By Michael O’Neill

US Inflation’s mighty roar has been beaten down to a meek squeak and now the spotlight is swinging to the employment outlook. Economists and analysts are biting their nails over fears of a weakening labor market, raising the specter of an economic “hard landing.”

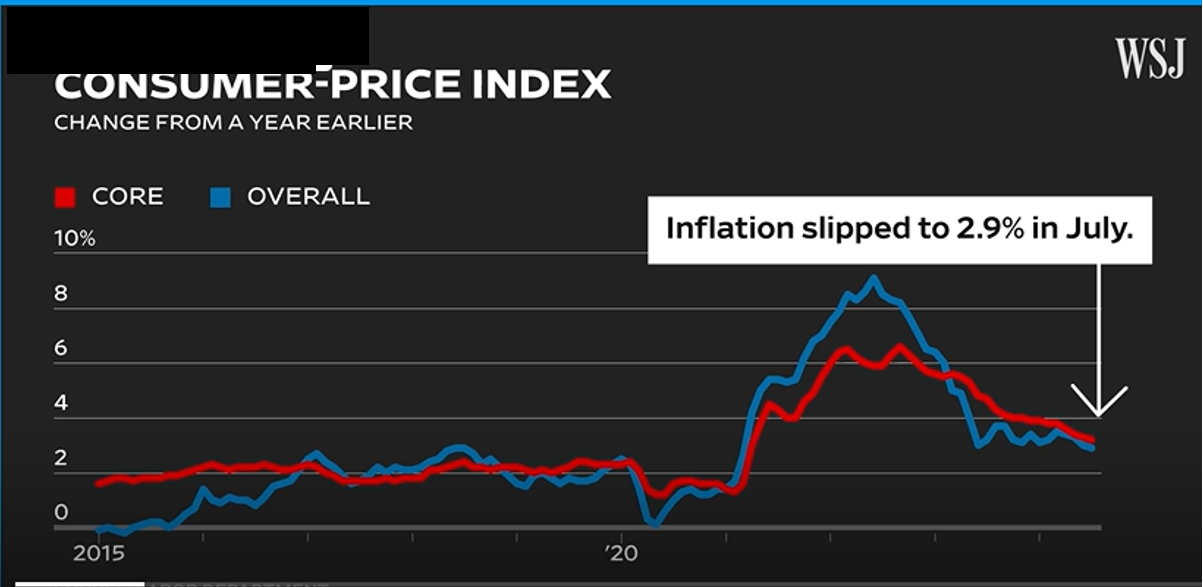

The August 14 inflation report landed almost exactly as expected, sparking cheers from some corners. The 0.2% increase in July CPI marks the third-best monthly reading of 2024, keeping the downward trend on track. Others note that the 2.9% year-over-year increase in July is the lowest since 2021.

Source: Wall Street Journal

Not everyone is celebrating, though. Those living in houses, condos, and apartments might be less inclined to cheer the CPI results, especially since shelter prices climbed faster than in June. But hey, it’s “no big deal,” right? After all, other U.S. rental measures are trending lower. Tell that to those whose disposable incomes are shrinking while they still have to shell out more for food. Who needs Ozempic when you’ve got “Shrinking through Inflation”?

CPI Data Already Out of Date

The August 14 inflation report is mixed enough to provide fodder for any view. But when it comes to the interest rate outlook, it’s about as meaningful as a Snickers bar in a nutrition plan. It’s disposable data—destined to be stale by the time the Federal Open Market Committee meets on September 18. By then, fresher and more critical inputs—like PCE Price Index data, Q2 GDP, and no fewer than five employment reports, including the September 6 nonfarm payrolls—will set the stage for the size and pace of Fed rate cuts.

Don’t Fight The Fed

The 1980s taught financial markets a lesson that still rings true: “Don’t fight the Fed.” Back then, Fed Chair Paul Volcker went full throttle on interest rate hikes to combat inflation. In 1979, with U.S. inflation at around 11.3%, Volcker famously declared, “Inflation is the cruelest tax of all” (carbon taxes were still a gleam in some bureaucrat’s eye). He didn’t just talk the talk—he walked it, announcing, “The American standard of living must decline.” And decline it did. By June 1981, fed funds had reached a staggering 20%. Two years later, CPI had cooled to 3.2%, though it took another 4-5 years for rates to settle back into the 7.0-8.0% range. This was also the era when investors learned the hard way: betting against the Fed was a surefire way to end up on the losing side of trades.

But its Different this Time

Bond traders do not think the warning applies to them or is even applicable today. They have aggressively snapped up bonds, driving the U.S. 10-year Treasury yield down from 4.62% on May 29 to 3.80% on August 14—suggesting they expect at least 75 bps in rate cuts. The June Summary of Economic Projections hinted at just one 25 bps cut by year-end, but when the Treasury yield slide accelerated, the June dot-plot was a distant memory. Nevertheless, a host of Fed speakers continued to downplay rate cut risks. Who is going to be right?

Jackson Hole Lotta Hype

The answer might come around August 22-23, when the who’s who of central banking gather at the Kansas City Fed’s 2024 Jackson Hole Symposium in Wyoming. Central bank bigwigs, including the Bank of Canada’s Tiff Macklem, Bundesbank President Joachim Nagel, ECB President Christine Lagarde, and Bank of England Governor Andrew Bailey, will join Fed Chair Jerome Powell to discuss “Reassessing the Effectiveness and Transmission of Monetary Policy.” It’s a timely topic, considering at least three of these attendees have fumbled inflation management. This annual bun-fest in the Teton Range of the Rocky Mountains has a knack for producing market-moving news—five Fed Chairs have used it to signal policy shifts or outline economic outlooks. For example, Alan Greenspan hinted at rate cuts in 1998, post-Asian Crisis and LTCM collapse. Ben Bernanke laid the groundwork for QE2 in 2010. And most recently, in 2020, Jerome Powell introduced the shift to average inflation targeting, which traders heard as “low rates for longer.”

“Let’s Go To the Ex”

The Canadian National Exhibition opens its doors in Toronto on August 15, continuing a tradition that began in 1879. It’s been running nearly uninterrupted, save for a few timeouts during the world wars (1917-18, 1942-45) and the COVID-induced hiatus in 2020-2021. Traders might find it a welcome distraction since the Jackson Hole meeting gives them a perfect excuse to sit on the sidelines. Of course, an escalation in Middle East hostilities could change that.

The inflation beast may have been tamed, but the hard-landing beast is still on the loose.