By Michael O’Neill, Agility FX, Senior Market Strategist

This year, the Canadian Thanksgiving turkey may be the Loonie. No, not the waterfowl that is depicted on the one-dollar coin but the currency that the coin represents.

The Canadian dollar may be in for a rough ride in the next few months and it isn’t all due to domestic issues. The oil price rally has stalled below $51.00 per barrel in WTI, forecasts for global economic growth this year and next, continue to be trimmed, the US presidential election poses serious risks for Canada and China is still attempting to finesse a soft landing. Lurking in the wings is the on-going UK negotiations for its exit from the European Union and the EU migrant crisis. Sabre rattling has gotten nosier as well. Reuters reported on September 29 that the Chinese military warned Japan that joint military patrols with the US, in the South China Sea, would be playing with fire. Russia and the US remain at odds over the Syria civil war and Ukraine. North Korea continues to threaten the West with aggressive missile tests. Any one of these risks or a combination of them, could put the Loonie in the roasting pan.

And that’s not all. The Bank of Canada does not appear enamored with the pace of growth in the Canadian economy and the stubbornly low inflation rate.

The rough ride is already starting. On Wednesday, September 28, oil prices soared over 5% on news that Opec agreed to cut production. That news also led to a dramatic jump in the value of the Canadian dollar against its American counterpart. That move may end in tears.

The official press release from the 170th (Extraordinary) meeting of the Opec Conference merely states that the Conference “opted for an OPEC-14 production target ranging between 32.5 and 33.0 million barrels per day, in order to accelerate the ongoing drawdown of the stock overhang and bring rebalancing forward.”

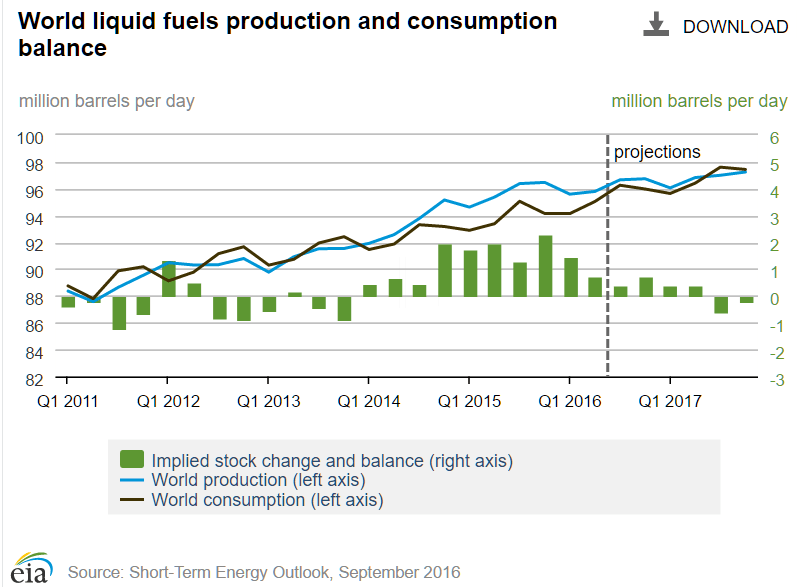

At first glance, it sounds impressive. Opec will reduce daily production about 0.4 mb/d to 0.9 mb/d. That sounds impressive until you realize that, according to the US Energy Information Administration, Q2 world oil production averaged 95.79 mb/d. The Opec reduction is a mere 1/10 of 1% of the daily oil production.

And that’s not the worst of it. This so-called deal is still a suggestion. Opec has turned the suggestion over to a committee, in order to study and recommend implementation which will be considered at the November meeting.

Oil price and USDCAD volatility will likely remain at elevated meetings until the November 30, Opec meeting.

Opec is counting on global growth to help sop up the excess over supplies. The problem with that thought is that many organizations are cutting global growth forecasts, not increasing them. On September 21st, the Organization of Economic Cooperation and Development (OECD) trimmed their 2016 forecast to 2.9% from 3%. The head of the International Monetary Fund, Christine Lagarde, said at the beginning of September, “The IMF will likely downgrade its 2016 global growth forecast in October”. If so, it would be the sixth downgrade in eighteen months.

Slowing global growth will undermine the Canadian dollar as it also implies slowing demand for raw materials which are key Canadian exports.

The US election is another major source of uncertainty for the Canadian dollar. Donald Trump repeatedly described the North American Free Trade Agreement (NAFTA) as the “worst deal ever” during the September 28 television debate. He is on record stating that if he is elected president, he would renegotiate or scrap the trade deal altogether.

Source: IFXA Ltd/IMGflip

You do not need to travel too far down memory lane to find out what happens to a currency when a country bails out of a trade agreement. Just look at what happened to the British pound when the UK voted to leave the European Union. GBPUSD dropped from 1.5000 to 1.2800. As long as Donald Trump remains a viable presidential candidate, nervous investors will ensure that Canadian dollar gains are limited.

Bank of Canada Governor Stephen Poloz may have given subtle encouragement to USDCAD buyers. On September 20 during a speech in Quebec, Mr. Poloz hinted that the BoC may have to trim growth forecasts as the current projections may be too optimistic. By itself, that statement would be considered doveish. Then came Canadian inflation data a few days later. The data wasn’t great. CPI was below expectations and at a ten-month low. The doves started flapping their wings and there were whispers of rate cuts in some camps. Fears of lower Canadian rates may be unfounded however the prospect of a rate increase is now further into the future.

The Canadian dollar strengthened impressively following news of that OPEC may have reached an accord on production quota’s but the sustainability of that rally is questionable. The details haven’t been worked out and it hasn’t been ratified leaving plenty of time for disappointment.

This Thanksgiving Loonie may not be seasoned with eleven herbs and spices but it won’t be bland, either. Trump, oil, the domestic economy and geopolitical risks will provide the flavor.