By Michael O’Neill, FX Analyst

The Canadian dollar has had busy year and it is not even half-over. In January, the currency was at levels not seen in 13 years and the outlook was grim. At lot of blame for the negative sentiment was the fault of Opec and the Bank of Canada. Opec’s decision not to reduce or freeze production sent oil prices plunging. The drop in oil prices fueled expectations that the Bank of Canada (BoC) would reduce interest rates because the market believed that was the message being sent by the BoC. Consequently, USDCAD soared.

The BoC fooled a lot of people. The failure to cut interest rates on January 20, 2016 caught traders off-guard and off-side. The USDCAD decline was fast and furious and then the move took on a life of its own when oil prices started to rally.

But that was then, this is now. The frantic pace of the USDCAD decline has morphed into a consolidation phase between 1.2450 and 1.3000, coinciding with the WTI price rally stalling out in the $47.00/barrel area. It is not a coincidence that both the USDCAD decline and the WTI rally stalled at major support/resistance levels.

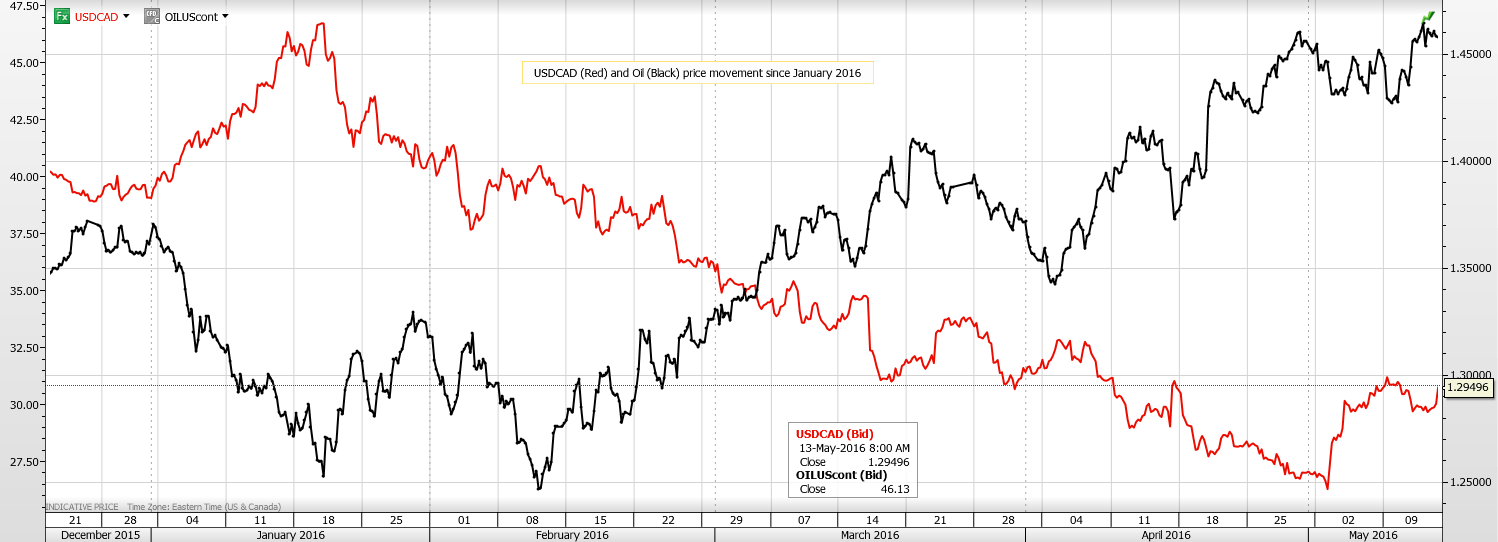

Chart depicts USDCAD price movements compared to WTI price movements since January 2016

Source: Saxo Bank

BoC takes a “time-out”

At the beginning of the year, the Bank of Canada, was a major factor influencing Canadian dollar direction and sentiment. But for the next few months, not so much. The April interest rate statement was on the doveish side due to the numerous references to downside risks but at the same time, the BoC expects a positive economic impact from the federal fiscal stimulus announcements. Combined, they have reduced the odds of a rate cut.

