By Michael O’Neill

Canadian dollar traders are singing “Clowns to the left of me, jokers to the right, and here I am stuck in the middle with you. Most of them never heard of Stealers Wheel, a Scottish folk-rock band that had their fifteen minutes of fame forty-seven years ago. The clowns and jokers could be references to Trudeau and Trump but “stuck in the middle” is where the Loonie sits, after nearly four months of trading.

Coincidently, (or maybe not) EURUSD and AUDUSD are suffering a similar fate to the Loonie. Both those currency pairs are bouncing around the middle of their mid-July-mid-November trading ranges.

Traders have fixated on a host of issues. US recession fears, the Fed’s monetary policy outlook, and anticipating European Central Bank’ monetary stimulus plans, took turns driving G-10 major currency direction. Great Britain’s self-mutilation provided additional trading fuel until the feared apocalypse at the Brexit deadline never materialized. Most of those issues have come and gone, albeit with the odd flare-up. However, the US/China trade war, which began July 6, 2018, continues to be the itch that you just can’t scratch. It is a chronic ailment flummoxing central bankers and their policies, across the globe. And it isn’t going away, or maybe it is. Only the “Tweetmaster” knows for sure.

Chinese and American trade negotiators are doing the “two-step boogie”. It’s a very noisy, yet simple dance, where the partners amidst a background of raising and deferring trade tariffs, shuffle backwards, forwards and side-to-side, without going anywhere.

FX traders are showing signs of fatigue, while equity traders are oblivious to the trade talk issues or any of the other risks overhanging markets.

Wall Street equity indices are posting record highs despite warnings flashing like strobe lights in a 70’s era disco. CNBC reported the S&P is poised to show the third consecutive quarter for negative year-over-year earnings growth, yet the stock markets rise into nosebleed territory. Equity traders are seemingly oblivious to trade disputes and geopolitical frictions.

Fed officials, including Chair Jerome Powell and Vice Chair Richard Clarida, harp about downside risks to the US global growth outlook. These include sluggish global growth and the uncertainty around global trade policy which creates headwinds for manufacturing activity and investment spending. Brexit is another festering sore, and it will be oozing pus until January 31, 2020. Officials are also concerned about slowing growth in China, global disinflation forces and a US recession. No one is listening.

The US bull market is in its eleventh year. It is nearly two years longer than the 1990’s bull market that ended in 2000, with the Nasdaq at 5,048.62 and the Dot-com bubble bursting in 2000. By 2002, the Nasdaq erased 78% of its bull-market gains. Why will this time be different?

If equity traders are living in an “Neverland” where prices always go up, FX traders have booked rooms at the “Heartbreak Hotel.” They jumped into many trade deal love affairs only to have their hearts broken with each set-back or hostile tweet. No longer. The US dollar came under selling pressure on November 7 in Europe, after reports surfaced that Chinese and American negotiators agreed to rollback tariffs. The losses were shallow and fully recouped within a few hours, in part because President Trump didn’t tweet about his agreement to the rollbacks.

Global central bankers are united in the view that the ongoing trade war is hampering their domestic economic growth, exports, and business investment. A US/China trade deal won’t solve their problems. Chinese economic growth has been slowing for the past few years, and the trade war just exacerbated the slowdown. China is trying to transition to a consumer consumption economy from one fueled by debt. China’s Q3 GDP was 6.0%, and economists at the World Bank forecast GDP further slowing to 5.9% in 2020.

If so, it doesn’t bode well for Canada or the Canadian dollar.

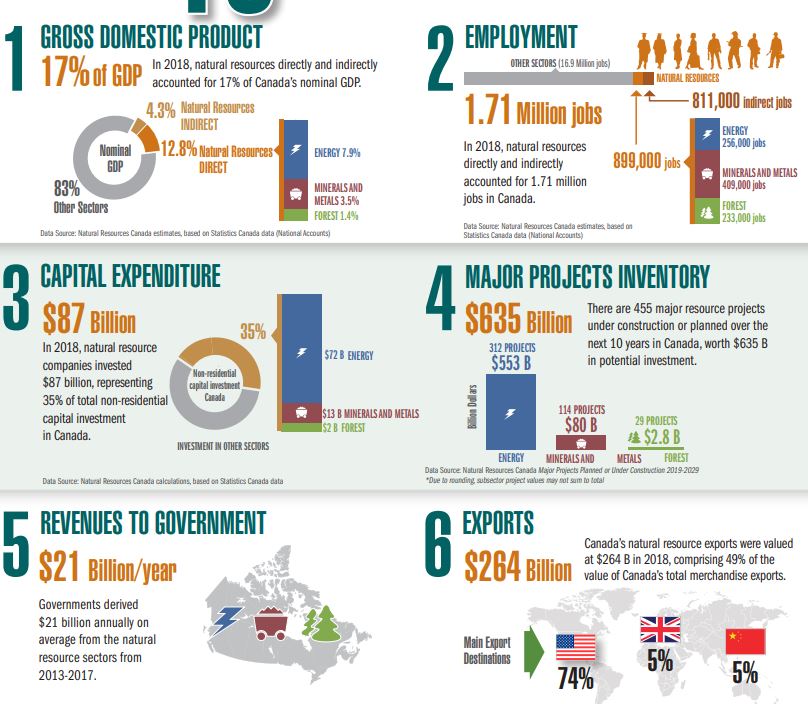

Canada remains a resourced based export economy. In 2018, natural resources, directly and indirectly, accounted for 17% of GDP, $1.71 million jobs, and $21 billion in revenue to the government. Canada’s oil patch is in disarray. Prime Minister Trudeau’s Liberal government has adopted an anti-oil production and pipeline agenda in the guise of being climate change champions, leaving land-locked Alberta, awash in crude but nowhere to send it. The Canadian dollar is already seeing the erosion of traditional support from rising crude prices.

Graph: Importance of natural resources to Canada

Source: Natural Resources Canada

Agriculture and agri-food exports contribute 2.6% to total GDP. China is an important destination for these exports, but Beijing is unhappy with the Canadian government. So unhappy that they banned imports of pork, beef, soybeans, and canola without any ill effects on their economy. President Trump is not only eager to fill the void from the ban, he is insisting China import massive dollar amounts of US agricultural products or tariffs remain. If successful, Canadian farmers will suffer, as will the domestic economy and the Loonie.

The Canadian dollar is the strongest major currency against the US dollar this year, and it has risen against the rest of the G-10 majors as well. Unfortunately, it puts Canadian exporters at a disadvantage to their global competitors. Falling exports could be the “straw that breaks the camel’s back” and force the Bank of Canada to cut interest rates. The Reserve Bank of Australia has already adopted the currency devaluation strategy, with some success.

There is no doubt that the Loonie has clowns to the left, and jokers to the right, but it is unlikely to stay stuck in the middle, for much longer.