By Michael O’Neill

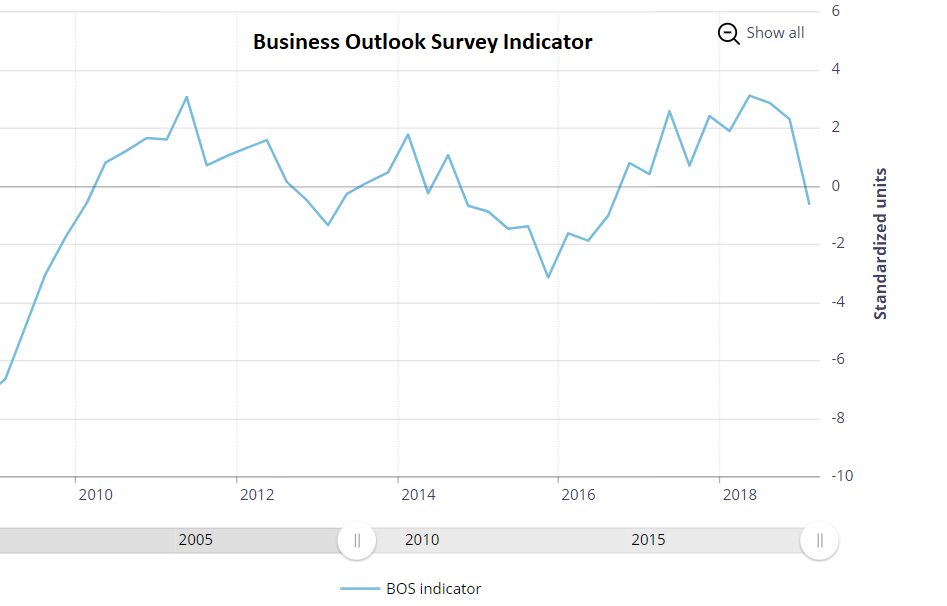

The quarterly Bank of Canada Business Outlook Survey (BOS) said “Bah, humbug.” Well, not quite but its’s conclusions were not warm and fuzzy either. The BOS warned its key indicator flipped, saying it “decreased from a strongly positive level in the winter survey and is now slightly negative, suggesting a softening in business sentiment.” The survey noted “expectations for sales and demand have softened, especially in the prairie provinces, alongside a sharp decrease in capacity pressures.

Source: Bank of Canada Business Outlook Survey

The Canadian dollar sank on the news amidst an avalanche of negative media headlines trumpeting a “drop in business sentiment.” But it wasn’t all bad news. The Survey noted that “sales prospects abroad remain positive, supported by sustained foreign demand.”

Some economists suggest that this BOS means that the Bank of Canada will leave interest rates unchanged for the rest of the year. They point to the big drop in capacity pressures as evidence of a widening “output gap,” a favourite measure for BoC Governor Stephen Poloz. The output gap (a largely unquantifiable value) is defined as the difference between actual and potential output.

Other economists are a little more skeptical of that view. There was a dark cloud hanging over markets during the survey period of February 19 to March 13 which had to weigh on sentiment and therefore their survey responses. At the time, equity markets were still recovering from their December swoon. US/China trade talks were just restarting under the threat of a massive tariff levy by the US slated for March 1, and a series of Canadian economic reports were weaker than expected. Some of the results were sketchy. The BOS said indicators of labour shortages decreased. Scotiabank economists questioned that result because Canada hired 115,000 in the quarter. They do not see how labour shortages could decrease in the face of all that hiring. They also pointed out that the survey sample is tiny-just 100 businesses.

Questionable data isn’t just a Canadian problem. The European Central Bank (ECB) has continuously revised its economic forecasts lower, and that has raised a few eyebrows. Reuters reported that some ECB policymakers were questioning the accuracy of ECB projection models, because of their history of downward revisions. ECB President Mario Draghi attributes the revisions to “downside risk.: Fed Chair Jerome Powell calls them “crosscurrents.” Computer geeks call it GIGO. (garbage in-garbage out)

The geeks may be right. The Fed went from projecting two rate hikes in 2019, just last December, to no rate hikes, at their March 20 meeting. In the past six months, the ECB has pushed rate hikes out from June, to the end of the summer, and then most recently not until the end of 2019. The Bank of Canada raised interest rates October 24 and hinted at two more rate hikes in 2019. By March 6, rate hikes were off the table, and there is some talk that the October hike could be reversed. Those are serious reversals of economic outlooks.

The major central banks have scores of economists and analysts with more degrees than a thermometer, and still, they struggle to get an accurate read on their economies. Why then, should anyone expect that the Business Outlook Survey’s sampling of 100 Canadian CEO’s would produce any better results.

President Trump’s trade war with China is a significant negative to the growth outlook domestically and globally. Most, if not all the G-10 major central banks cite some variation of “trade tensions” for their concerns that economic growth “risks are to the downside.”

Those concerns may disappear in the not-so-distant future. Reportedly, China is ready to start making concessions including removing tariffs on US poultry and pork imports. On April 16, Trump’s National Economic Advisor Larry Kudlow said: “We continue to make very good progress across the board. These are the largest in scope negotiations in U.S. China trade-relations history.” He said that both sides had made noteworthy progress on such issues as enforcement, intellectual property theft and barriers for agriculture and industrial commodities. Another sign that the US/China negotiations are in their final stages is Trump has kicked off trade talks with the European Union.

Central bankers are fretting about downside risks, but Wall Street traders aren’t. The S&P 500, Dow Jones Industrial Average, Nasdaq and TSX are close to all-time highs, fueled by low-interest rates and the prospect that rates will stay low for the rest of this year.

The US/China trade war has hurt domestic economic sentiment. However, BoC Governor Stephen Poloz said back in January, that “if the United States and China were to reach a broad agreement on trade issues, global and Canadian economic activity would be stronger than in the base-case projection.” As well, the near-term upward pressure from tariffs on prices would be removed.

If Mr Poloz is right, the answer to the question “and the survey says” will be “let the good times roll.”