By Michael O’Neill

“The dots should be taken with a big grain of salt.” That’s what Fed Chair Jerome Powell said during his June 16 press conference when asked about the two rate hikes in 2023 that were forecast in the Summary of Economic Projections (SEP).

Unfortunately, large grains of salt were in short supply in financial markets.

FX, bond, and commodity prices churned and burned following the release of the FOMC meeting statement and during Mr Powell’s press conference after the Federal Open Market Committee (FOMC), increased the number of interest rate hikes they expected in 2023. The US dollar soared across the board, Wall Street stocks plunged, and gold lost its glitter.

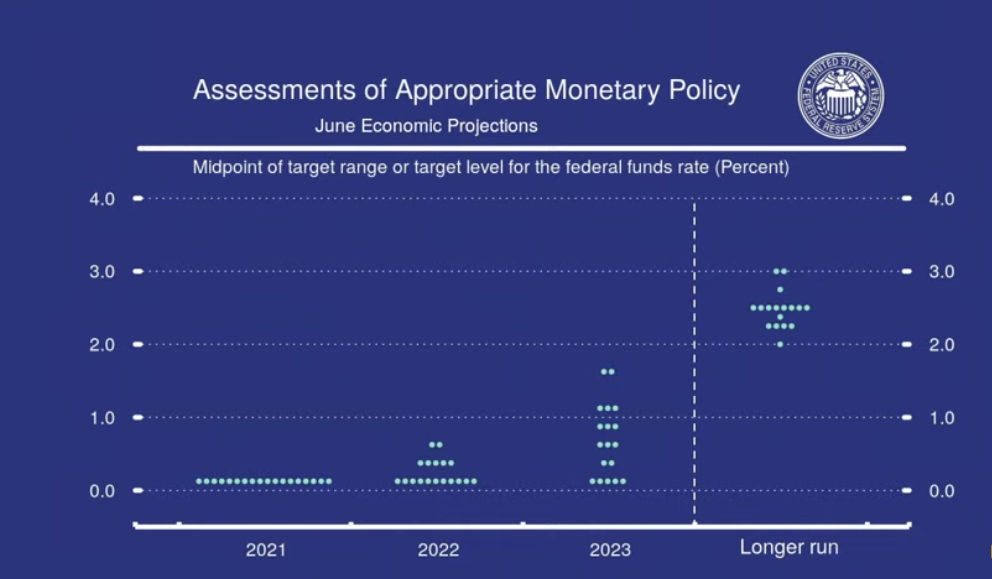

Source: FOMC/CNBC

The medium forecast of two rate hikes in 2023 is a hawkish shift as there were zero hikes predicted in the March SEP. However, Mr Powell dismisses the dot-plot projections saying, “in terms of the two hikes, 1) “they are individual projections.” 2) “they are not a Committee forecast.” 3) “They are not a plan.” And we never actually had a discussion of whether liftoff is appropriated any particular year, because liftoff now would be highly premature. It wouldn’t make any sense”

He goes on to say that the dots are not a great forecaster of future rate moves just because it is highly uncertain.

Obviously, he thinks they are pretty useless, hence the grain of salt comment.

Prior to the meeting, traders were concerned as to whether tapering quantitative easing(QE) purchases would be discussed.

It was, and it wasn’t.

Mr Powell responded to a question about the timing of tapering saying “we will say more about tapering when we see more data. You can think of this meeting that we had as the “talking about talking about” meeting if you like.”

The FOMC statement had a few tweaks compared to the April 28 statement, but if anything, those tweaks made it more dovish.

The Fed added “progress on vaccinations has reduced the spread of COVID-19 in the US” as part of the unchanged assessment of the US economy paragraph.

But they followed with “Progress on vaccinations will likely continue to reduce the effects of the public health crisis on the economy, but risks to the economic outlook remain.”

The Statement rationalized the decision to leave rates unchanged by adding the following, “and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.”

So, in summary, the Fed left the FOMC virtually unchanged and adjusted the dot-plot, which the Fed Chair believes is useless.

Traders reacted to the change in the dot-plots as if the Fed had pre-announced two rate hikes. They blissfully ignored Mr Powell’s comments about employment.

He said “The unemployment rate remained elevated in May at 5.8 percent, and this figure understates the shortfall in employment, particularly as participation in the labor market has not moved up from the low rates that have prevailed for most of the past year.”

Powell pushed back against fears of rising inflation saying that many price increases were due to a spending rebound from the economy reopening and supply bottleneck, which are transitory. He also noted growth risks as “the pace of vaccinations has slowed, and new strains of the virus remain a risk.”

The Fed will not raise rates until it fulfils its mandate which will require “substantial further progress” and Mr Powell repeated that “substantial further progress is a long ways off.”

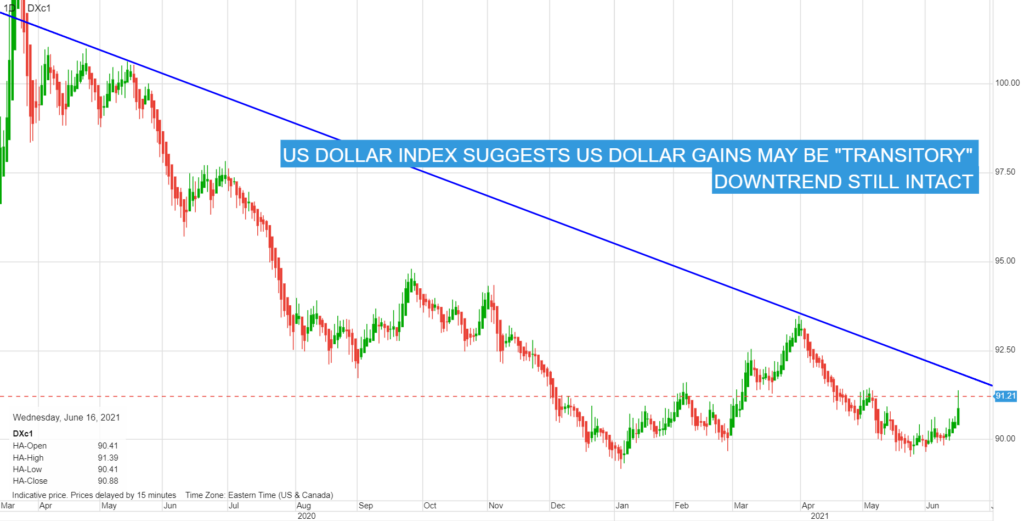

Is the market reaction to the revised dot-plot forecasts a sign the era of easy money is over? Probably not.

Often times, the first reaction to a major central bank event is the wrong reaction. That may be the case this time, as well, if the US dollar index (USDX) is a guide.

The USDX is a measure of the value of the greenback to a weighted basket of currencies that represent the major trading partners of America. Those currencies are Euro, Japanese Yen, Swiss Franc, Canadian dollar, British pound, and Swedish Krona. The USDX rallied following the FOMC meeting, but the gains stalled below the long term resistance at 92.00, a level guarded a double top at 91.50. While prices remain below those levels, the USDX downtrend is intact.

If the dot-plot is not worth squat, as Fed Chair Powell believes, the post-FOMC FX reaction is also not worth squat.

Chart: USDX 1 year

Source: Saxo Bank