Photo: prezi.com

By Michael O’Neill

Those that don’t believe history repeats, flunked history. This is America today.

Economic prosperity, margin trading exacerbates stock price gains-√

Increased consumption of illegal substances √

Growth in air travel accelerates √

Large-scale development of cars, phones √

Geopolitical tensions elevated √

Media fixated on movie stars and celebrities to fuel demand √

It was also America in the 1920’s.

And most people know what followed.

The Great Depression kicked off on October 28, 1929, after the Dow Jones Industrial Average (DJIA) plunged 13%. It finally found a bottom in the summer of 1932, dropping 89% from its peak.

If the DJIA suffered a repeat performance, the index would plummet to 4,064.79 based on the January 4 peak of 36, 952.65.

A drop of that magnitude is not going to happen in this era unless there is a planet-destroying nuclear apocalypse. The odds of that happening are not zero, especially with the likes of Russia’s Vladimir Putin, North Korea’s Kim Jung-Un, and Iran’s Supreme leader Ali Khamenei, in the equation.

That doesn’t mean stocks won’t fall.

They will. The S&P 500 has gained nearly 3% since the beginning of August, and the month isn’t even half-over. That gain is despite US inflation rising 8.5% y/y in July.

President Joe Biden jumped all over the inflation report tweeting, “July’s 0% inflation and last week’s booming jobs report underscore the kind of economy we’re building – an economy that works for everyone.”

Biden is right. The economy works for everyone, at least those who do not eat (food inflation rose 1.1%), use energy (energy is still up 32.9% y/y), or live indoors (shelter rose 0.5% after a 0.6% increase in June)

Interestingly, when CPI hit 8.5% in March, it was viewed as a catastrophe, while today it is an opportunity.

Traders have decided that because July inflation was lower than June’s 9.1% y/y rate, inflation has peaked, which means the Fed will soon be cutting rates. “Give your head a shake” is the message from some Fed policymakers.

Chicago Fed President Charles Evans said inflation remains “unacceptably high” even after the latest CPI print. He expects rates to rise to 4.0 by the end of 2023, while his colleague Neel Kashkaris predicts 4.4%.

The S&P technical picture warns the latest rally is unsustainable, with weekly and daily indicators well into overbought territory.

Nevertheless, the Wall Street stock rally has turned global risk sentiment positive and fueled a steep slide in the US dollar. The US dollar index ( a weighted average of the euro, Japanese yen, British pound, Canadian dollar, Swedish krona, and Swiss franc) is in a month-long slump, falling from 109.10 to 104.50 on August 11. Short-term technicals suggest further weakness to 103.05 on a sustained break below 104.20.

And that’s what is fueling Canadian dollar gains. Canadians like to believe that the Bank of Canada and the government dictate the direction of the currency. They do, from a long-term macroeconomic view. However, that view, like a large swath of financial market participants, is on holiday.

The Canadian dollar is unlikely to remain at these lofty levels due to poor fundamentals and bullish long-term technicals.

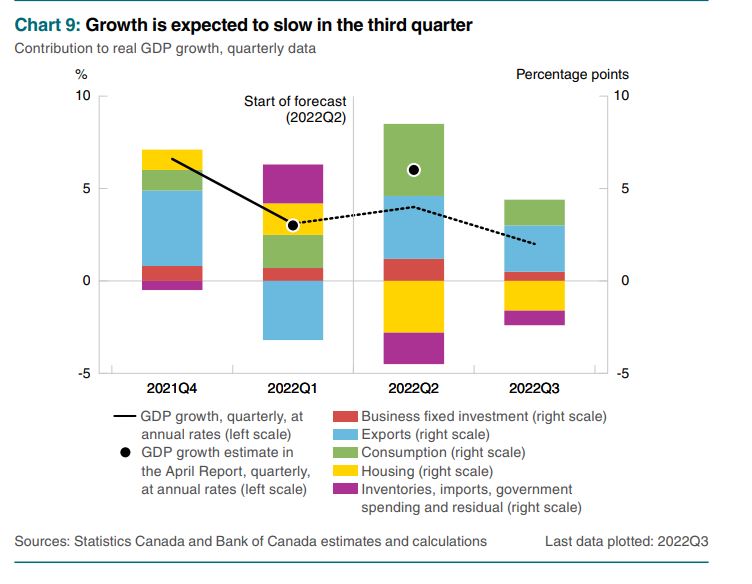

The Bank of Canada expects domestic growth to slow to 3.5% in 2022 and then fall sharply to 0.3% in 2023. The slowdown is due to the fading impact from the easing pandemic restrictions, consumers dealing with high inflation, and rising interest rates.

Chart: Bank of Canada MPR

The view of USDCAD as a petrocurrency has been tarnished in recent years. The Canadian government loathes Alberta’s oil sands, hampered pipeline expansion, and scared off foreign investors. West Texas Intermediate (WTI) is trading below where it sat before Russia invaded Ukraine, but the slump in crude prices has not impeded USDCAD sellers.

USDCAD climbed from a low of 0.9010 on November 7, 2007, and peaked at 1.4653 Monday January 19, 2016. It has since traded in a 1.2000-1.4650 range with a longterm uptrend bias while prices are above 1.2350, a level guarded by a short term uptrend at 1.2600. That suggests the USDCAD downside is limited to the 1.2600-20 area.

Uncle Sam, or more accurately Jerome Powell, is the largest influence on the Canadian dollar. He said he is committed to lowering inflation to 2.0% so will not be impressed with CPI at 8.5%. The Cleveland Fed’s inflation Nowcast projects August CPI at 8.39% , core CPI at 6.22% and Core PCE at 4.83%. Those are levels that will ensure the Fed continues to tighten policy. The Fed’s interest rate guidance will dictate S&P 500 direction, and by default USDCAD direction, which is likely to be higher in the second half of 2022.

The US and Canadian economies enjoyed a robust recovery from the pandemic, and things are still looking pretty good.

Nevertheless, it makes sense to be cautious as today’s world has many similarities to the “Roarin 20’s” in the previous century and we know how that era ended.