By Michael O’Neill

The Fiscal Circus Comes to Canada

The fiscal circus comes to Canada on April 16, and the clowns are in the center ring. Finance Minister Chrystia Freeland will unveil the Liberal government’s fiscal outlays for 2024-25. Meanwhile, her boss, Justin Trudeau, is running around the country pre-announcing spending initiatives designed mainly to improve Liberal re-election prospects. That’s not hyperbole.

According to March 31 data on 388Canada.ca polling suggests that if an election were held that day, the Liberals would lose 93 seats, while the NDP (Jagmeet Singh’s party) would lose 7 seats. Pierre Poilievre’s Conservative Party (PC Party) would win a 210-seat majority government. This explains why the current government will spend billions of taxpayer dollars, much of it yet to be collected, to reverse the trend.

Spending Spree Has Already Begun

Just this week, Justin Trudeau announced a $15 billion top-up for the federal government’s construction loan program. This is in addition to the recently announced $6 billion Canada Housing Infrastructure Fund. Renters weren’t forgotten either, as Trudeau promised to create a new Canadian Renter’s Bill of Rights (conveniently ignoring that renting falls under provincial jurisdiction). This comes on top of the expanded $10/day daycare program. Earlier, the federal government announced plans for a single-payer, universal drug plan, which the Parliamentary Budget Office estimated would have an annual cost of about $12 billion. This news followed the announcement of a new $13 billion dental-care program for children and seniors.

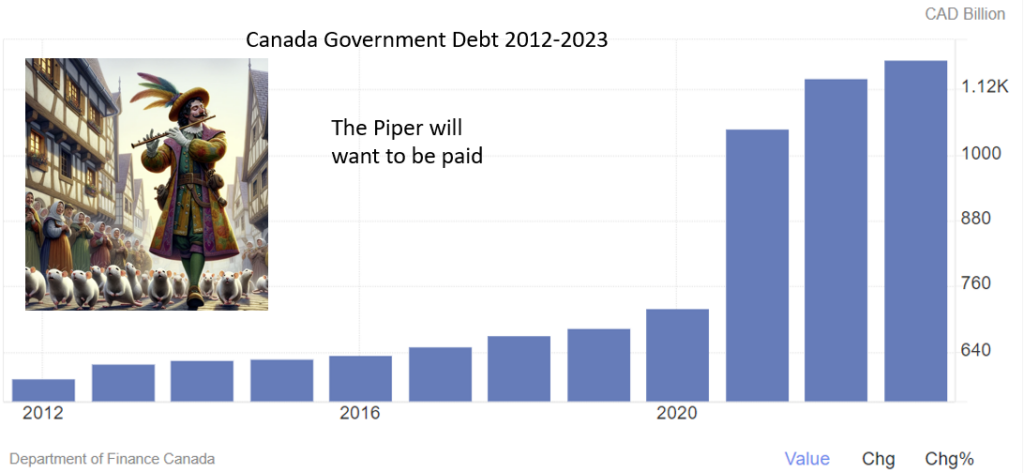

Concerns About Long-Term Economic Impact

Such fiscal maneuvers raise questions about the long-term economic implications of massive government spending. A Fraser Institute report, “The Growing Debt Burden for Canadians: 2023 Edition,” authored by Jake Fuss, examines the fiscal trajectory of Canada’s federal and provincial governments. It meticulously outlines the doubling of combined federal and provincial net debt from $1.1 trillion in 2007/08 to a projected $2.1 trillion in 2022/23, marking a significant fiscal shift. This escalation accelerated when Trudeau was first elected, signifying an upward trend in government indebtedness relative to the country’s economic output.

Other Economic Considerations

Other economists point out that underlying inflation risks, which have remained sticky and are above the Bank of Canada’s mandated target, could be exacerbated by higher government spending. If so, it would mean hardships for households with hefty mortgages coming up for renewal. The problems have already begun. Equifax Canada reported that consumers in Ontario and British Columbia increasingly missed mortgage and credit card payments in the fourth quarter of 2023. Mortgage delinquency rates rose 52.3% in Q4 2023 compared to the same period in 2022.