That sentiment is unlikely to change at the May 25 interest rate meeting, although the Fort McMurray evacuation and oilsands production interruption may have a short term negative impact. Therefore, if they are not cutting rates and they are not hiking rates, the Bank of Canada is on a “time-out”.

But the Fed is still “Live”

Janet Yellen and her colleagues on the Federal Open Market Committee have repeatedly said that “April is a live meeting”. Just last week, San Francisco Federal Reserve President, John William’s said that he would support a June rate hike. And today, the one-two punch of blow-out Retail Sales data and a strong Michigan Consumer confidence survey have temporarily knocked interest rate doves to the canvas. The US dollar has rallied on the news and will be finishing the week with a healthy gain against the G10 currencies.

With the Bank of Canada taking a “time-out, the FOMC has stepped in to fill the void.

Oil makes the Loonie go round

“Love makes the world go round” is an old adage. “Beyonce and a baseball bat makes Jay-Z come around” may be a more modern version but for FX traders, it is oil that gets currency markets turning.

The simple fact that oil is priced in US dollars means rising crude prices are good for countries that have lots of oil and not so good for those nations needing to import it. Canada is blessed by an abundance of crude and the Canadian dollar is closely tied to oil price movements.

That relationship has been on full display for over a year and that won’t change anytime soon.

Oil bulls think that there is more upside due to: a) Thursday’s Energy Information Administration (EIA) report projecting a 48% increase in world energy consumption by 2040. b) Opec’s prediction that non-Opec production will shrink in 2016. c) The 3.41 million barrel drawn down in weekly US crude inventories as reported by the EIA on Wednesday. d) supply disruptions in Nigeria and Canada. e) bullish technicals. The short term WTI technicals are bullish while trading above the $42.80-$43.20 area and looking for a break of resistance at $47.00 to extend gains to $48.20 and then $51.10.

Oil bears are not convinced that the “rebalancing” has run its course. The 4-week average of US crude production has declined from 9.6 million barrels in June of 2015 to 8.8 million barrels as of May 6 2016. Meanwhile, it appears that Iran has already filled that void and has plans to substantially ramp up exports. Saudi Arabia and Iran were never the best of friends and that relationship may have taken another hit.

Iran has reportedly been undercutting Saudi oil prices for export to Europe and Asia. Price cutting and market share woes don’t bode well for higher prices. Big oil may care about energy consumption 24 years from now but as a factor for intraday/intraday price moves, it is not. In addition, the intraday WTI rally appears to have stalled at $47.00/b. A break of $42.30-50/b suggests a deeper correction to $35.00/b is possible. The Canadian oil outage from the Fort McMurray fire is only a temporary blip with production expected to resume very shortly.

USDCAD balancing Fed and oil price expectations: Photo: Shutterstock

The fate of USDCASD is tied to the expectations for oil prices and US rates. The debate is which of the two factors will have the biggest impact in the short term.

Arguably, it is WTI. The FOMC doesn’t meet until June 15 and there is a ton of data, including another nonfarm payroll report which could upset the apple cart. The weekly Jobless claims report has posted two increases in claims in the past two weeks which suggests that the soft May 6 NFP may not have been an aberration.

That leaves oil to dictate direction. The oil price rally has stalled at $47.00/barrel. Fresh reports of price-cutting/market share grabbing between Iran and Saudi Arabia should limit WTI gains in the near term and open up a steeper downside probe. If so, USDCAD should head back to 1.3300. On the other hand, continued increases or even stability in the $45.00-$47.00/b area will act as a brake against USDCAD gains at least for the next couple of weeks.

The Fed, oil and the Loonie are so closely linked that Canadian data and the Bank of Canada will have very little influence on USDCAD direction, at least for the next couple of weeks.