Source: Anthem Entertainment/Hugh Syme

By Michael O’Neill

The late Neil Peart partnered with Pye Dubois to write the lyrics for “test for echo,” the title track of the sixteenth studio album by Rush. Twenty-four years later, financial market participants were again testing for echo. They found one in the Eccles Building, in Washington D.C, home of the Federal Reserve.

It came in the form of the Federal Open Market Committee (FOMC) statement, January 20, which echoed the December document. There were some modifications. The first line changed October to December. Household spending is no longer rising at a “strong pace,” the rise is merely moderate. There was a notable tweak. “In December, inflation was described as “near the Committee’s symmetric 2 percent objective.” The January statements now hopes inflation will be returning to the 2 percent objective. The inflation tweak suggests the statement was every-so-slightly dovish.

Expectations around this meeting were low, and they were met.

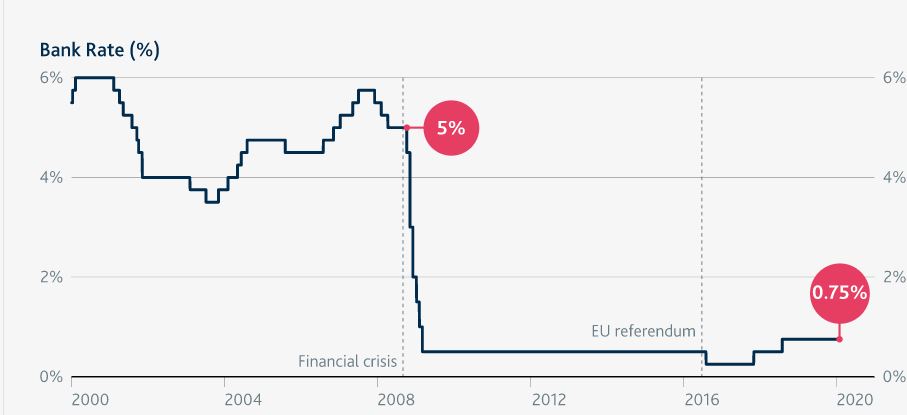

The old lady of Threadneedle Street heard echoes as well. Bank of England left interest rates unchanged at 0.75% again in hopes inflation returns to its 2.0% objective. According to the Monetary Policy Report (MPR), low, stable, and predictable inflation supports jobs and growth. Really? The following charts contradict that view. UK interest rates have not been higher than 0.75% for twelve years and since 2016, ranged between 0.25% and 0.75%. Those low rates do not appear to be supporting UK growth.

Bank rate barely moves….

Source: Bank of England MPR

Average growth rate shrinks…..

Source: Bank of England MPR

Governor Mark Carney, at his final press conference, repeated that UK business investment has weakened since the Brexit vote. The quarterly Monetary Policy Report said growth slowed, inflation is below the 2% targets, and if growth doesn’t pick up, interest rates could fall. If so, a rate cut may be in the cards as the MPR cut 2020 GDP growth to 0.8% from 1.2% previously.

GBPUSD rallied on the news. Traders are concluding that the BoE is less likely to cut interest rates in the coming months, as only two policymakers voted to cut rates, but those gains may evaporate in the days ahead. The UK officially exits the European Union on January 31, ending a forty-seven year membership in the bloc. Sterling suffered during the divorce negotiations, and it may suffer the same fate as it tries to negotiate a new trade deal with the EU.

Echoes of SARS (Severe Acute Respiratory Syndrome) are reverberating due to the Wuhan coronavirus. As of January 30, the virus has affected 7,921 people worldwide, of which 7,804 are in China. Financial markets shifted into risk-aversion mode, albeit reluctantly. Global equity indices are down, but the Dow Jones Industrial Average is still above its December 31 closing level when it finished the year with a 22% gain. Furthermore, the traditional safe-haven currency pairs, Swiss franc and Japanese yen are well-above their January lows. CNBC reported that the “what me worry” market reaction may stem from reports that although the coronavirus is “more infectious,” it is less severe than SARS with a correspondingly lower mortality rate. A cynic would suggest that, if you get the coronavirus, it is a life-threatening, debilitating infection, whereas a stranger’s infection is no big deal.

China ushered in the Year of the Rat on January 25. FX markets welcomed the Year of the (US dollar) Bull on January 1. At least that is how January is poised to finish. The US dollar is poised to end the first month of 2020 on an up-note, posting a 4.5% and 3.5% gain against the Australian and New Zealand dollars respectively. The Canadian dollar lost 1.8% in that time.

Why the attraction to US dollars? Quite simply, America is the only game in town. Federal Reserve Chair Jerome Powell repeatedly said that the US economy was in a good place, and since he said those words, the “place” has gotten better. The latest FOMC statement pointed out that the labour market remains strong and that economic activity has been rising. President Trump and China Vice Chair Liu He signed the US/China Phase 1 trade deal and on January 29, Mr Trump signed the United States Mexico Canada Agreement on trade.

Trade friction is still an issue. The US Trade war did not end with China and USMCA deals. It just moved to another front. President Trump is aiming his tariff cannon at France, and other European nations that threaten to levy a digital tax. He also has his sights trained on German auto imports into America. Elsewhere, the UK and European Union are preparing the groundwork for a new trade relationship.

US interest rates are still expected to remain unchanged for 2020, despite the inflation tweak in the monetary policy statement. That isn’t the case elsewhere. Bank of Japan officials are talking about the need for more monetary stimulus. The Reserve Banks of Australia and New Zealand are expected to cut rates in the near term, and the coronavirus may have exacerbated that need. The ECB is maintaining a dovish monetary policy, and the Bank of Canada opened the door to a Canadian rate cut.

There is no need to test for echo; you can hear it. The easy money mantra is reverberating throughout central bank meeting rooms, globally.