Canada’s Debt Position

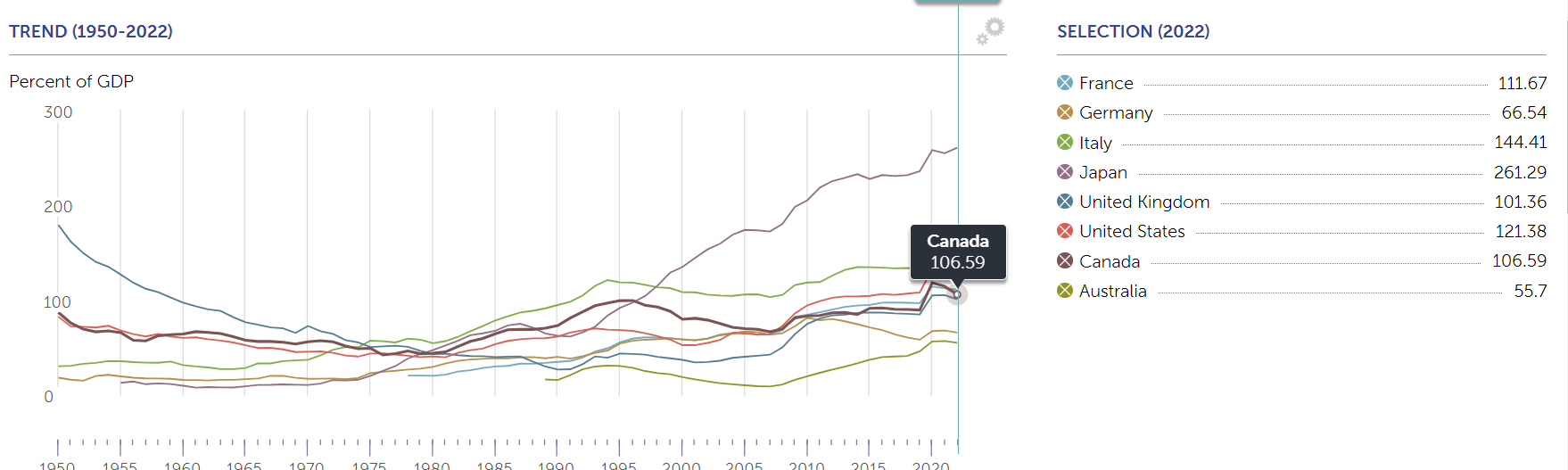

But does it really matter? Worldometers.info claims that 7,009,336 people died after testing positive for COVID-19. Worldwide government fiscal restraint was just another casualty.

The data may be old, but despite spending the third-most on COVID-19 policies, the International Monetary Fund (IMF) shows Canada with the fourth-lowest debt-to-GDP ratio among the G-10 as of 2022

Source: IMF.org.

The Dominance of the U.S. Federal Reserve

The Bank of Canada’s monetary policy decision is due on April 10, and on April 18, the federal government tables its budget. Previously, these were highly anticipated events due to their potential market-moving impacts. However, in the current landscape, the Federal Reserve is the only central bank that truly sets the global tone.

The developed world may be moving away from international supply changes in favor of domestic industry, but that’s not the case for financial markets. The U.S. Federal Reserve, led by Chair Jerome Powell, plays a crucial role in shaping monetary policy across developed markets. It acts as a central figure whose decisions significantly impact global finance. Its policies on interest rates and quantitative easing set benchmarks that other central banks and financial markets often follow or react to.

The Influence of the Fed on the Loonie

When the Fed makes a move, whether tightening or loosening its monetary stance, markets worldwide tend to respond, highlighting the Fed’s influence beyond the U.S. economy. The Fed’s policy announcements tend to dictate the course of action for global investors and central banks, all of whom adjust their strategies based on the Fed’s actions.

The Bank of Canada is no different. They claim to be independent and make decisions based on Canadian economic data. However, the evidence suggests otherwise. How else would you explain the Bank of Canada’s adoption of the terms “quantitative easing,” “quantitative tightening,” or “transient inflation,” which first appeared in Fed communications?

The dollar will likely rally when the Fed is on the cusp of cutting interest rates. While Fed officials aren’t suggesting any rate moves until the second half of the year, sending in the clowns in Ottawa, could make the Loonie vulnerable for a brief moment. However, its overall direction will be determined by broad-based U.S. dollar sentiment.