By Michael O’Neill

The Board of Governors of the US Federal Reserve want the world to believe that rising inflation is a transitory phenomenon, and not a reason to alter the existing course of monetary policy.

They are not concerned that soft word lumber climbed 118% in one year, or that WTI oil rose 102% since November. US airfares have risen 9% for domestic flights and 17% since April 1. They do not seem to think that restaurants, bars, and other service industries that lost substantial income from coronavirus restrictions won’t raise prices, and a lot higher than the Fed’s 2.05 inflation target.

Some analysts think Fed officials are madder than Lewis Carroll’s hatter in Alice in Wonderland. Others believe they just have their heads in the sand.

Picture: Publicdomainpictures.net

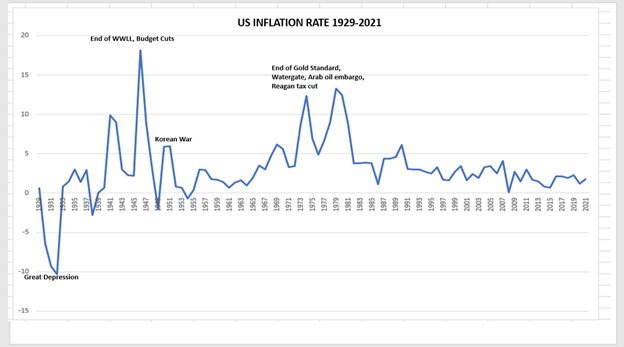

Fed officials may have a point. Inflation hasn’t been above 5.0% since 1991, so why worry?

The worry stems from 40+ years ago, when it took policymakers 9 years to reign in inflation which peaked at 13.3% in 1979 and averaged 9.4% between 1973 and 1981. Nine years is a long time to live with the damaging effects of high inflation levels.

Source: The balance.com/IFXA Ltd

That inflation problem will not reoccur in 2021. Fed Chair Jerome Powell has repeatedly said, “We understand well the lessons of the high inflation experience in the 1960s and 1970s, and the burdens that experience created for all Americans. We do not anticipate inflation pressures of that type, but we have the tools to address such pressures if they do arise.”

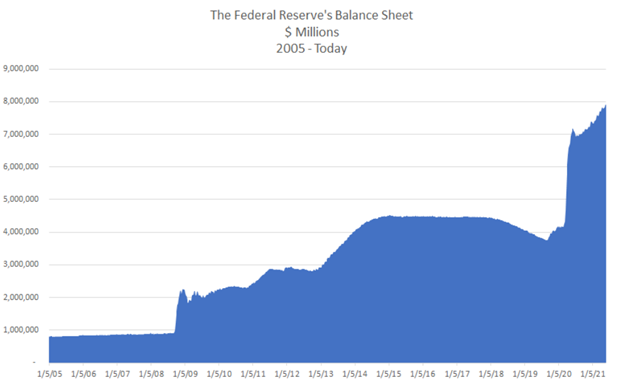

Quantitative Easing (QE) is the tool of choice. Simply put, QE is when the Fed issues securities to increase the money supply and increase lending, thereby lowering interest rates. QE was merely a theory until then-Fed Chair Ben Bernanke put it into practice in 2008.

Mr Bernanke’s successors, Janet Yellen, and Jerome Powell, loved QE, and between the trio, the Fed’s balance sheet has ballooned to $7.9 trillion (May 26, 2021) from just over $2.0 trillion in $2009. Nearly $3.0 trillion of that growth occurred since January 2020.

Source: American Action Forum

If QE is designed to lower inflation, what happens when QE purchases start to decline? The Bank of Canada says “nothing,” which suggests the Fed’s answer will be the same.

BoC Deputy Governor Toni Gravelle told the CFA society in Toronto, March 23, “I want to be clear here: moderating the pace of purchases while adding to our holdings would simply mean that we are still adding stimulus through QE but at a slower pace. It would not mean we are removing stimulus. We would be easing our foot off the accelerator, not hitting the brakes.”

Mr Gravelle added, “the timing of these moderations to the pace of purchases, and the amount of time that we take to get to the reinvestment phase, will be guided by our evolving assessment of the macroeconomic outlook and the strength and durability of the recovery.”

So, they are still stimulating the economy, but not as much. If it sounds like a taper, reduces like a taper, it is a taper. And tapering will lead to higher rates.

The BoC’s assessment of the economy is rapidly evolving. So much so that just a month after Mr Gravelle’s speech, Governor Tiff Mackem admitted the Canadian economy was considerably stronger than what they had expected, and he raised the BOC’s 2021 growth forecast to 6.5% from 4.3%.

The US economy is outperforming Canada’s, and JPMorgan economists are forecasting US core inflation (which excludes the impact of food and energy prices) at 2.8% for 2021. But like the Fed, they expect most, but not all, the rise in core inflation to fade.

If so, it suggests core inflation will be above the Fed’s 2.0% target. That itself is not a big deal as Mr Powell, and other Fed officials said the inflation target is when inflation achieves a sustainable average rate of 2.0% over time. “Over-time” was not quantified.

Albert Einstein is considered to have been a pretty clever fellow. He is known for developing the “Theory of Relativity”, and made considerable contributions to the “Theory of Quantum Physics”. He is often credited with coining the Definition of Insanity, as well.

Source: Publicdomainpictures.net

Mr Einstein said the definition of insanity is “doing the same thing over and over again and expecting a different result”.

That sounds a lot like Fed led, global central bank monetary policy. The Fed and the Bank of Canada have flooded the system with oceans of cash in an effort to boost inflation. Yet when inflation does rise, they claim it will be a transitory phenomenon.

The FOMC members may not be unhinged, but the following exchange from “Alice in Wonderland” sums up their deliberations.

“Have you guessed the riddle yet?′ the Hatter said, turning to Alice again. No, I give it up,′ Alice replied: `what’s the answer? I haven’t the slightest idea, said the Hatter.”