Source: Nintendo Switch

By Michael O’Neill

The FX market is not all its quacked up to be. Currency movements were once determined by intensive macroeconomic, technical, and statistical analysis, and guided by thoughtful central bank guidance.

Not anymore. Often price action has all the rationale of a meme stock surge.

Wild price swings are usually sparked by central bank miscommunication, sharp deviations in economic data from consensus forecasts, a herd mentality that is easily spooked with the USA as the common denominator.

And the FX market has gotten bigger.

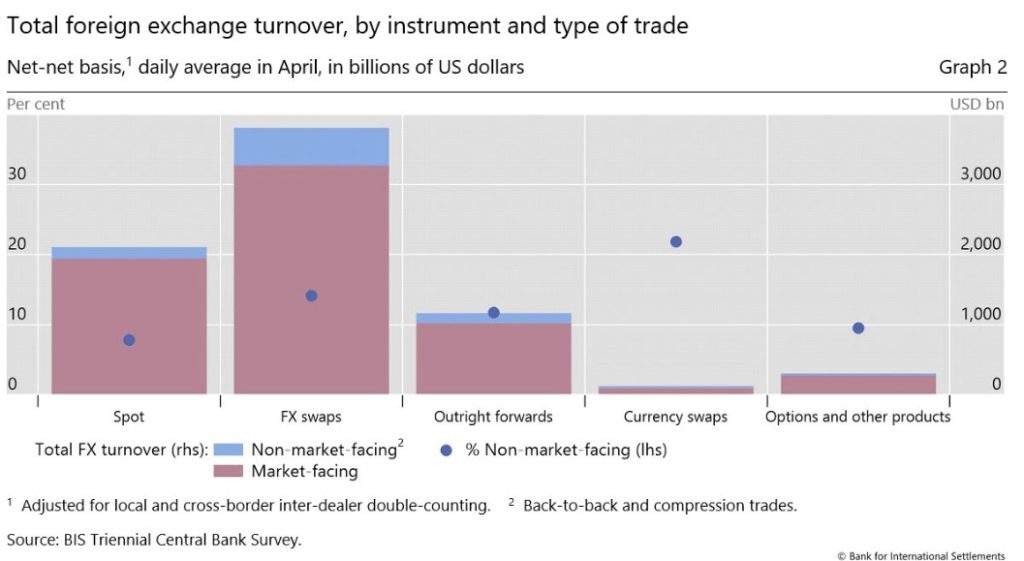

Fun with Figures: The Bank for International Settlements (BIS) released its Triennial Central Bank Survey of Foreign Exchange on October 27. The survey was conducted in April and involved central banks and authorities in 52 jurisdictions which collected data from over 1200 banks and other dealers.

The foreign exchange market turned over $7.5 trillion per day in April 2022, a 14% increase from 2019.

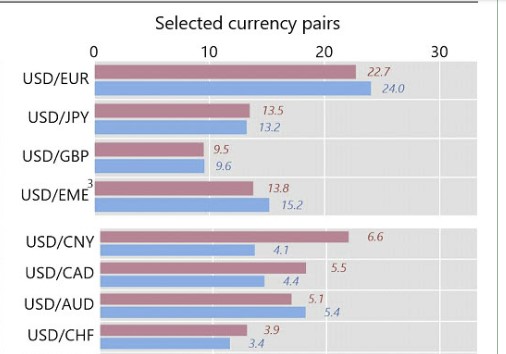

The USDCAD spot (same or next day delivery) share of that volume is US$172 billion, a 57% increase compared to the US$109.1 total in 2019, which represents about 5.5% of the daily total.

FX Market Turnover by currency pair

Source: BIS

The chief factor fueling FX volatility is that the US dollar is the most dominate currency. It is one side of 88% of all trades making Fed monetary policy decisions and outlooks the star of the show. The other major G-10 central banks merely have supporting roles.

The evidence is irrefutable. Just compare the impact of domestic influences on a currency pair with the recent price action around US employment data, or the FOMC monetary policy decision and even the US mid-term elections. No contest!

The furor around recent votes in Germany, Italy, Japan and even Brazil generated a lot of headlines and noise in their respective countries, but FX traders were apathetic.

Not so, with the US mid-term elections.

The American media is chock full of polls, and analysis about who will win control of the Senate and House of Representatives and it is still undecided a day after the vote. That’s because every state count votes differently and apparently no state officials have heard of the internet. Online gaming-sure, voting? Not a chance.

Traders’ reactions to rumours about which party is gaining or losing seats is condensed into risk sentiment as measured by the S&P 500 index.

If Republicans win the House (as expected) it raises the risk of policy gridlock, which traditionally has been bullish for equities. A rising US stock market improves global risk sentiment and weakens the US dollar.

The reality is the election is largely an entertaining distraction from parsing Fed policymaker comments and the discussion around terminal rates and pivoting.

It is that discussion that drives global risk sentiment and by US dollar direction. Nothing else. Even risk off fears of nuclear war, or China’s designs on Taiwan have a short shelf life.

The Canadian dollar may be the fifth most traded currency pair (excluding USD vs emerging markets), but its market share is dwarfed by the US Dollar.

The late former Prime Minister Pierre Elliot Trudeau said about this about America: “Living next to you is in some ways like sleeping with an elephant. No matter how friendly and even-tempered is the beast, if I can call it that, one is affected by every twitch and grunt. The same holds true for USDCAD traders.

Fed Chair Powell said he is focussed on lowering inflation, yet some Fed officials are suggesting that a slower pace of hikes is in order.

Richmond Fed President Thomas Barkin said “My personal hypothesis is that we’re on the back end…not on the front end. “Commodity prices seem to be cooling, supply chains seem to be easing up, excess spending is being spent down and the Fed is raising rates and doing what we need to do about it.”

His colleague Boston Fed President Susan Collins echoed the sentiment saying, “The risks of inflation falling too slowly and of the economy weaking too quickly are becoming more balanced,” “In my view smaller increments [of rate hikes] will often be appropriate, as we work to determine how much tightening is needed,”

Bank of Canada Governor Tiff Macklem is also signaled a slower pace of increases in order. He testified to the Senate Banking Committee November 1 and said, “we are trying to balance the risks of under- and over-tightening.”

However, USDCAD traders are far less concerned about Mr Macklem’s outlook than they are with the FOMC and that makes this week’s USDCAD performance questionable and arguably unsustainable.

USDCAD dropped from 1.3800 November 3 to 1.3389 November 7. The move was entirely due to a surge in the S&P 500 fueled by speculation the Republican’s would capture the House and the Senate. The rally happened in a thin, election day market, and poor liquidity conditions exacerbated stop loss US dollar selling. USDCAD found a floor in the 1.3380 range and a close above 1.3525 on November 9, implies a1.3380-1.3620 trading range.

FX markets are volatile but the November 8, USDCAD plunge was a sheer loonacy with the losses unsustainable.