Photo: Rotten Tomatoes

By Michael O’Neill

To paraphrase Winston Churchill “Never in the field of economics has so much inflation hurt so many and been caused by so few.”

Inflation is running at 10.9% in the European Union, 9.9% in the Euro area, 10.1% in the United Kingdom, 8.2% in the USA and 6.9% in Canada. The inflation target for all those banks is around 2.0%.

That quartet of central banks share one key mandate-maintaining price stability. They have failed miserably.

Take a bow, Bank of Canada, and European Central Bank Governing Councils, good on you Bank of England Monetary Policy Committee, and a hearty well-done to the Federal Open Market Committee.

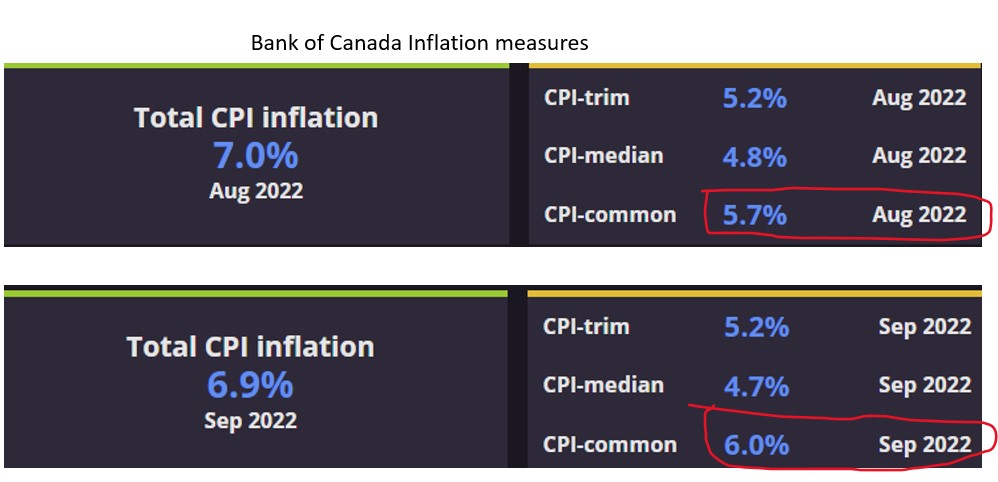

Statistics Canada proudly announced that the inflation decelerated from 7.0% in August to 6.9% in September. Do you feel better? Probably not, because food inflation (which only effects those that eat) soared 11.4%, the fastest pace since August 1981 which is just one year after Led Zeppelin broke up.

Inflation has left Bank of Canada officials “dazed and confused, and suffering a “communications breakdown,” as they warn of “good times bad times, but Bank of Canada Governor Tiff Macklem is loathe to admit its “nobody’s fault but mine.”

If you were confused by the Core-CPI reading you are not alone. Statistic’s Canada measures core-inflation the traditional way, by excluding food and energy while the Bank of Canada has adopted a different measure.

They call it CPI-common which “is based on trends in price changes that are similar across the various categories in the CPI basket, rather than focusing on increases to specific items, such as the prices of gasoline or fruit. It uses a statistical procedure called a factor model to detect these common variations, which helps filter out price movements that might be caused by factors specific to certain components core-inflation. Yada, yada, yada.

Source: Bank of Canada

Unfortunately, CPI-common doesn’t work. Mr Macklem admitted as much on October 6 when he said, “Of our three measures, CPI-common is becoming more difficult to use in real time because it has been subject to large historical revisions.”

A former Chief Economist at a major US Investment market explained CPI/Core CPI in golf terms. He said, it is like determining the winner of a foursome of duffers playing a par 72 golf course.

The gross score should win but when handicaps are included, it is not necessarily the case. That’s the same as inflation. CPI is an estimate of real inflation, and the core measure (after dubious adjustments) is whatever the Bankers want you to think.

Canadian consumers are reminded about inflation every time they open their wallets, tap their debit cards, or use Google Pay. They only care about what the CPI data means for interest rates.

They will not be happy. The BoC’s Business Outlook Survey warned that inflation expectations risk becoming entrenched which are exacerbated by the firm CPI data and all but guarantee a 75-basis point rate hike October 26.

A rate hike won’t do much for the Canadian dollar. Fed Chair Jerome Powell will determine its direction.

The Fed Chair is the most to blame for surging global inflation. He stubbornly ignored signs that inflation was rising and insisted it was transitory. As the boss man for the most powerful central bank in the world’s largest economy, his words carried a lot of weight. So much so that” transitory” became the “go-to” word by central bankers worldwide to explain higher prices. When he finally changed his tune, he went from a contented dove to a ravenous, inflation fighting hawk. He dispensed of any notion that the Fed would engineer a “soft-landing” and on September 22 warned that if the process led to a recession no one knows how significant that recession would be.

He seems to have converted many FOMC members. On October 18, Minneapolis Fed President Neal Kashkari said that “if we don’t see progress in underlying inflation, I don’t see why I would advocate stopping at 4.5% or 4.75%, or something like that.”

The hawkish Fed rhetoric has fueled a steep rise in the US 10-year yield which climbed from 3.61% on October 5 to over 4.12% on October 19. That move help to snap the October S&P 500 rally and set the stage for further losses which targets the 3500 level.

Rising US Treasury yields and falling S&P 500 prices will drive USDCAD to 1.4000, likely before month end.

Central banks used to be held to the highest regard due to the steady guiding hands navigating economies through troubled waters. In a word, they were “credible.” Not today. They are the “not-so-Incredibles, known for missteps, mistakes, and miscommunication.