Source: Wikipedia

By Michael O’Neill

The UK Prime Minister wore the COVID-19 crown on April 5, 2020. He went from exhibiting COVID-19-like symptoms to requiring oxygen in ICU at the St Thomas Hospital in London. Doctors released him a week later.

President Trump donned the COVID-19 crown on October 1, notifying the world in a tweet. “Tonight, @FLOTUS and I tested positive for COVID-19. We will begin our quarantine and recovery process immediately. We will get through this TOGETHER!”

Trump’s experience was a tad different from that of the UK Prime minister. No ride in a battered ambulance to an inner-city hospital for the so-called “leader of the free world.” Instead, Marine 1 airlifted him to Walter Reed Army Medical Center, a mere 13.6 kms away, where a phalanx of physicians greeted his arrival.

Four days later, Mr Trump tweeted I will be leaving the great Walter Reed Medical Center today at 6:30 P.M. Feeling really good! Don’t be afraid of Covid. Don’t let it dominate your life. We have developed, under the Trump Administration, some really great drugs & knowledge. I feel better than I did 20 years ago!

Sadly, the 1,051,000 people who died from the virus, didn’t receive the same level of health care as Mr Trump, and none of them feel better than they did 20 years ago.

Predictably, financial markets reacted to news of Trump’s COVID-19 diagnosis like it was the end of the world, before many realized the story was a baloney sandwich, without the bread.

Boris Johnson’s approval rating got a bump higher, which may be attributed to respondents actually liking the Prime Minister, however his attitude toward the pandemic was just as stupid, (he insisted on shaking hands ignoring a critical coronavirus defence).

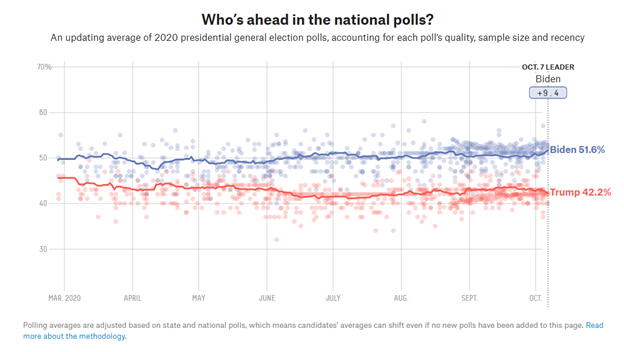

If President Trump hoped for a similar bump in his election fortunes, he would be disappointed. His approval rating barely budged. If you believe the polls, its Democrat Joe Biden’s election to lose.

He is ahead by 9.4 points in the latest polls aggregated by FiveThirtyEight.com

Source: FiveThirtyEight.com

Do the polls even matter? Not really. Not after Hillary Clinton’s experience. She went from “President-to-be-elected” to “President rejected.”

Traders are no longer just concerned about how stock markets will react to Trump or Biden presidency. The President’s health scare, and the advanced age of the candidates, put a spotlight on their running mates. One of these candidates may find themselves taking the Oath of the Office of the President, and so the October 7th debate may attract more viewers than usual.

Although the US election results have a significant impact on global geopolitical and economic affairs, that impact doesn’t occur instantly.

There are more pressing concerns for financial markets. The EU/UK divorce may turn nasty. London is the world’s largest financial center, controlling 90% of euro-denominated derivatives, and one-third of EU capital markets activity. Financial services contributed 6.9% of the UK’s GDP in 2018, and without a deal by December 31, a smooth transition may not occur, disrupting global markets.

The coronavirus is the cockroach of global medicine. No matter what governments do, they can’t get rid of it. New coronavirus cases in the US are well-above the peak-March to June levels. The UK has experienced a sharp jump in hospitalizations this week. Eurozone countries are not unscathed. Paris is on the verge of a new lockdown; Berlin identified several risk areas and EU Commission President Ursula von der Leyden is self-isolating.

Canada added another 2,364 new COVID-19 cases on October 6. More than half of those cases were in Quebec.

In the second quarter of 2020, world governments spent billions and trillions supporting economies and workers who were locked down to help stem the spread of the virus. Central banks did their part. They slashed interest rates to near-zero or even negative, and ramped up quantitative easing programs to stimulate and support economies.

But that was then. What’s left for COVID-19, the Sequel?

Canada GDP dropped 38.7% y/y between April and June this year, and that is after the Federal government deficit surged to $328.5 billion to support the economy. The Parliamentary Budget office said that domestic growth won’t reach its pre-pandemic level until 2022, and that forecast doesn’t include a second-wave.

How much additional spending will be needed to counter the impact of the second wave of coronavirus. The hospitality and travel industries are still reeling from the first pandemic and will be hard-pressed to survive another wave of lockdowns. Commercial landlords must deal with tenants asking for relief, while Banks insist, they continue to service their debt.

Kit Juckes, Macro Strategist at Societe Generale, observed that countries that went into the first pandemic with poor public finances will pay the price for their heavily indebted positions. Countries with low debt like Switzerland and Australia, are better position to spend their way to an economic rebound.

Canada’s deficit is going to get worse. A week ago, Prime Minister Trudeau announced a $10 billion infrastructure spending plan, which will put a smile on the faces of green energy enthusiasts but does nothing for workers impacted by both waves of the coronavirus.

The US bond market is starting to price in more spending in the event of a Biden victory. With little scope for a reduction in government spending in Canada, how long before rates back up here. It then becomes hard to justify increased deficit spending because “rates are low”

The Canadian economy is likely to underperform its G-10 peers, which suggests the Canadian dollar will underperform as well.

The head that wears the COVID crown may be uneasy, but it beats a dunce cap.