The roar you heard, right at 1900 GMT, on December 16th, was the groan of global financial markets saying in unison “that’s it, that’s all there is”?

Janet Yellen, Chair of the Federal Reserve, and her colleagues on the Federal Open Market Committee, raised the overnight interest rate target from 0.00%-0.25% to 0.25%-0.50%. And nothing happened.

For the past 12 months’ traders, analysts, talking heads and even cab drivers were warning all who would listen of the dire consequences to global markets when the Fed finally hiked rates and put an end to seven years of zero interest rate policy. Those warnings led to sizable US dollar gains against emerging market and G-10 currencies, year-to-date. (except the Swiss franc, which is almost unchanged).

The FOMC action merely validated the actions of those who bought US dollars this year. The lack of dramatic currency swings, post-FOMC, indicates that the current levels adequately priced the rate hike.

Chart US dollar change vs. G-10 currencies year to date 17Dec15

Source: IFXA ltd

That assessment changed on Thursday morning. Even though the reaction to Wednesday’s FOMC action was understated there is a growing consensus that the statement and the economic projections have a modestly hawkish bias. Ms. Yellen was fairly upbeat about the strength of the economy and wasn’t at all troubled by the low oil prices. Ms. Yellen has managed to persuade all the voters to her way of thinking as well. The vote was unanimous.

The Federal Reserve’s bullish expectations for an expanding US economy and forecast of four additional rate hikes in 2016 is in sharp contrast to the Bank of Canada’s(BoC) outlook for the Canadian economy. And that doesn’t bode well for the Canadian dollar.

The BoC recently downgraded their GDP forecast for 2016 and 2017 and similar to last year, projects the economic rebound to occur in the latter part of the year. If so, that means an ugly Q1. They expect weaker business investment and the “complex adjustments to the decline in Canada’s terms of trade” to be weaker in the “near term”.

The outlook for oil prices took a turn for the worse when the US announced an end to the ban on oil exports. The world is already awash in oil and Opec can’t be thrilled with another nation trying to gain market share. The Oil Wars have begun and the Loonie bears awakened.

The US news helped WTI prices to decline to $34.76 which were also undercut by news of another build in US inventories. It will get really nasty if the 2008/2009 support in the $32.60-90 zone gives way. That sets the stage for a plunge to $24.70 a level last seen in 2003.

But that price masks another reality. Nearly one-third of Canadian oil exports are Western Canada Select. WCS is trading at a $13.70 discount to WTI which means Canada is already selling oil at $21.00/barrel. That discount was not all that problematic for Canadian producers and the government when WTI was at $100/b but now it is leaving a mark. You will recall that the BoC cut rates last January in response to falling oil prices. You can’t rule out a repeat of that scenario.

Chart Crude oil prices for various grades on December 14, 2015

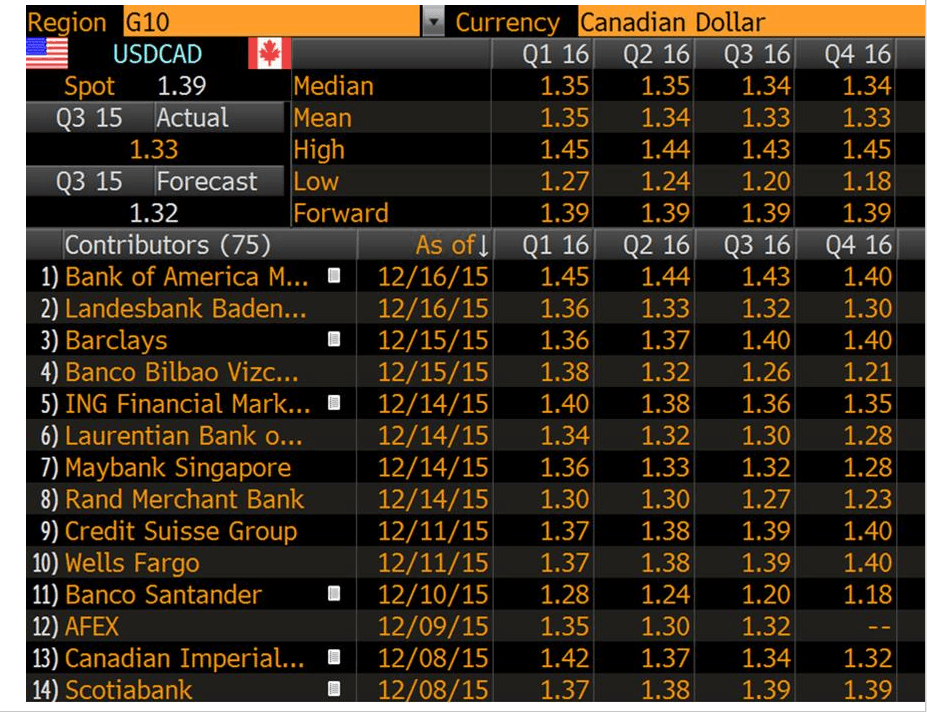

This week’s US dollar rally decimated USDCAD forecasts. Bloomberg surveyed 75 contributors. The mean forecast was 1.3500 for Q1 2016 and 1.3400 for Q2. USDCAD traded at 1.3980 today which is a long way from the mean.

All that proves is that Alan Greenspan, former Chairman of the US Federal Reserve was right. He said that despite having access to reams and reams of data and access to great analytical minds, the Fed concluded that FX forecasting results weren’t much better than flipping a coin.

However, it should be noted that the Q3 2015 forecast, as seen in the top left side of the following chart, was pretty close.

Chart USDCAD forecasts

Source: Bloomberg

The short and medium term USDCAD technicals are bullish. The break of resistance at 1.3465 was also the 61.8% Fibonacci retracement level of the entire 2002-2007 range. That sets the stage for a probe of the 76.4% retracement level at 1.4500.

It won’t be a straight shot. USDCAD will run into significant resistance in the 1.4000-1.4060 area representing previous tops and bottoms. In addition, 1.4000 is a psychologically important trading level and will attract selling interest. The steepness of the rally above 1.3460 to 1.3980 provides ample room for consolidation while leaving the uptrend intact.

The continuing fall in oil prices will take a toll on Canadian investment, employment, consumer confidence, exports, and inflation. That isn’t news. Those issues occurred in 2015 and are the reason why USDCAD sits where it sits. The problem is that their impacts were expected to diminish. So far, there is little evidence of that occurring.

Last week, The Bank of Canada governor, Stephen Poloz went to great lengths to describe the Bank’s unconventional monetary policy tool kit. The fact that he felt the need to talk about the action that the BOC would take if the economy didn’t unfold the way they expected it to, may have been a deliberately subtle way of “talking down the currency”. He did mention that one tool was “forward guidance”.

The prospects for the Canadian dollar in the first quarter of 2016 are grim. Rising US interest rates, lagging Canadian rates, sluggish Canadian economic growth, additional fall-out from falling oil prices and possible speculation of Bank of Canada stimulus action may drive USDCAD to 1.4500 by March.

By David Marks , Agility FX analyst