By Michael O’Neill, Agility FX, Senior Analyst

“Is the BoC truly optimistic or what is really in that glass?” Photo BoC

There may be better days ahead for the Loonie. At least that will be the case if the Bank of Canada’s economic outlook proves to be prophetic.

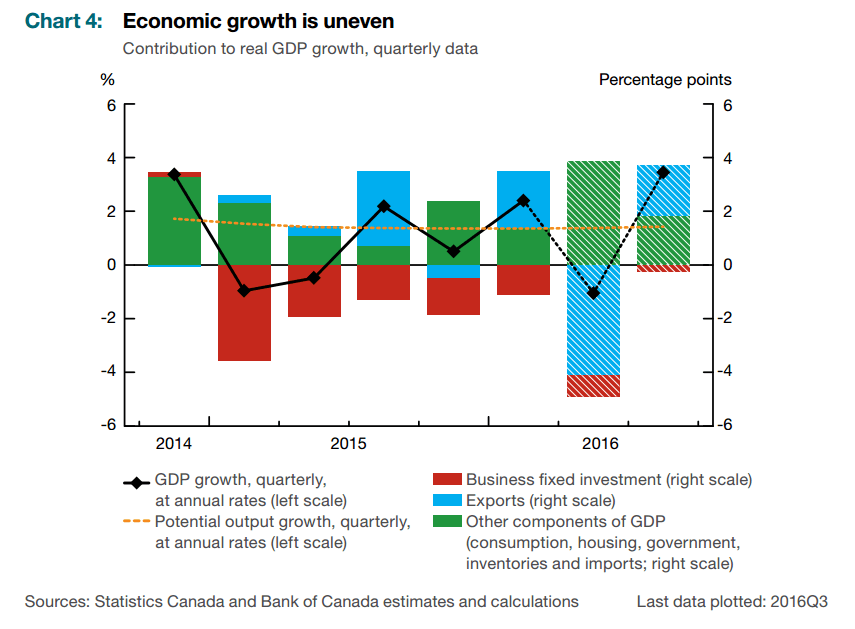

That’s because the Bank of Canada forecast Real GDP growth in the second half of 2016 will be an eye-popping 3.5%, a sizeable leap from the April prediction of 2.2%.

The BoC left the overnight rate at 0.5% while the Bank Rate is stuck at 0.75%. That wasn’t a surprise although there were a few traders who were mildly nervous about the possibility of a rate cut, noting that the BoC has surprised markets before, most notably in January 2015. Prior to the announcement, the odds for a rate cut in 2016 were 31%. According to Bloomberg, they are now just 16%.

There are many reasons for the second half optimism. The impact from the Alberta wildfires will have dissipated as lost oil production gets fully restored and as the rebuilding effort gets underway. Federal infrastructure spending and other measures, including the child tax credit are expected to provide an economic boost as will a rise in exports, driven by solid US economic growth.

The medium term outlook for inflation is 1.6% in 2016 and 2.1% in 2017. Although inflation will remain below the 2% target in 2016, the BoC believes that disinflationary pressures from weak energy prices and excess capacity will gradually dissipate.

Even Brexit, the UK’s decision to exit the European Union, won’t have much, if any impact on Canadian growth, at least in the second half. That is because the UK only represents a tiny 2.4% of global GDP.

Source: Bank of Canada, MPR

Of course there are risks to the outlook and the BoC was not shy in pointing them out. Those risks include; sluggish business investment, weaker household spending a slowdown in US economic growth and global growth, a more dysfunctional Brexit negotiation and slowing growth in emerging markets, particularly China.

Canadian dollar traders liked what they heard. USDCAD plunged from a pre-announcement level of 1.3076 to 1.2938 after the news.

The lowered rate cut expectations helped fuel today’s USDCAD decline as did positioning. FX traders were long USDCAD going into the BoC meeting, supported by bullish technicals and soft oil prices with a dash of risk aversion trading concerns thrown in for good measure. They were also comforted by USDCAD’s inability to break below support at 1.2980. They got it wrong and the break triggered intraday stops.

Today’s Monetary Policy report and interest rate statement provided valuable insight into the domestic economy but for USDCAD traders it is only part of the equation driving Canadian dollar direction.

Photo: shutterstock

Shifts in global risk sentiment have wreaked havoc in FX markets and USDCAD is not immune. Markets have seen these shifts many times since the June 23rd Brexit vote. It doesn’t take much to stampede an optimistic risk-seeking market into a risk-off panic. When risk is off, USDCAD gets bought and when it’s risk-on, USDCAD sellers emerge.

Oil price fluctuations are another source of USDCAD instability. The positive price outlook that was evident April was predicated on declining US inventories, a forecast for falling non-Opec production and rising demand from China. Those forecasts have taken a hit in the past month. Expected declines in US crude stocks haven’t materialised. One analyst pointed out that this is the time of year for US crude inventory draw downs. The problem being that inventories are at twice the level they were at in 2015 and the pace of declines is just half of last years’ decline.

To make matters worse, the intraday WTI technicals are bearish since breaking below $47.75 on June 9th. The ensuing downtrend has contained numerous rallies and remains intact while prices are below the $46.90-$47.10 area.

Another key factor for the Canadian dollar is the US economy and the direction of interest rates. Recent American economic data has been positive and last Friday’s 287,000 gain in nonfarm employment washed away the stench of May’s 11,000 gain. That data has kept US rate hike hopes alive. The CME FEDWATCH Toll assigns a 66.6% probability of a December rate increase. Rising US rates when Japan and the ECB have negative rates keeps US dollars in demand.

The health of the Chinese economy and the government’s ability to engineer a soft landing poses risks to the global economy and by default Canada.

All of the above risks are well known and therefore imbedded in the current exchange rate. The Bank of Canada’s view on the Canadian economy is just one more factor that will drive the currency in the coming weeks and months while the 1.2500-1.3200 range since mid-April, is likely to remain intact for the rest of the summer.

.