so, that would make the BoC the first G-7 central bank to cut interest rates in the post-pandemic era. (The Swiss National Bank cut rates by 25 bps in March, but they are not a G-7 country). The analysts are probably right, especially if Mr. Macklem talks to Peter Routledge, the Superintendent of Financial Institutions (OSFI). Mr. Routledge released OSFI’s Annual Risk Outlook for the fiscal year 2023-2024 on May 22. The section on mortgages is not pretty.

Mortgage Concerns

As of February 2024, a significant 76% of outstanding mortgages are due for renewal by the end of 2026. Homeowners who secured their mortgages when interest rates were lower between 2020 and 2022 will face a nasty shock, even more so for those households that are heavily leveraged. It’s even worse for those 15% with variable rate mortgages but fixed payments, as many are negatively amortizing, which means the scheduled mortgage payments no longer cover the full interest costs or the principal.

The mortgage issue should serve as a strong motivation for the Bank of Canada to cut interest rates. Lower interest rates would alleviate the payment shock for homeowners renewing their mortgages, especially those with variable rate mortgages and fixed payments. It would also ease the financial strain on households and reduce the risk of defaults and arrears.

Economic Stimulus

OSFI notes that lower interest rates could stimulate economic activity, potentially strengthening labor markets and reducing the risk of higher unemployment rates. This would further alleviate the debt strain on households and the risk of losses for financial institutions.

Challenges Ahead

A rate cut is not as straightforward as central bank comments and data might suggest. For starters, the BoC announced it was overhauling its projection and policy analysis models after their colossal failure during and immediately after the pandemic. Arguably, the new batch of models may need more time to prove themselves.

Central bankers like to talk to each other, and often monetary policy statements are very similar. On May 22, the Reserve Bank of New Zealand left interest rates unchanged at 5.50% because, although inflation was declining, at 4.0%, it was still far above its 1-3% target. The RBNZ noted that increased immigration is driving up rent inflation, currently 4.7%, which is well above the 20-year average of 2.6%. The RBNZ left rates unchanged because inflation was too high.

Contrasting Situations

It’s a bit different in Canada. Inflation is inside the 1-3% target range, and the BoC’s sole mandate is to maintain price stability. Based on that, there should be no question about a June rate cut.

However, the RBNZ’s major trading partners are China and Australia. Both of those economies are pretty soft. Canada’s biggest trading partner is the United States, and its economy is fairly robust growing 1.6% y/y in the first quarter. The US inflation decline is painstakingly slow, which forced many Federal Open Market Committee officials to suggest US interest rates will need to remain in restrictive territory for longer than previously expected.

Risks of a Rate Cut

If Tiff Macklem opts to cut interest rates in June, while the Fed decides to keep rates in restrictive territory for most of 2024, he may end up with the proverbial egg on his face. One reason is that CAD/US interest rate differentials would widen out in favor of the US dollar and lead to USDCAD demand. And that is inflationary as it would drive the price of US imported goods higher. At the moment, a 25 bp BoC rate cut is mostly reflected in the current exchange rate, so the tone of the monetary policy statement is key. A hawkish rate cut suggests the status quo, while a dovish cut could drive USDCAD to 1.4000.

Sometimes, being the leader of the pack means you get hit with the eggs first.