Photo: Mondelez International/Cadbury/IFXA

By Michael O’Neill

Geopolitical tensions are on the rise.

Canada is the latest country to feel China’s wrath for complaining and reacting to Beijing’s bad behaviour. Both countries are kicking out diplomats to show disapproval.

Ukraine is on the cusp of launching a counter-offensive to oust Russian forces. This is a pre-announced move, which may be as effective as Russia’s 30-day plan to capture Ukraine in 2022.

US and China relations are deteriorating and becoming bitter with each passing moment. The US is flexing its financial and trade muscles to ban Chinese Apps and prevent strategic technology sales or purchases.

The global tensions are occurring at the same time Uncle Sam looks lost.

China is crafting an alliance with American foes, particularly Russia and Iran, while using its massive cash hoard to undermine US influence in South America and Africa.

The US spent 20 years, and reportedly $2.13 billion, trying and failing to tame the Taliban. They looked like whipped puppies when they fled the country in 2020. Joe Biden was Commander-in-Chief, and he was seventy-eight at the time. His performance may have encouraged Vladimir Putin to invade Ukraine.

On May 4, the US Government Accountability Office, reporting on US military readiness, said that mission capability and readiness ratings declined from 2017 to 2021. Of particular note was that naval forces faced a $1.8 billion backlog in maintenance and poor shipyard infrastructure. Even worse, Navy ships faced staffing shortfalls and fatigued crews.

Meanwhile, China already has the world’s largest navy boasting 340 warships compared to around 300 for the US.

The President is well-past his best-before-date, the former president was convicted in a civil trial for sexually abusing and defaming a woman, (and wants to run again) while Republicans and Democrats threaten to put the country into default.

Geopolitical risks are being ignored by the financial markets. Traders have adopted the NIMBY-NOMP approach (“not in my backyard, not my problem”). They only care about the Fed’s interest rate plan.

It is all that matters.

Headline CPI dipped to 4.9% y/y from 5.0% in March. The headlines shouted, “US inflation cools,” US inflation drops below 5.0% for the first time since 2022.”

The next day, producer prices rose just 0.2% while jobless claims rose.

The CME FedWatch tool odds are 85% for a 25 bp rate cut in September.

If the market is right and the Fed cuts rates in September, what does that mean for stocks, bonds or the US dollar?

For starters, cutting rates means the Fed is starting a victory lap because they believe they have slayed the inflation dragon. Treasury yields will retreat with traders debating how low rates will fall.

But what if the Fed cuts interest rates to avert a credit crunch?

A credit crunch and a recession go hand in hand and a recession is not usually bullish for stocks, while the US dollar may rally because of its safe-haven status.

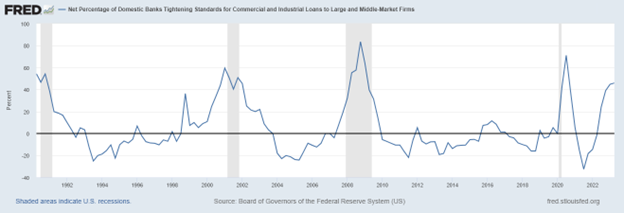

The latest Senior Loan Officer Opinion survey (LOOS) found that banks expect to tighten lending standards for the rest of the year due to recession concerns and the fallout from the Silicon Valley Bank collapse.

The Fed’s Financial Stability Report warned that worries about the economic outlook, credit quality, and funding liquidity could cause “banks and other financial institutions to further contract the supply of credit.”

Chicago Fed President Austan Goolsbee seems to agree. He said “The credit crunch or at least the credit squeeze is beginning. I think you have to say that recession is a possibility.”

The following chart argues that the credit crunch has arrived.

Source: FRED St Louis Fed

A US recession isn’t favorable for the Canadian dollar.

If the US is in recession, Canada will follow suit, mainly because 70% of Canada’s trade is with America.

Canada exported USD 458 billion of goods to the US in 2022. Of these, mineral fuels, oils and distillates, vehicles and lumber accounted for 88.8% of the total. If the US is in recession, demand for Canadian exports will decline, suggesting higher unemployment and slower growth.

Twin Canadian and US recessions do not always occur. It didn’t happen in 2008. There was an economic downturn, but Canada did not experience two consecutive quarters of negative growth.

The Canadian dollar was not convinced. It dropped 37% between November 2007 and October 2008, mainly due to a plunge in WTI prices, which fell from $147.00/b to $33.00/b.

Things are different today. Opec and Russia are aggressively managing oil supply, and are happy to reduce production to support prices.

Canada is different. The government is actively transitioning away from fossil fuels and has taken measures to hamper new oil infrastructure investments. The drop in foreign investment erodes Canadian dollar support, even with elevated crude prices.

If you strip out the extreme covid-era USDCAD price moves, USDCAD is in a 1.2960-1.3880 range, and the long term uptrend that began in 2022 is intact above 1.3200.

The storm clouds are gathering but USDCAD may be closer to the bottom than the top.

Chart: USDCAD monthly 15 years.

Source: Saxo Bank