Photo: HDclipartall.com

By Michael O’Neill

Were you surprised by the Fed’s hawkish 50 bp rate hike last month? You were supposed to be.

The minutes from the December 14 FOMC meeting revealed that the Committee’s upward adjustment of interest rate projections and inflation forecasts was a manipulation of forward guidance in a calculated effort to manage financial market expectations.

It was a deliberate attempt to convince financial markets that speculation about a “fed pivot” was very premature. The FOMC wanted to “clearly communicate that a slowing in the pace of rate increases was not an indication of any weakening of the Committee’s resolve to achieve its price stability goal or a judgment that inflation was already on a persistent downward path.”

And just in case the market did not get the message, the minutes emphasised that “No participants anticipated that it would be appropriate to begin reducing the federal funds rate target in 2023.”

However, like all good central bankers, they hedged themselves. They noted that “uncertainty associated with their economic outlooks was high.”

According to the minutes, the risks to the inflation outlook remained tilted to the upside, or downside, depending upon who you asked.

Does that make you confident?

The Fed was out to lunch at the start of 2022. They failed to realize that if something was transitory it meant it could move in more than one direction. They admitted inflation was well-above 2% at the January 24 meeting, but like a deer caught in the headlines, they didn’t react until they got run over.

Bank of Canada officials were not much better. They ignored inflation readings that were well above mandated levels and then were forced to drive interest rates 400 bps higher to 4.25% by year end.

The December monetary policy statement suggested that they BoC may be close to deciding that the current rate hike cycle is over, which may happen January 25, with a 25 bp rate hike.

That’s because they hope the inflation genie gets stuffed back in the lamp.

Source: Disney

Many analysts expect that the Consumer Price Index (CPI) will drift lower throughout 2023. BMO economists are predicting that Canadian inflation will be lower than the UK, Euro area, US, and Australia. Kudos for Canada.

The BoC may be enroute to declaring victory in its inflation fight but it could be the pyrrhic kind. Low inflation will be a small comfort to those who find themselves unemployed due to a recession.

The severity of a recession, if it occurs, may be exacerbated by the Organization of Petroleum Exporting Countries (Opec)

Cartel members were rubbing their hands with glee after the US and EU led a host of countries in imposing sanctions and outright bans on Russian energy exports after Putin’s army invaded Ukraine. They were hoping depriving the world of Russian crude would boost prices well above $100.00/barrel for Brent and West Texas Intermediate.

It happened, but only for about four months. Prices have since retreated to pre-invasion levels.

Opec is not amused and is reportedly making plans to increase prices to take advantage of projected 2.2 million barrels/day increase in world demand in 2023.

That should be good news for USDCAD bears as historically prices tend to fall when WTI rises. However, that relationship has hit some speed bumps. The Federal government’s aggressive anti-oil agenda has sharply curtailed foreign investment in Canada’s energy industry. Less foreign investment means less Canadian dollar demand.

The S&P 500 index has had more influence on USDCAD direction than day to day oil price swings in recent months as the index is considered a barometer for risk sentiment. The Fed’s interest rate path is the key driver of risk sentiment (ignoring geopolitical issues and events) which suggests the risk sentiment will improve the closer the Fed gets to its terminal rate.

However, if the December 14 minutes are a guide, the Fed does not even know the level of the terminal rate and they do not have a lot of faith in their economic outlook.

That suggests that USDCAD will be rangebound in 2023.

The long-term technicals agree.

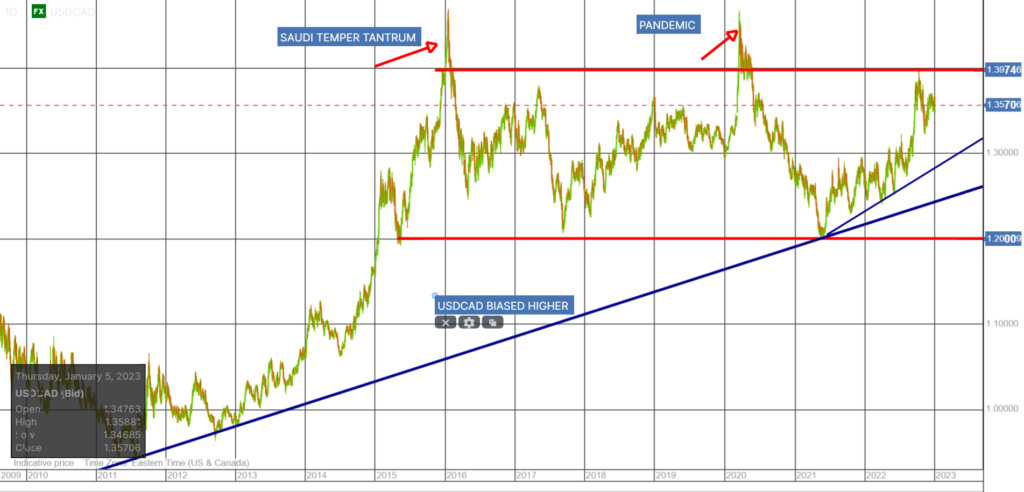

USDCAD has been trading with an upward bias since July 2011 and has been content to bounce in a 1.2000-1.4000 range since 2015, ignoring two spikes above 1.4000 which were anomalies.

USDCAD was above the 1.2970 area between October 2018 until November 2020. It dropped to 1.2020 in May 2021 then climbed steadily until decisively breaking above 1.2970 in August 2022. The USDCAD uptrend from July 2011 is intact while prices are above 1.2440, a level guarded by the June 2021 uptrend line at 1.2780.

The risk that the BoC fails to keep pace with Fed rate hikes should provide another layer of support to the 1.2970 uptrend line and leave USDCAD wanting to probe resistance at 1.4000

The FOMC may have massaged the message but there is unlikely to be a happy ending for the Canadian dollar.

Source: Saxo Bank