By Michael O’Neill

It is hard to know where you are going if you don’t know where you started. Ask Christopher Columbus. He landed in the Bahama’s and thought it was India. Donald Trump started the year in the White House but slunk away like a dead-beat tenant, and thanks to bans from Twitter and Facebook, tact and diplomacy returned to geopolitics. Former Teamster Union boss Jimmy Hoffa did not know where he was going when he was picked up on July 30, 1975, and now he is a housing development or a parking garage.

We are nearly halfway through 2021. How are December/January forecasts measuring up to reality? Did investors get lost like Columbus, get buried like Hoffa, or make out like Melinda Gates?

The COVID-19 pandemic was the wild card in most, if not all, forecasts at the beginning of the year.

Many economic forecasts carried a caveat about a third-wave coronavirus outbreak. The IMF World Economic Outlook published in January 2021 optimistically raised their 2021 global GDP forecast by 0.3% to 5.5%. They were concerned with renewed outbreaks. They were right.

Canada economic growth was forecast to grow around 5.4% to 6.8%. Those proved to be reasonably good guesses. Statistics Canada said Q1 GDP grew 5.5% annualized. The surprise third-wave coronavirus outbreak drove April GDP down 0.8%, but an aggressive vaccination program argues for a sharp recovery in May and June. Chalk another victory for the forecasters.

Economists and analysts predicted a post-pandemic economic boom fueled by massive government spending and persistently low interest rates. They nailed it. The S&P/TSX Composite gained 15.9% YTD, topping the three major US indexes ( S&P 500 13.1%, Dow Jones Industrial Average 12.2%, and NASDAQ 10.8%, as of June 22)

Treasury yields were expected to be tame. They weren’t. The median forecast for 10-year US Treasury yields in December 2021 was 1.20%, per a Reuters poll. Forecasters noted that a potential rise in inflation was a risk. So far, the 10-year yield forecast is well below the current 1.49% yield, but they were right about the inflation risk. CPI was expected to rise 2.3% in 2021 from 1.2% in 2020. It soared 5.0% y/y in June

Many FX forecasters were expecting the US dollar to slide. They anticipated that disappearing risk from Brexit, increased vaccinations in the US and globally, and the end of US political uncertainty because of the election would spark US dollar selling as safe-haven trades were unwound.

Some forecasts had EURUSD ranging from 1.2300 to 1.2700, due to positive, post-pandemic risk sentiment.

USDJPY was expected to drop to the 0.99-1.02 range due to a combination of reserve diversification and demand for Japanese bonds due to rising real yields. GBPUSD was expected to be around 1.3300-1.3500, due to economic underperformance from the Brexit hangover.

USDCAD forecasters were looking for prices in the area of 1.2700-1.3300 due to broad US dollar weakness, rising crude and other commodity prices and hopes for a successful vaccine roll-out.

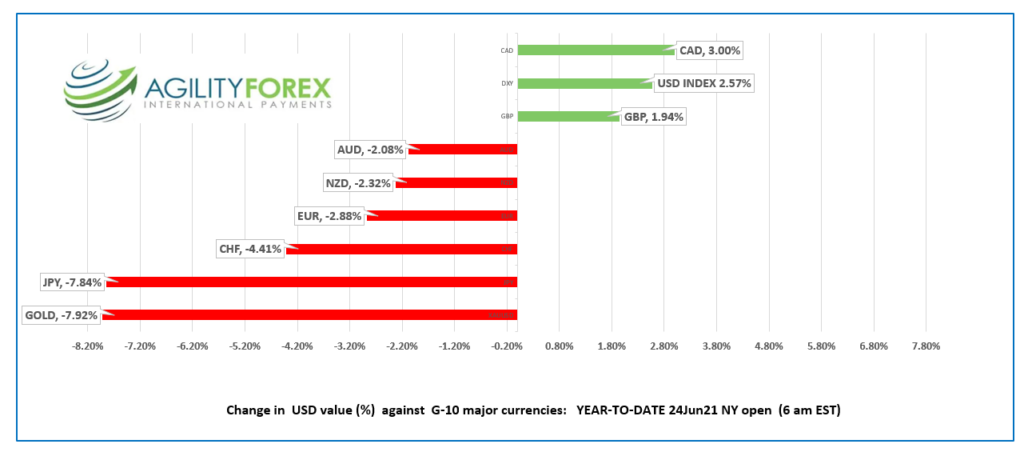

Chart: Year-to-Date performance of US dollar vs major G-10 currencies

Forecasters performed admirably in the first six months. Those forecasting economic fundamentals had a Christopher Columbus outcome; they got the direction right, although US inflation and GDP ran hotter than expected. FX predictions were of the Jimmy Hoffa variety; one day they were there, and the next day gone, never to be seen again.

