By Michael O’Neill

Analysts forecasting US and Canadian interest rate direction for 2024 may have mistaken ice cubes in a heavily-spiked punch for leaves in a teapot. How else would you explain predictions of 150 and 75 basis interest rate cuts from the Fed and Bank of Canada, respectively?

It is even more perplexing when you consider Fed Chair Jerome Powell’s warning during the December 13 FOMC press conference that “We are prepared to tighten policy further if appropriate.” Bank of Canada Governor Tiff Macklem didn’t sound all that eager to cut rates when he said, “Until we see evidence that we are clearly on a path back to 2% inflation, I expect the Governing Council will continue to debate whether monetary policy is restrictive enough and how long it needs to remain restrictive to restore price stability.”

Those comments do not sound like people highly motivated to lower interest rates.

Even so, a whole lot of really smart people are betting that the US and Canadian rate hike cycle is over. Traders on the Montreal Exchange have assigned a 100% probability that the BoC cuts rates by 25 bps on March 6, again on June 5, and once more on December 11.

US traders are much more aggressive. They expect the Fed to chop rates six times, beginning in March, taking the Fed funds rate from 5.50% to 4.00% by December.

The minutes from the December 13 Federal Open Market Committee meeting suggest traders need to “give their heads a shake.”

Sure, the minutes clearly say that “Participants viewed the policy rate as likely at or near its peak for this tightening cycle.” And the minutes also noted that “participants indicated that based on improvements in their inflation outlooks, their baseline projections implied a lower target range for Fed funds would be appropriate by the end of 2024.”

There is no doubt that the Committee expects to lower rates in 2024, but anticipating a 25 bp cut at six out of the next seven meetings is a bit of a stretch.

It’s even more of a stretch when you consider the following:

- Continued Inflation Concerns: Despite acknowledging the easing of inflation, the Committee remains focused on inflation being above their 2 percent target, indicating an ongoing concern about price stability.

- Restrictive Monetary Policy Stance: The FOMC’s commitment to maintaining a restrictive monetary policy until inflation consistently moves towards their goal shows a priority for curbing inflation over stimulating growth.

- Uncertainty about Economic Outlook: The minutes reflect uncertainty about the economic outlook, suggesting caution and a readiness to continue with a tighter policy if needed.

- Labor Market Rebalancing: Emphasis on the rebalancing of the labor market, with expectations of a rising unemployment rate, aligns with a hawkish stance focused on cooling the economy.

- Future Policy Adjustments: The readiness to adjust policy as necessary, based on incoming data, indicates a focus on inflation control.

These elements suggest the minutes were hawkish and certainly do not justify 150 bps of easing in 2024.

Analysts expect that the Bank of Canada will follow the Fed’s lead and, if the Montreal Exchange rate cut probabilities are correct, could be the first off the mark with a move two weeks earlier than the Fed. That’s because not only is Canadian economic growth stalling, but the country may also be already experiencing a recession, and the unemployment rate has climbed steadily since April.

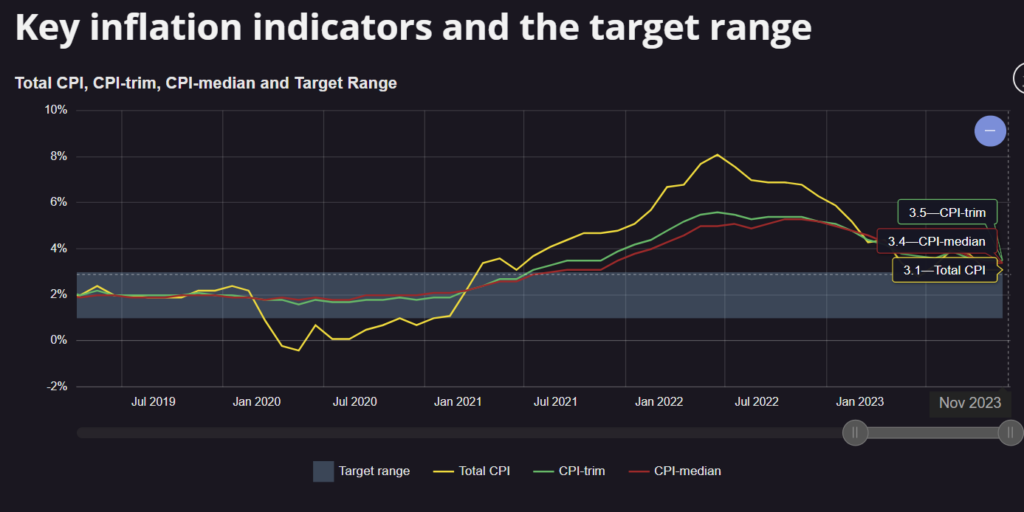

Governor Macklem didn’t sound too thrilled about the outlook for inflation. In his December 14 speech, he expressed concern about food inflation being around 5.5%, non-core inflation being sticky in the 4.5% area, and shelter services cost at nearly 7.0%. Then, five days later, the November Core inflation results showed the rate remained at 3.5%. The BoC’s mandated target is 2.0%, and the latest data proves the inflation fight is far from over.

The start of a new year brings plenty of optimism. After all, if your books work on a calendar year, you probably haven’t lost any money. (yet) There is nothing but upside. But not this year.

Arguably, the big moves have already occurred since the Fed pivot on December 13. Stocks soared, and the US dollar tumbled. Bond traders led the way, driving the US 10-year Treasury yield down from 4.95% in the middle of October to 3.80% on Boxing Day.

The problem isn’t just that the moves are excessive, but they totally ignore the rapidly rising geopolitical risks.

The Middle East is starting to burn. A Hamas leader suffered missile-stroke in a camp in Lebanon. Meanwhile, in Iran, an unexplained explosion near the tomb of the late General Qasem Soleimani, who is recognized as a sponsor of terrorism, caused significant casualties among those gathered to commemorate him. The US Navy is leading a group of nations including the UK and Norway in protecting Red Sea shipping from Houthi terrorists.

Russia has ramped up missile and drone attacks on civilian targets throughout Ukraine, and North Korea continues to fire missiles into the Sea of Japan. China’s economy is slowing, and youth unemployment has risen so sharply, the government no longer provides the fake statistics it used to. Wars have traditionally managed to boost employment (military draft), and Taiwan makes an inviting target, especially as the US is distracted with the 2024 election.

Analysts predicting US and Canadian interest rates for 2024 might be mistaking wishful thinking for reality. Their forecasts of significant cuts by the Fed and Bank of Canada may be as misguided as seeing shapes in ice cubes rather than tea leaves.