By Michael O’Neill

The Canadian dollar is sailing into 2024 under cloudy skies and rough seas but there is some sunshine on the distant horizon. However, its direction is still a US dollar story, with Admiral Jay Powell commanding the G-10 currency fleet, and USDCAD is merely a leaky frigate along for the ride. This forecast integrates insights from FX predictions by leading banks in Canada and in Europe while also accounting for anticipated trends in CPI, Canadian GDP, the Bank of Canada overnight rate, and Federal funds.

Executive summary:

- USDCAD range is 1.2700-1.4500 for the year, peaking in H1, then falling until year-end.

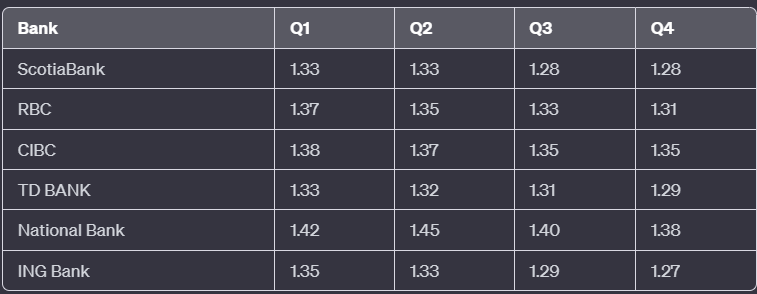

- The median rates are: Q1 1.3600, Q2 1.3400, Q3 1.3200, and Q4 1.3000.

- The key drivers for USDCAD will be the timing and magnitude of US interest rate cuts, global economic factors, and Bank of Canada monetary policy action (or inaction).

- Geopolitical tensions will continue to be the dark-colored swan, as will Donald Trump’s many prosecutions and its impact on his Republican nomination. Later in the year, the focus will be squarely on the US election.

- The Bank of Japan could surprise markets with a more aggressive monetary policy tightening, and the ensuing demand for yen could derail G-10 currencies.

Source: data form BNS, BMO CIBC, National Bank, ING

Bullish USDCAD Factors

- Early Year Momentum: The year has started with a somewhat bullish undertone, with the short-term technicals showing a mild uptrend above 1.3340, supported by the consensus forecast of 1.3600 for Q1.

- Macroeconomic Optimism: With the US economy showing resilience, particularly in employment and consumer spending sectors, alongside somewhat sticky US inflation data for December, a is suggests ongoing demand for US dollars.

- Elevated Geopolitical Tensions: The US and Britain have launched attacks on Houthi targets in Yemen. The Houthis responded by declaring British and American assets legitimate targets. Russia has stepped up attacks on civilian targets in Ukraine and North Korean President Kim Jong-Un has missile envy.

- Oil Prices: West Texas Intermediate (WTI) cannot gain traction despite Middle East tensions threatening to disrupt supply, and OPEC production cuts. WTI remains below the 50-day, 100-day, and 200-day moving averages, which is limiting gains, and the soft prices underpin USDCAD.

Bearish Factors

- Mid to Late Year Reversal: The landscape shifts as we progress into Q2 and beyond. The consensus forecast dips below the moving averages, indicating a potential weakening of USDCAD. By Q4, the forecast falls to 1.3200, significantly lower than the 200-day MA, suggesting a bearish outlook.

- Interest Rate Differentials: The Bank of Canada’s (BoC) rate forecasts, contrasted with the Fed Funds outlook, suggest a narrowing interest rate differential. This will diminish the USD’s yield advantage, thereby applying downward pressure on the USDCAD.

- Commodity Prices: Oil prices are expected to rise toward $85.00/b in 2024 and could easily top that level if the conflict between Israel and Hamas expands to include other Middle Eastern countries. An uptick in the global commodity market could bolster the demand for Canadian crude and other resources, contributing to the bearish sentiment for the USDCAD.

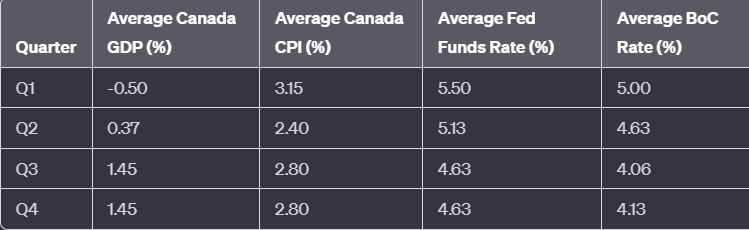

Chart: Macroeconomic forecasts imbedded in the USDCAD outlook.

The forecasts are the averages estimates from Canadian, US and a European bank.

