By Michael O’Neill, Agility Forex, Senior Analyst

Many Canadians have been admonished about crying over spilled milk. But that’s exactly what Canadian dairy farmers were doing on April 18.

That’s the day President Trump aimed his NAFTA “tweaking” blunderbuss squarely at the heart of Canada’s dairy farmers. The president told a Kenosha Wisconsin audience; “We are going to stand up for our dairy farmers in Wisconsin… that demands really, immediately fair trade with all our trading partners, and that includes Canada,” he said. “Because in Canada, some very unfair things have happened to our dairy farmers. And we’re going to start working on that.”

He went on to say that what was happening to Wisconsin dairy farmers was “very, very, unfair” adding “it was another typical one-sided deal against the United States and it’s not going to be happening for long.”

Canadian dairy farmers didn’t just cry, they went on the offensive. The Canadian Ambassador to the United States David McNaughton sent a letter to the governors of New York State and Wisconsin. In it he wrote that the US problems are due to US and global overproduction. He went on to say that Canada’s dairy industry is less protectionist that that of the US which has employed technical barriers to keep Canadian dairy out of US markets. So there!

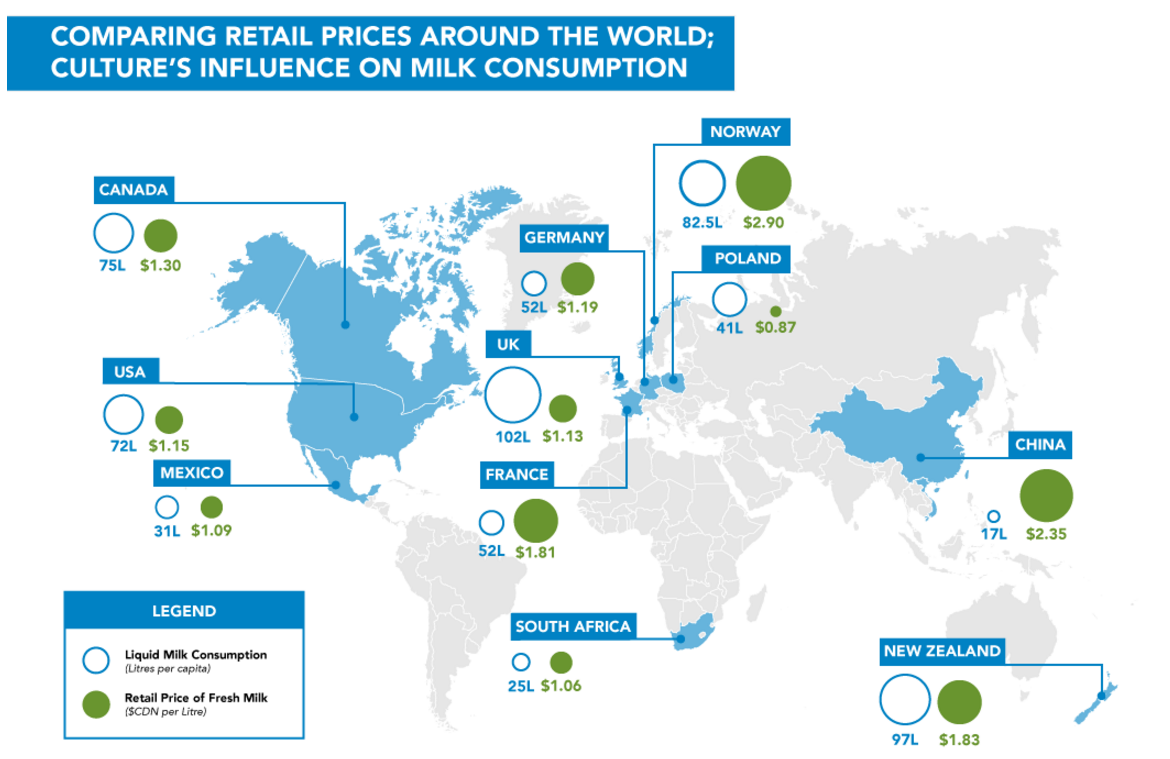

US dairy farmers say “not so fast”. They have their udders in a knot over ultrafiltered milk. UF milk is a milk protein concentrate used in the production of cheese and yogurt.

Under NAFTA, US producers have complete access to Canada for this product.

The Dairy Farmers of Canada disagree. Making matters worse, the Canadian government is actively pursuing a strategy of incentives to encourage local producers to buy ultrafiltered milk locally. And that strategy is why the American’s are so miffed.

The $200 million dollar UF milk industry is barely a rounding error when it comes to the $575 billion in two-way goods trade between Canada and the United States.

For President Trump and his “Fair Trade, not Free Trade” campaign promise, it’s an easy win.

FX traders know it, which is one of the reasons why the Canadian dollar has been under pressure since just before Easter.

There is more to the Canadian dollar weakness than just sour milk. Foreigners are dumping oil-sands assets.

At the beginning of March, Marathon Oil sold its Canadian subsidiary to Shell and Canadian Natural Resources for $2.5 billion in cash. On the same day, Shell announced that all of its undeveloped oil-sands assets and reduce its share of Athabasca Oil Sands from 60 percent to 10 percent. The combination of those sales would give Shell $7.25 billion. ConocoPhillips got into the act on March 29 with news that it agreed to sell oil-sands and natural gas assets to Cenovus Energy for $17.7 billion.

That adds up to $27 billion Canadian dollars. Assuming the sellers do not want Loonies, it could mean serious USDCAD demand. Realistically, that scenario is unlikely. The use of cross currency swaps, US dollar loans and existing US dollar cash suggests that USDCAD demand from these transactions will be substantially smaller and possibly negligible. Nevertheless, the mere thought of massive Canadian dollar selling, gave FX traders reason to buy USD dollars.

The French election and British Prime Minister Theresa May’s surprise election call have combined to undermine the Canadian dollar, as well.

The first round of the French presidential election is Sunday April 23. It is a vote between the far right, anti-euro, Marine Le Pen, pro euro, independent centrist Emmanuel Macron, and center right, Republican candidate (and former Prime Minister) Francis Fillon. The polls suggest that the race is extremely tight yet speculation that Mr. Macron will win has lifted EURUSD in recent days. The Canadian dollar was collateral damage due to EURCAD demand.

The UK election caught Britain and the rest of the world by surprise. That’s because Theresa May had previously denied any plans for a vote. That led to GBPUSD and GBPCAD buying.

Oil prices have dropped sharply after peaking at $53.73 on April 10 and that drop seems to have had an outsized impact on the Canadian dollar. Nevertheless, oil prices have been in an uptrend for the past year and the prospect of Opec extending production cuts should continue to support prices.

President Trump’s verbal assault on the Canadian dairy industry, oilsand divestitures by foreign investors, the oil price decline and French and UK politics have led to a 2 percent decline in the Canadian dollar, since April 13.

That move is nothing to “moo” about. However, it is not “lights out for the Loonie.” Not by a long shot.

The USDCAD strength has occurred around major holidays when liquidity is not the best which may have exacerbated the move.

The 2017 USDCAD range is still intact and the currency is well below the top of the range.

The Bank of Canada has shifted its monetary policy stance to “cautiously neutral” from doveish which has led forecasters to predict an interest rate increase in the last quarter of this year.

Trade, oil, and politics may be driving Canadian dollar direction now. Yet, it is only a matter of time before the focus shifts back to domestic economic data and monetary policy which should ensure better days ahead for the Loonie.