The oil bears are out of hibernation. And they are hungry. Unfortunately for them, a flock of Canadian rate-hike hawks have been eating their lunch.

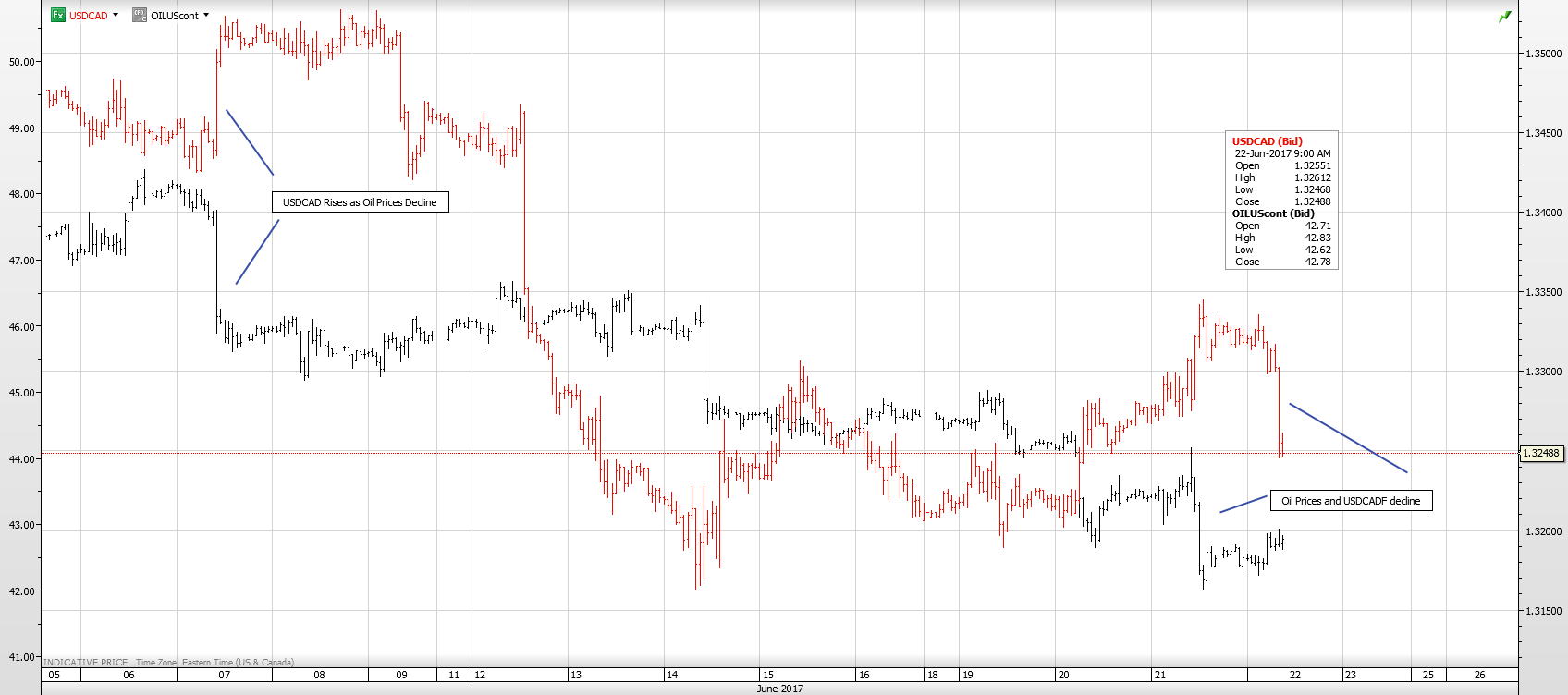

West Texas Intermediate (WTI) oil prices rallied from April through May They peaked at $51.92/barrel on May 22 after rising from $43.76/b when Opec announced a nine-month extension to production cuts. One month later, those gains are gone.

In the same period USDCAD climbed from 1.3220 to 1.3790 and then retraced the entire move by June 13.

That is not the “normal” Canadian dollar/oil relationship. A 19 percent decline in oil prices rarely translates into a 4.7 cent gain in the Canadian dollar against its US counterpart.

The Organisation of Petroleum Exporting countries (Opec) wrote in their June 13 Monthly Oil Market Report that global oil demand would pick up in the second half of 2017 projecting a 2 million barrel /day increase in total consumption.

They also expect that the overhang in OECD commercial oil inventories will continue in the 2nd half of 2017 supported by Opec production cuts.

