By Michael O’Neill

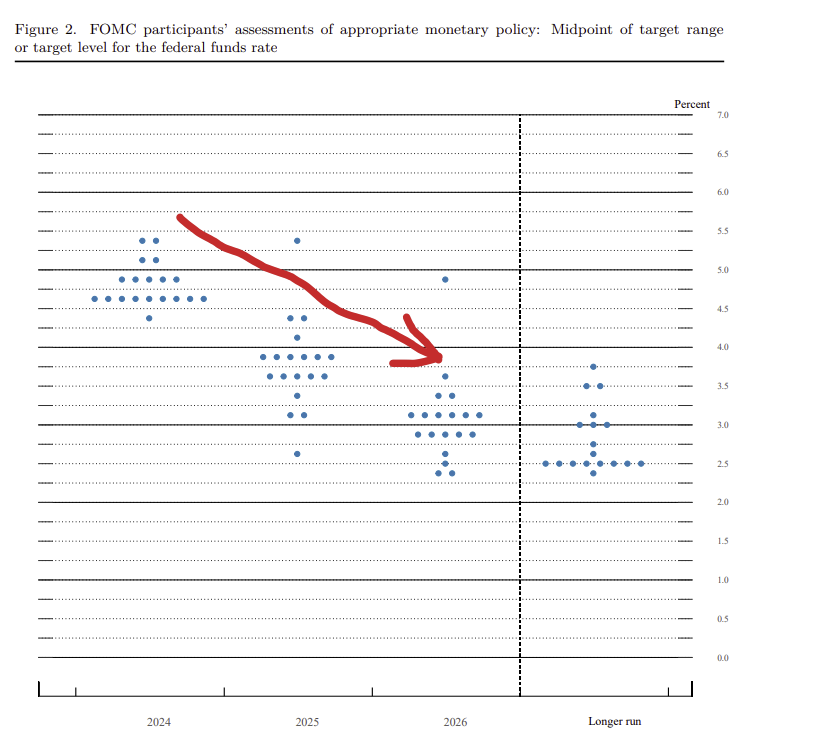

The Fed left interest rates unchanged as was universally expected but traders were sandbagged by the Summary of Projections dot-plot. The dots indicated officials were still looking for three rate cuts in 2024, the exact same as they did in December.

Source: FOMC SEP

Rate hike hawks were left looking really, really sheepish. They had decided that recent robust nonfarm payrolls employment numbers and a tick higher in inflation was proof-positive that the Fed would only cut rates twice (if that) in 2024.

If Fed Chair Jerome Powell was a university professor, he would be tapping his pointer on the chalkboard and saying, “You are not listening. I have said repeatedly that inflation is coming down gradually, but the road is bumpy. The recent data has not changed the overall story.”

Equity traders were elated, and they drove the S&P 500 above 5,200. Gold bugs got into the act, and XAU/USD rose to over $35/oz, and the US dollar index (DXY) plunged from 103.81 to 103.04. Bond traders were less enthusiastic, and the US 10-year Treasury yield was steady at 4.285%.

The reality is that the Fed is sticking to its “meeting by meeting” mantra and rate decisions will be dependent on incoming data. Nothing new there which suggests the period of low FX volatility that has characterized activity since the beginning of the year will continue at least until May.

Tiff’s Juggling Act

The Bank of Canada has a dilemma. What do they do about interest rates? Policymakers told Canadians that interest rates would go lower when inflation returned to target. Headline and core inflation fell into the 1-3% target zone, but rates were left unchanged. That suggests that the data-dependent, error-prone policymakers (from even before the onset of the pandemic), are afraid to act. It’s a fair conclusion when comparing the Summary of Deliberations from the January and March meetings.

Governing Council explains the decision to maintain the policy rate at 5% in both January and March meetings by claiming it is strategic patience aimed at allowing previous rate hikes to permeate the economy. They justify leaving rates unchanged by saying that more time is needed to observe the full effects of monetary policy adjustments on inflation and economic activity.

They acknowledged that inflation was easing but continue to be very concerned about shelter price inflation which climbed from 6.2% y/y in January to 6.5% in January. And that is the real reason why Canadian interest rates are not going lower any time soon. The country is already experiencing rising housing and rental accommodation prices which the Federal government exacerbated by bringing in over 1 million immigrants in 2023. These people need a place to live, and they are contending with a severe shortage of accommodation of any type. A BoC rate cut would exacerbate the situation as lower prices would likely renew the bidding war practice of a few years ago.

More than likely, the BoC was probably unwilling to commit to a course of action until the March 20, FOMC meeting. And for good reason. All the angst about higher US rates evaporated after the SEP revealed Fed officials still expected to cut rates three times in 2024, the same as they did in December. That huge gust of air you felt around 11:00 am (PDT) was a collective sigh of relief from the Governing Council when the members saw the dot-plot.

The FOMC meeting managed to yank the Loonie from the brink of the abyss. USDCAD was threatening to blow the top off the 2024 peak of 1.3614, setting the stage for a new period of strength.

That’s not going to happen now. USDCAD is comfortably ensconced in its well-defined 1.3200-1.3600 range that has contained price action since the start of the year. When Fed Chair Powell said, “Listen up,” BoC Governor Tiff Macklem heard him loud and clear, and his interest rate dilemma gradually diminished