By Michael O’Neill

The Loonie is singing, “My bags are packed, I’m ready to go, and I’ll go as far south as Laredo.”

The days of a relatively strong Canadian dollar are a thing of the past, and it is likely to get worse – a lot worse, and for a host of reasons, domestic and external.

It starts with monetary policy. There is a growing gap in interest rates between Canada and the United States. The Fed aggressively raised rates all year and last week indicated that another rate hike was likely. Even worse, they have no plans to lower rates in 2024. In contrast, the Bank of Canada has been decisively indecisive. They have adopted a hike-pause-pause-hike-hike-pause strategy since the beginning of the year. They don’t seem to be in a hurry to raise rates but fear that if inflation persists, it will become entrenched and, therefore, more difficult to contain.

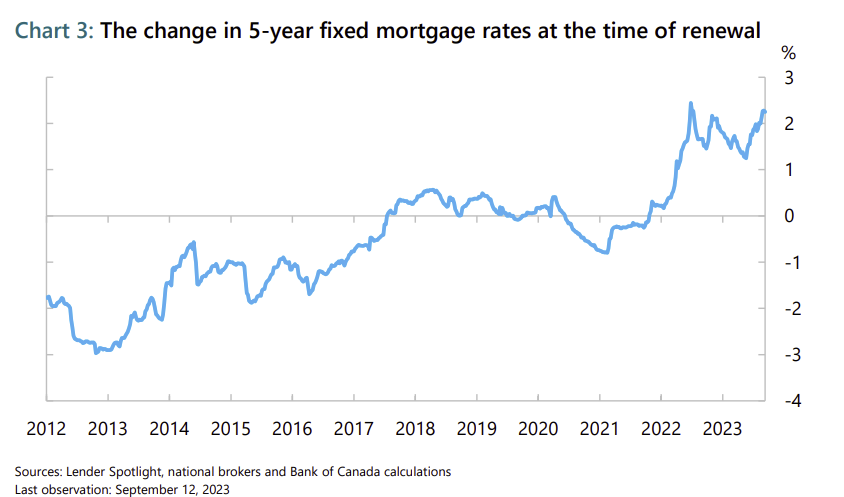

However, hiking rates to cure inflation is a delicate balancing act as consumers have accumulated significant debt, according to BoC Deputy Governor Sharon Kozicki. Last week she noted that “all five-year fixed-rate mortgages issued before 2022 will likely face significantly higher interest rates when they are renewed (Chart 3). That is what has been happening, and it could continue for an additional three and a half years. The resulting drag on spending could last even longer.”

It could also annoy the government. Deputy Prime Minister and Finance Minister Chrystia Freeland was effusive in her praise for the BoC’s decision to leave rates unchanged, saying, “It is welcome relief for Canadians. As the bank continues this work, my number one priority is to use all the tools at my disposal, and to work with partners at other levels of government across Canada, to ensure that interest rates can come down as soon as possible.” A rate hike could lead to a pink slip for a BoC governor because being an independent entity is just a nice theory.

Source: Bank of Canada

The Bank of Canada’s September 6 monetary policy statement highlighted a weaker economy and tightening labor market, with persistent inflation pressures. Hmm, that is close to the textbook definition of stagflation, which is defined as an economic situation with slow economic growth, elevated inflation, and high unemployment.

Now unemployment isn’t an issue just yet, but if Canada continues to accept 100,000 immigrants each month while creating just 40,000 jobs, it soon will be. The unemployment rate has been steadily climbing, rising by half a point in just three months, hitting levels we haven’t seen since January 2022.

Some forecasters are painting a gloomy picture for Canada’s 2024 real GDP outlook predicting no growth at all. The forecast is in the minority and stands in contrast to the consensus view of 0.6% growth and the Bank of Canada’s rosier projection of 1.2%, as outlined in its July Monetary Policy Report. Nevertheless, it is a risk.

The Canadian dollar is often described as a commodity currency. That’s because 30% of its GDP is derived from exports, and mineral fuels, precious metals, aluminum, ores, and fertilizers account for 44% of the overall value of exports. Those exports have been taking a hit since peaking in 2022, which is a Canadian dollar negative. Sure, oil prices may continue to rise, but if the other commodity exports do not follow suit, the benefit of higher crude price on the loonie may be limited.

Source: Bank of Canada

USD/CAD has been relatively unscathed in September. It lost a mere 0.14% between the September 1 and September 27 NY opens. It’s time is coming.

Meanwhile, the British pound got hammered, plunging 4.18% as investors fear that high UK rates will drive the country into a recession. The Bank of England surprised markets when they left interest rates unchanged last week, and traders scrambled to downgrade forecasts for future rate hikes. The odds are about 50/50 that rates will remain at 5.25%. Traders also fear that the UK is headed for a long period of stagflation.

Many traders were blindsided when Russia invaded Ukraine. USD/CAD surged on the news as investors flocked to the safe haven of US dollars. China could trigger an even worse reaction if President Xi Jinping feels a need to deflect attention from his bungling and invades Taiwan. History is rife with dictators using war to burnish their images.

The combination of geopolitical risks, interest rate differentials, diverging central bank policies, and the rising risk of a recession in Canada suggests USD/CAD may have further upside. USD/CAD has been trending higher since the pandemic low of 1.2020, and a break above 1.3660 targets 1.4000, then 1.4660.

The Loonie’s bags are not just packed; they have already left the building.