Photo: VectorPortal.

By Michael O’Neill

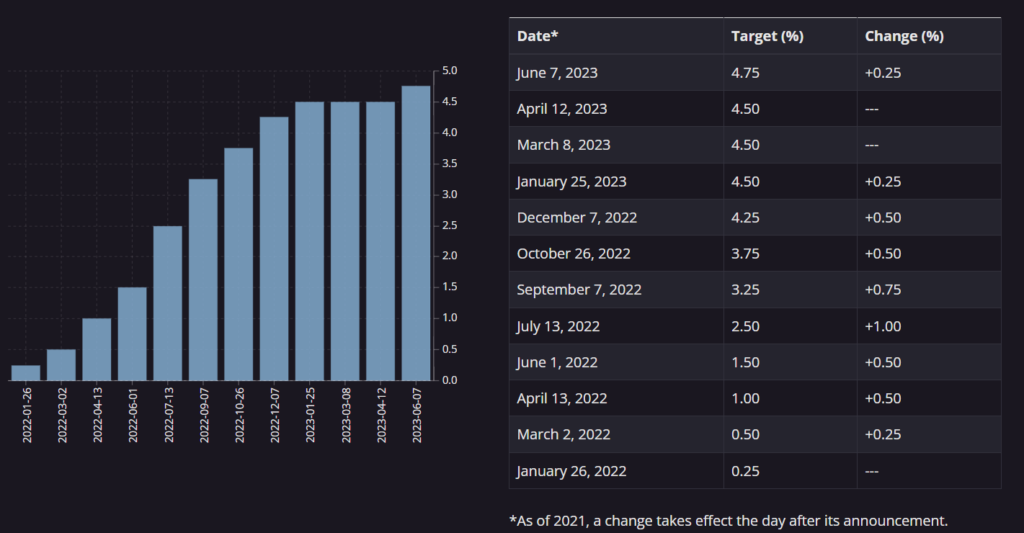

The Bank of Canada faced a significant dilemma on June 7: whether to raise interest rates by 25 basis points or keep them unchanged. Ultimately, they decided to hike, bringing the benchmark overnight rate to 4.75%.

The unexpected news caught many market participants by surprise, as they believed Governor Tiff Macklem had a solid understanding of the factors influencing inflation and economic growth, both domestically and globally. However, the available evidence suggests otherwise.

On January 25, Mr. Macklem announced the Bank of Canada’s plan to maintain policy rates at 4.5% “while assessing the impact of cumulative interest rate increases.” He emphasized that the bank’s ongoing quantitative tightening program complemented the restrictive stance of monetary policy. However, it seems that the relationship between quantitative tightening and monetary policy has not played out as expected.

In February, Mr. Macklem delivered a comprehensive explanation to a Quebec audience regarding how monetary policy works in controlling inflation. He emphasized that the Bank is an inflation-targeting central bank with a 2.0% inflation target, which it had consistently maintained for approximately thirty years before the pandemic.

During the same month, Mr. Macklem observed that “we are beginning to see signs that higher rates are rebalancing the economy.” He pointed to moderating household spending, indications of a loosening labor market, and lower inflation levels as evidence. He also noted that the policy rate’s impact on inflation is indirect and may take up to two years to fully materialize.

Bank of Canada rate hikes since January 2022

Source: Bank of Canada

Tiff Macklem has embraced forward guidance as a favored monetary policy tool. He and his team maintain an active Twitter account with 231,000 followers to reach a wider audience and explain monetary policy and decisions.

In theory, it’s a great idea. Frequent communication from policymakers provides transparency and clarity, helping manage market expectations and enabling households and businesses to make better-informed decisions while anchoring inflation expectations.

Unfortunately, the Bank of Canada’s forward guidance has been a failure. Mr. Macklem has made several policy communication missteps. In 2020, he advised Canadians to take on debt because rates would remain low for a long time. However, he was late to recognize that inflation was becoming more than just transitory. He also advised private sector employers not to incorporate inflation into long-term employee contracts, while neglecting to address the 14% wage increase given to public sector employees. Furthermore, he and other Bank of Canada officials have repeatedly stated that they do not react to every data point before proclaiming that rate hikes will be data-dependent.

The Bank of Canada’s forward guidance tool should be discarded in an environmentally-friendly, biodegradable manner.

The rate hike by the Bank of Canada briefly impacted USDCAD, pushing it down from 1.3380 to 1.3323. However, attention quickly shifted to events in the United States and the outlook for the June 14 FOMC meeting.

US Treasury yields surged, with the 10-year yield rising from 3.60% on June 6 to 3.80% on June 8 due to the fallout from the debt ceiling issues. Analysts at JPMorgan Chase estimate that approximately $850 billion of bond issuance was delayed due to Republican-Democrat gamesmanship.

The rise in yields bolstered the US dollar and weighed on equities.

The upcoming FOMC meeting remains uncertain. Market sentiment fluctuates between expectations of a rate hike or a pause in July, or a pause followed by a hike. However, stubbornly high inflation, a tight labor market, and stronger-than-expected economic growth indicate a hawkish bias with reduced chances of a rate cut in 2023.

Geopolitical tensions are escalating, but dire headlines about near misses, missile tests, drone strikes, and counter-offensives rarely have a significant impact on financial markets.

China’s Defense Minister refused to meet with his US counterpart, while Chinese warships engage in provocative encounters with US destroyers in the South China Sea, and Chinese fighter jets buzz a US spy plane.

European Union Foreign Affairs Minister Josep Borrel suggested deploying member country warships to patrol the Taiwan Strait.

Russia’s invasion of Ukraine has stalled. Ukraine might retaliate for drone attacks on residential areas of Kyiv by using similar weapons against Russian intelligence officers in residential areas of Moscow. Russia reportedly possesses 5,889 nuclear warheads, and even if half of them don’t work, it is a devastating arsenal. Things can escalate rapidly.

Former US President Harry Truman advised school children to “duck and cover” in the event of a Russian nuclear attack, an idea as flawed as the Bank of Canada’s forward guidance policy.