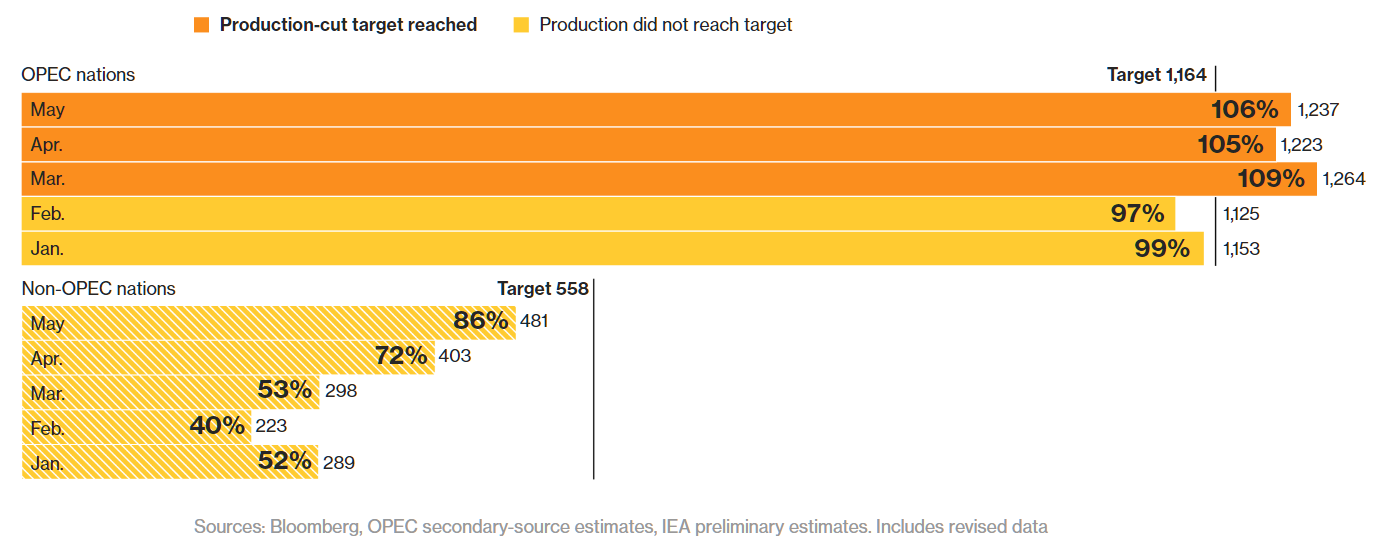

Opec extended production cuts that began in January 2017 for another nine months beyond June 2017. According to Bloomberg on June 19, OPEC members are close to achieving their 1.8 million b/d reduction target.

That is a reasonably positive outlook for crude prices.

However, the recent price action implies that oil traders don’t see it that way.

There are several reasons for why that is the case. For starters, the upbeat Opec outlook and the production cuts were already factored into the prices. WTI had rallied from $43.80 to $51.95 on anticipation of not just a production cut extension but deeper production cuts as well.

Furthermore, US production and high inventories were a major concern. The Energy Information Administration (EIA) weekly crude stock report on June 21 said “At 509.1 million barrels, U.S. crude oil inventories are in the upper half of the average range for this time of year.”

A near-doubling of US oil-directed drilling rigs has led to rapid US crude production which is weighing on prices.

The EIA expects US crude production to increase steadily through 2018, noting the US is the largest contributor to the 820,000 b/d of non-Opec liquids supply growth from January to May 2017.

At the same time, Libya and Nigeria have been ramping up production.

Lastly, WTI oil price technicals are bearish while trading below $44.30 and looking for a break of support in the $41.90-$42.10 level to extend losses to $39.10

Yet, despite the oil price drop and the bearish short term outlook for prices, the Canadian dollar rallied.

That’s because of the Bank of Canada metamorphosis. The doves became hawks.

BoC Governor Stephen Poloz was getting quite the reputation as a “Gloomy Gus,” especially during policy press conference. He had a penchant for focusing on perceived risks to the economy while downplaying positive data. In January, he was saying “rate cuts were on the table”. In March, he was hyping “looming uncertainties” as he was concerned about rising US protectionist trade policies. The Bank of Canada’s negative outlook was occurring despite better than expected economic data.

The tone started changing in April. The possibility of a rate cut was gone.

The metamorphosis was completed in June and in a surprising fashion. The doves became hawks and they didn’t wait for a policy meeting press conference to emerge.

Instead, a newly hawkish Deputy Governor Carolyn Wilkins was unveiled in Winnipeg on June 12. She used a speech titled “Canadian Economic Update: Strength in Diversity” to give an economic driving lesson when she announced it was time “to let up on the gas” in reference to monetary policy stimulus.

Steadily improving domestic economic data and a conclusion that the adjustment by the Canadian economy to the “oil price shock” had run its course. The curtain was getting ready to fall on the era of “easy money.” That was what traders concluded after a speech by Deputy Governor Carolyn Wilkins on June 12. Her remarks were endorsed by the governor the following day.

Governor Poloz endorsed her view the next day when he announced “rate cuts have largely done their work”.

The policy “about-face” sent the Loonie soaring.

The Bank of Canada policy shift got an added dose of support from the June 22 Retail Sales report. March retail sales far exceeded forecasts and the gains were across 9 out of 11 subsectors.

The oil bears may be hungry and looking for a further drop in WTI prices, but the newly minted interest rate hawks at the Bank of Canada have flown to the front of the buffet table.