By Michael O’Neill, Agility FX Senior Analyst

November 1, 2016, All Saints Day in many parts of the world, will henceforth be known as Morneau Debt Day in Canada. Well, maybe not, but Generation X and Millennials will remember this day as the day their version of “Freedom 55” became “WageSlave 75”.

Canada’s Finance Minister, Bill Morneau, fresh off tabling a March budget with a $29.4 billion deficit and promising “A New Approach”, delivered his Fall Economic Statement 2016”. He called it “A Plan for Middle Class Progress”. He wasn’t very clear if it was progress to prosperity or progress to poverty.

“Let me tell ya, when it comes time to pay back all this debt, it won’t be my problem”. Photo Canada Dept. of Finance website.

“Let me tell ya, when it comes time to pay back all this debt, it won’t be my problem”. Photo Canada Dept. of Finance website.

Whoever coined the phrase “talk is cheap” never met a Federal Liberal Party member. When Mr. Morneau started talking on November 1st, the Liberal Party planned on spending $120 billion dollars in infrastructure spending over 10 years. When he finished speaking, an hour later, the government was spending $186.0 billion over the next 11 years. This “Plan for Middle Class Progress” just cost Canadian’s another $66.0 billion dollars. Canadian’s can’t afford to have any more Liberal government budget updates.

A cornerstone of the Liberal plan is the Canada Infrastructure Bank. Its purpose, described as a true win-win, is to identify a pipeline of potential projects and identify investment opportunities that provide the biggest economic, social and environmental returns.

They cite the example of Vancouver’s Canada line as evidence of a successful Public Private Sector partnership. The $1.9 billion-dollar project delivered $92 million in savings by working with the private sector. That amounts to a mere 4.8% which in multi-billion budgets, is a rounding error. As for win-win; check out BC Hydro or Ontario’s Hydro One. The win-win applies only to employees and government coffers.

What Mr. Morneau didn’t tell you was how much it would cost the government to create a brand-new department and how many employees it would require. In addition to expanding the deficit, he is also expanding the public service.

Mr. Morneau also indulged in the time-honour tradition of playing “Fun with Figures”. In the March budget, the Finance Minister allocated $6.0 billion for contingencies in his announced $29.4 billion deficit. The Fall Update says the deficit is now only $25.1 billion. “Wow” you say. “That’s great money management. What a fine steward of public finances you are proving to be”.

Except he isn’t. There is no longer a $6.0 billion contingency fund. In fact, that projected deficit in March actually widened by $1.7 billion. If he was Pinocchio, his nose would have grown a foot.

“Really, its true. The budget deficit is lower” Photo: Shutterstock

Mr. Morneau is hoping that these initiatives lead to prosperity for all Canadians. Building new highways is a great idea. That would allow workers in Ontario to drive to their auto manufacturing jobs that have relocated to Mexico. It isn’t very clear how $80 billion in infrastructure spending will offset the planned carbon taxes which will place the Canadian oil industry at a competitive disadvantage. Ottawa’s loss of oil industry tax revenue will exacerbate the rising deficit.

The fact is the Canadian economy was stagnating. Extremely low interest rates and a fixation on a balanced budget weren’t providing any economic stimulus when Stephen Harper’s Conservative government was calling the shots. Something had to change. The Federal government and various provincial governments, particularly Ontario, are running up massive debt and budget deficits. The question is whether the Canadian economy can grow fast enough to sustain the level of debt.

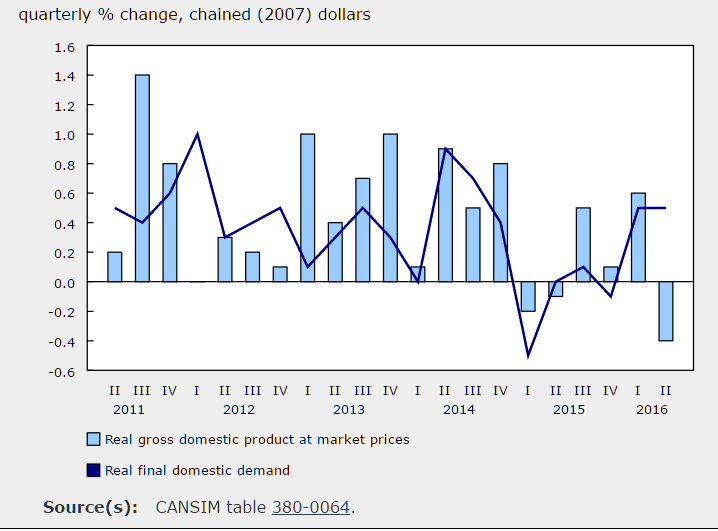

Chart: Canada GDP

Source: Statistics Canada

The Bank of Canada is doing its part to encourage domestic economic growth. The governor, Stephen Poloz, indicated at the Oct 19 monetary policy press conference that the governing council discussed cutting interest rates, knowing full well that the Canadian dollar would weaken. A weak currency leads to increased exports.

Despite the efforts of the Finance Minister and the Bank of Canada to jump start the domestic economy, external influences will hamper their efforts. Global economic growth is stagnant, oil supply has outpaced demand, Brexit has raised economic uncertainty concerns across the Eurozone and China is still engineering a “soft landing” for their economy. The US is hiking interest rates which may lead to additional stress on emerging market economies. Next week’s US election has added another layer of uncertainty around the globe.

The Canadian government has ramped up deficit spending at a time when the growth rate of the population aged 65 years and older was about 4 times the growth of the total population. That implies a bigger drain on health care and social security costs.

Who is going to pay for all of this? That would-be Generation X and Millennial’s.

The ever-increasing amount of provincial and federal government debt may have this cohort clamoring to change the national anthem from O’ Canada to Big Sugar’s 1996 classic, “Digging a Hole”.