Source: various Canadian, and European banks

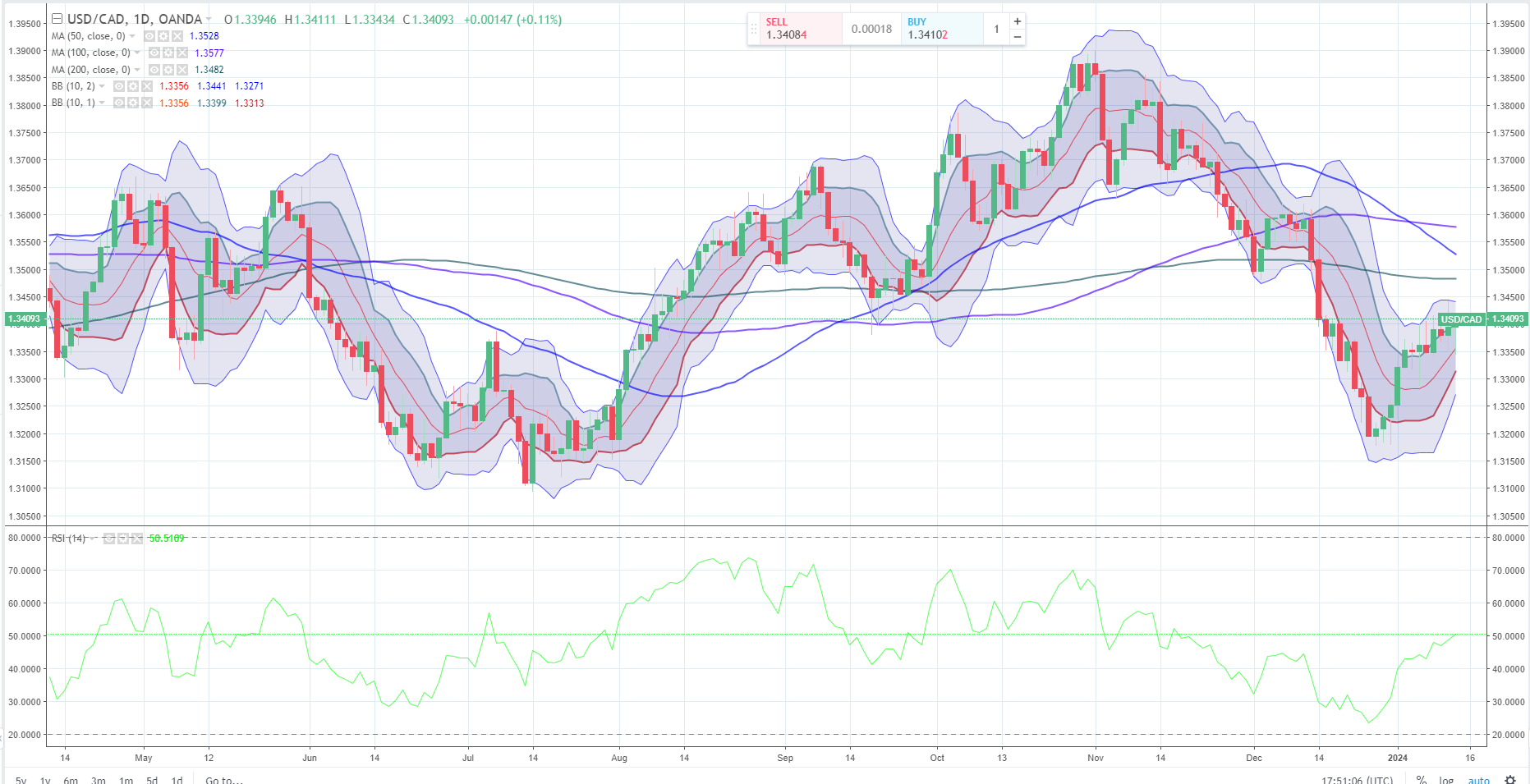

The USDCAD technicals are murky. The Bollinger band show USDCAD above support with room to rise to test the upper range. However, it remains below the 50 day, 100 day and 200 day moving averages which suggest a negative bias.

USDCAD Chart Analysis -1 year

Conclusion and Direction

The consensus forecast for USDCAD in 2024 seems to be initially bullish but shifts to bearish as the year progresses. However, the forecast does not jibe with the current technical picture, which is bearish. Technicals aside, the early year strength of the USD is driven by solid economic fundamentals. The latest inflation data supports a Fed content to leave rates in restrictive territory for longer than anticipated, which will support the US dollar. The modest narrowing of CAD/US interest differentials may be temporary if the Bank of Canada is forced to cut rates ahead of the Fed. That’s because the Canadian economy is sharply weaker than the US, and the current interest rate risks sparking a mortgage crisis. The federal government is free-falling in the polls, and they wouldn’t want the BoC to exacerbate the issue.

The reality remains that USDCAD direction is almost entirely dictated by the Fed and developments south of the border. This year has a major wild card as it includes another Trump/Biden confrontation, assuming one is still alive, and the other isn’t incarcerated.

When considering the veracity of this USDCAD outlook, consider that forecasting the Loonie is like a badly confused sailor attempting to navigate the seas with a protractor rather than a compass.