If the US Founding Fathers were penning an H2 outlook, it would begin like this:

“We hold these truths to be self-evident, that the Fed will begin tapering, and interest rates are going higher.”

Tapering is a sure thing.

Its impact on markets is questionable.

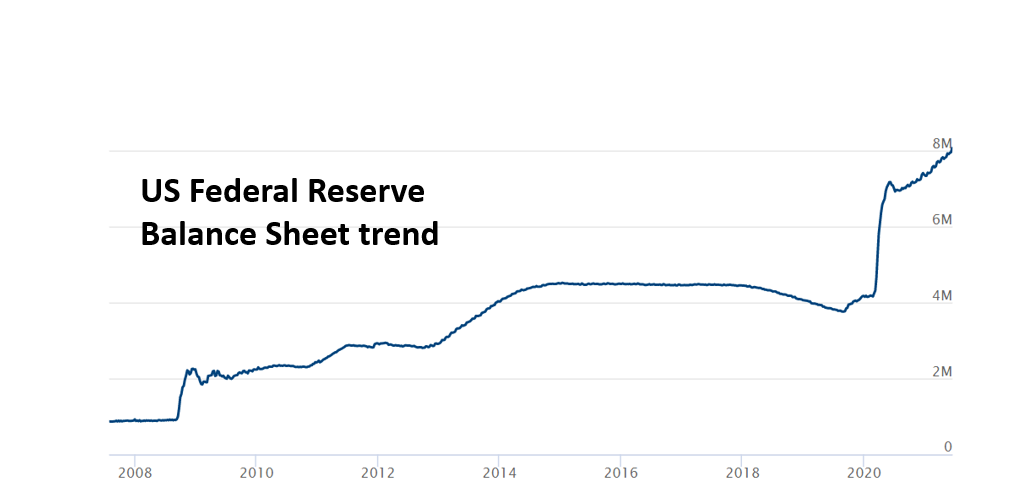

The Fed’s balance sheet ballooned from $4.2 trillion at the start of January 2020 to over $8.0 trillion in June 2021 as officials pumped $120 billion a month into the financial system in response to the pandemic. The monthly purchases are known as quantitative easing (QE) and the program to reduce the monthly purchases, tapering.

Tapering fears reached a crescendo following the June surge in US inflation, leading to carnage across asset classes. Treasury yields and the US dollar soared. The FOMC dot-plot projection of two rate hikes in 2023 rubbed salt into the wound.

Source: Federal Reserve

The market reaction to the mere thought of tapering is overdone. The Fed has not even started tapering discussions. It has taken the Fed over 33 months to pump in the additional $4.0 trillion of liquidity since January 2020. Tapering implies a reduction in purchases, and even if they reduced the existing QE program by 30%, it would take over 5/12 years to reach the pre-pandemic balance sheet level.

Bank of Canada Deputy Governor Toni Gravelle summed up the impact of tapering in a speech on March 23.

He said, “I want to be clear here: moderating the pace of purchases while adding to our holdings would simply mean that we are still adding stimulus through QE but at a slower pace. It would not mean we are removing stimulus.

We would be easing our foot off the accelerator, not hitting the brakes.”

The US dollar rallied after the dot-plot showed two rate hikes in 2023. The move was silly, and Fed Chair Jerome Powell said as much in his press conference, telling people to take the dot-plot projections with a “big grain of salt.”

G-10 economies are experiencing above-forecast inflation, with many central bankers attributing the rise to post-pandemic pent-up demand and supply chain bottlenecks.

In summary, buying US dollars on inflation-fueled rate hike concerns is probably a year or so too early.

However, if you are buying US dollars because American economic growth will far surpass the UK, Eurozone, Canada, and Japan, you may have a trade.

CIBC Deputy Chief Economist Benjamin Taj agrees. He told BNN recently that the market is pricing Bank of Canada rate hikes earlier and more aggressively than warranted. He says weaker inflation and slower Canadian growth that delays the closure of the output gap means the Bank of Canada will lag US rate increases.

If so, USDCAD will be a buy on dips.

The risk of looking through the rear-view mirror for an outlook for the next six months means you may not see the freight train coming right at you.