By Michael O’Neill

The Merriam-Webster dictionary defines “squabble” as a noisy altercation or quarrel usually over petty matters. The squabble avatar looks like President Trump. China and the US are embroiled in a squabble that had its beginnings during the presidential election campaign.

The squabble has evolved into a full-blown war. It is over 397 days since the United States and China traded 25% tariffs on $34 billion worth of each country’s imports. Since then there have been ten rounds of negotiations, including mid-level talks, phone calls and high-level meetings. Even with talks on-going, President Trump kept slapping on tariffs, and China kept retaliating. As of August 7, 2019, the US has levied $250 billion of tariffs applied exclusively to Chinese goods. Retaliatory Chinese tariffs applied exclusively to American goods total $110 billion.

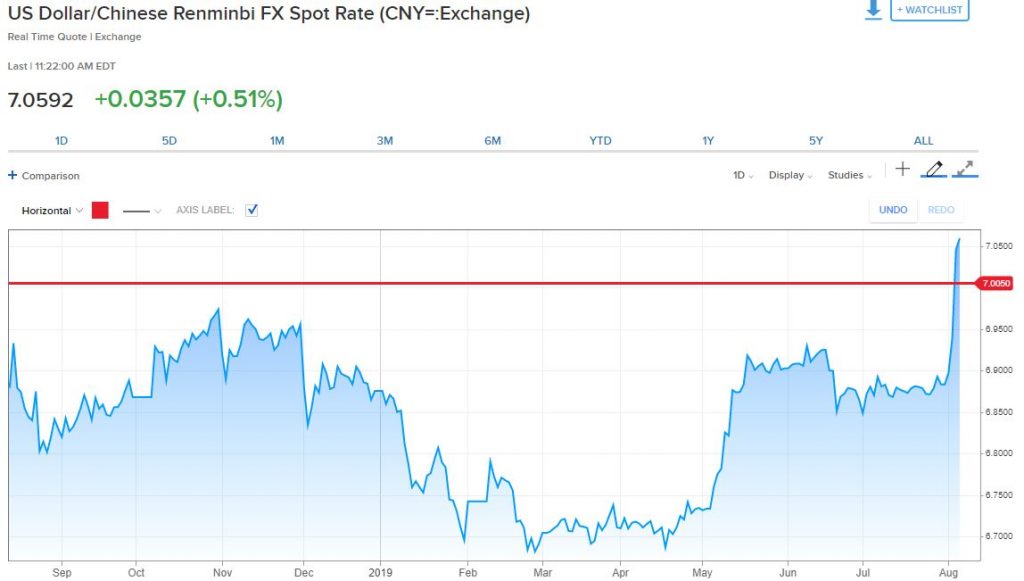

The trade dispute escalated at the beginning of the week. Chinese currency movements turned it into a war. The Peoples Bank of China (PBoC) carefully control their benchmark currency. (USDCNY) They value it against a trade-weighted basket of currencies, allowing it to fluctuate in a 2% range during a fifteen-hour period. USDCNY had not been above 7.00 since June 2008 so when prices touched 7.0300 early Monday morning, the American’s were outraged.

Ssource: CNBC

President Trump tweeted “currency manipulation and the same day, the US Department of the Treasury designated China a “Currency Manipulator.” The press release said, “Under Section 3004 of the Act, the Secretary must “consider whether countries manipulate the rate of exchange between their currency and the United States dollar for purposes of preventing effective balance of payments adjustments or gaining unfair competitive advantage in international trade.” Secretary Mnuchin, under the auspices of President Trump, has today determined that China is a Currency Manipulator.”

It smells like a pre-planned ploy. Mr Mnuchin set the stage for the determination in the May “Macroeconomic and Foreign Exchange Policies of Major Trading Partners of the United States” report. That report noted that the Chinese Renminbi (RMB) depreciated 3.8% in the second half of 2018. It also concluded, “Treasury determines that while China does not meet the standards identified in Section 3004 of the 1988 Act at this time, Treasury will carefully monitor and review this determination over the following 6-month period in light of the exceptionally large and growing bilateral trade imbalance between China and the United States and China’s history of facilitating an undervalued currency.” In a nutshell, Section 3004 of the 1988 act and its partner, the “Trade Facilitation and Trade Enforcement Act of 2015,” means that twice a year the Treasury Secretary evaluates trading partners with over $40 billion of bilateral trade, against three specific criteria, to determine if further action is warranted.

The next review is supposed to be over a six-month period. Barely two-months had elapsed before the currency manipulator tag was applied. It seems a tad premature and unfair, especially when you consider the major G-10 currency moves.

The trade war began on July 5, 2018, when both sides exchanged identical tariff amounts on imports. Since then, the Chinese yuan (Renminbi) has lost 5.4% of its value, as at the New York open on August 7, 2019. The currency that devalued the most was the Australian dollar. It dropped 8.78%, a more significant move than even the British pound which is dealing with the peril around a “no-deal” Brexit. The Euro dropped 4.3% while the Canadian dollar is only down 1.04%. If China is manipulating its currency, it isn’t doing a very good job,

Chart: Change in Percentage Currency value against the US dollar-July18/Aug19

Source: IFXA/Saxo Bank

Australia doesn’t figure into the US Treasury currency manipulation equation because it is below the three thresholds for action. However, if any single country is blatantly devaluing its currency to gain a competitive advantage, Australia fits the bill. China is Australia’s largest trading partner, taking 29.2% of its exports. If a cheaper currency is needed to protect those exports, why not? Of course, that is not how the Reserve Bank of Australia (RBA) justified cutting the overnight cash rate (OCR) twice, from 1.5% in May to 1.00% on July 3. They said the move was needed to shore up soft housing markets and jumpstart subdued inflation while acknowledging record employment levels. Those same conditions were in place at the August 6 meeting, but rates were left unchanged. The common denominator in the monetary policy statements from June, July and August was “uncertainty around trade and technology disputes.” Canada is in the same boat as Australia, yet Canadian rates have been unchanged since they were hiked to 1.75% on October 24, 2018.

If Australia, New Zealand, the Eurozone, Switzerland, and the Fed are cutting or thinking about cutting interest rates, can the Bank of Canada be far behind? That’s what some analysts and Canadian dollar traders are thinking. USDCAD broke above key resistance levels this week and opened the door to a retest of the 2019 peak of 1.3655.

Once upon a time, trade negotiations were mostly boring, bureaucratic backroom discussions which only became front page news on the cusp of a deal. The Trump White House (Squabblewood) changed all that.